RBS 2005 Annual Report Download - page 80

Download and view the complete annual report

Please find page 80 of the 2005 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

|

|

78

Operating and financial review

Operating and financial review continued

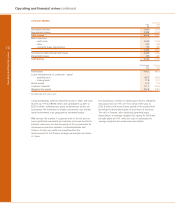

Citizens

Pro forma

2005 2004

£m £m

Net interest income 2,122 1,619

Non-interest income 1,142 659

Total income 3,264 2,278

Expenses

– staff costs 819 591

– other 739 501

1,558 1,092

Contribution before impairment losses 1,706 1,186

Impairment losses 131 117

Contribution 1,575 1,069

31 December 1 January

2005 2005

US$bn US$bn

Total assets 158.8 141.7

Loans and advances to customers – gross 104.6 91.7

Customer deposits 106.3 99.2

Weighted risk assets 106.4 93.5

Average exchange rate – US$/£ 1.820 1.832

Spot exchange rate – US$/£ 1.721 1.935

Citizens performed well in 2005, delivering a strong underlying

performance in challenging market conditions both from the

old Citizens franchise and from Charter One. Total income, in

US dollars, rose by 42% to $5,940 million and contribution by

46% to $2,867 million, including a full year’s contribution from

Charter One. Excluding Charter One and other acquisitions,

income rose by 6% and contribution by 10%, despite the

impact of the flattening of the yield curve, which reduced net

interest margin and the rate of growth in net interest income.

We have grown our customer numbers in both personal and

business segments, with Charter One increasing its small

business and corporate customer base by 10%. Co-operation

between Citizens and RBS Corporate Markets is yielding good

results. Citizens’ new international cash management service

has already won nearly 300 new accounts with existing RBS

customers, bringing in more than $80 million of new core

deposits.

Our cards businesses, which are only active in the prime and

superprime segments, have made good progress. Credit card

balances increased by 19% to $2.5 billion, as RBS National

launched into a number of new channels such as Charter One

branches. RBS Lynk, our merchant acquiring business,

increased its customer base by 24%.

The integration of Charter One progressed well and all phases

of the IT conversion were completed in July 2005, five months

ahead of schedule. This involved the conversion to Citizens’

systems of over 750 branches and three million customer

accounts spread over a wide geography. Despite the focus on

the integration process, Charter One achieved good growth in

business volumes, with loans and advances up 18% over the

course of the year and customers deposits up 10%.

Net interest income increased by 30% to $3,861 million. This

reflected strong growth in both lending and deposits.

Excluding acquisitions, average lending increased by 13% or

$6.7 billion, with robust growth in secured consumer lending,

and average customer deposits by 9% or $5.7 billion. However,

as a consequence of the flattening yield curve, net interest

income excluding acquisitions was only 3% higher at $2,534

million.

Non-interest income was up 72% to $2,079 million. Excluding

acquisitions, non-interest income grew by 15% to $1,004

million, benefiting from higher fee income, increased student

loan and leasing activities, and investment gains.

Expenses were up 42% to $2,834 million. Expense growth,

excluding acquisitions, was contained to 5%.

Impairment losses, including acquisitions, were up $25 million

to $239 million. Credit quality overall remained stable. More

than 90% of our personal sector lending is secured, and as a

result there was minimal impact from the change in US

bankruptcy laws in 2005.