RBS 2005 Annual Report Download - page 158

Download and view the complete annual report

Please find page 158 of the 2005 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

148 -

149

149 -

150

150 -

151

151 -

152

152 -

153

153 -

154

154 -

155

155 -

156

156 -

157

157 -

158

158 -

159

159 -

160

160 -

161

161 -

162

162 -

163

163 -

164

164 -

165

165 -

166

166 -

167

167 -

168

168 -

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

|

|

156

Notes on the accounts

Notes on the accounts continued

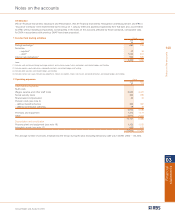

Securitisations

The Group engages in securitisation transactions of its

financial assets including commercial and residential mortgage

loans, commercial and residential mortgage related securities,

US Government agency collateralised mortgage obligations,

and other types of financial assets. In such transactions, the

assets, or interests in the assets, are transferred generally to a

special purpose entity which then issues liabilities to third

party investors.

Securitisations may, depending on the individual arrangement,

result in continued recognition of the securitised assets;

continued recognition of the assets to the extent of the

Group’s continuing involvement in those assets; or

derecognition of the assets and the separate recognition, as

assets or liabilities, of any rights and obligations created or

retained in the transfer (see Accounting policy on page 141).

The Group has securitisations in each of these categories.

Continued recognition

The table below sets out the asset categories together the carrying amounts of the assets and associated liabilities.

2005 2004

Assets Liabilities Assets Liabilities

Asset type £m £m £m £m

Residential mortgages (1, 2) 2,388 2,366 1,519 1,479

Finance lease receivables (1, 3) 1,467 1,170 1,897 1,502

Other loans (1, 4) 2,189 1,543 1,713 1,313

Credit card receivables (5) 2,891 2,836 1,133 1,133

Commercial paper conduits (6) 6,688 6,685 4,704 4,696

(1) At 31 December 2004, in accordance with previous GAAP, the financial assets in these categories were derecognised to the extent of non-recourse finance as the arrangements

qualified for the linked presentation.

(2) Mortgages have been transferred to special purpose vehicles, held ultimately by charitable trusts, funded principally through the issue of floating rate notes. The Group has

entered into arm’s length fixed/floating interest rate swaps with the securitisation vehicles and provides mortgage management and agency services to the vehicles. On

repayment of the financing, any further amounts generated by the mortgages will be paid to the Group. In 2004, the Group recognised net income of £26 million.

(3) Certain finance lease receivables (leveraged leases) involve the Group as lessor obtaining non-recourse funding from third parties. This financing is secured on the underlying

leases and the provider of the finance has no recourse whatsoever to the other assets of the Group. In 2004, the Group recognised net income of £13 million.

(4) Other loans originated by the Group have been transferred to special purpose vehicles funded through the issue of notes. Any proceeds from the loans in excess of the amounts

required to service and repay the notes are payable to the Group after deduction of expenses. In 2004, the Group recognised net income of £37 million.

(5) Credit card receivables in the UK have been securitised. Notes have been issued by a special purpose vehicle. The note holders have a proportionate interest in a pool of credit

card receivables that have been equitably assigned by the Group to a receivables trust. The Group continues to be exposed to the risks and rewards of the transferred

receivables through its right to excess spread (after charge offs).

(6) The Group sponsors commercial paper conduits. Customer assets are transferred into an SPE which issues notes in the commercial paper market. The Group supplies certain

services and contingent liquidity support to these vehicles on an arm’s length basis as well as programme credit enhancement.

12 Loans and advances to customers (continued)