RBS 2005 Annual Report Download - page 79

Download and view the complete annual report

Please find page 79 of the 2005 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

|

|

section

01

Operating and

financial review

77

Operating and financial review

Annual Report and Accounts 2005

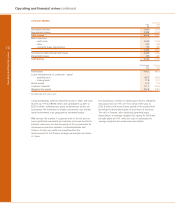

Ulster Bank

Pro forma

2005 2004

£m £m

Net interest income 655 559

Non-interest income 203 190

Total income 858 749

Expenses

– staff costs 191 170

– other 79 74

270 244

Contribution before impairment losses 588 505

Impairment losses 58 45

Contribution 530 460

31 December 1 January

2005 2005

£bn £bn

Total assets 35.9 28.7

Loans and advances to customers – gross

– mortgages 13.2 10.1

– other 15.0 12.9

Customer deposits 15.9 13.6

Weighted risk assets 22.4 18.6

Average exchange rate – €/£ 1.463 1.474

Spot exchange rate – €/£ 1.457 1.418

Total income increased by 15% to £858 million, with

contribution also up 15% to £530 million, as Ulster Bank

achieved another year of strong growth, with excellent

customer recruitment, robust lending volumes and very good

growth in deposits. First Active continues to perform well and

in line with our integration plan. It led the Republic of Ireland

market with the introduction of new mortgage products, as well

as launching new credit card and direct loan products.

The number of personal and business customers increased by

68,000 in the year. Ulster Bank personal customer numbers

rose by 9% in the Republic of Ireland, where our switcher

mortgage product has helped us to gain market share. In

Northern Ireland, Ulster Bank significantly enhanced its

personal current account offering in the fourth quarter to

provide free banking to all customers.

Net interest income rose by 17% to £655 million. Average loans

and advances increased by 33% to £25.0 billion and average

customer deposits by 21% to £14.4 billion. The continuing

strong growth in lending, particularly in mortgages and

business loans, led to a decline in net interest margin.

Non-interest income increased by £13 million or 7% to £203

million. This reflected increased volumes of customer

transactions and good growth in income from financial markets

services.

Expenses increased by 11% to £270 million, as a result of

investment to support the growth of the business. This

investment will continue into 2006. We have continued with our

branch improvement programme, upgrading 50 branches in

the Republic of Ireland and 39 in Northern Ireland.

Impairment losses increased by £13 million to £58 million,

reflecting the growth in lending.