RBS 2005 Annual Report Download - page 212

Download and view the complete annual report

Please find page 212 of the 2005 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

202 -

203

203 -

204

204 -

205

205 -

206

206 -

207

207 -

208

208 -

209

209 -

210

210 -

211

211 -

212

212 -

213

213 -

214

214 -

215

215 -

216

216 -

217

217 -

218

218 -

219

219 -

220

220 -

221

221 -

222

222 -

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

|

|

210

Notes on the accounts

UK GAAP

(a) Goodwill

Goodwill arising on acquisitions after 1 October 1998 is

capitalised and amortised over its estimated useful economic

life. Goodwill arising on acquisitions before 1 October 1998

was deducted from equity. Goodwill is reviewed for impairment

at the end of the first full year following an acquisition and

subsequently if events or changes in circumstances indicated

that its carrying value might not be recoverable,

(b) Intangibles other than goodwill

Computer software development costs

Most computer software development costs are written off as

incurred.

Other intangibles

An intangible asset acquired in a business combination is

capitalised separately from goodwill only if it can be disposed

of separately from the revenue-earning activity to which it

contributes and its value can be measured reliably.

(c) Leasing

Finance lease income is recognised so as to give a level rate

of return on the net cash investment in the lease; tax cash

flows are taken into account in allocating income.

Assets held under operating leases are depreciated on a

straight-line or reverse-annuity basis.

(d) Dividends

Dividends payable on ordinary shares are recorded in the

period to which they relate.

(e) Consolidation

UK GAAP requires consolidation of entities controlled by the

reporting entity. Control is the ability to direct the financial and

operating policies of an entity.

(f) Life assurance

To reflect the distinct nature of long-term assurance assets and

liabilities attributable to policyholders, they are shown

separately on the consolidated balance sheet; the results of

life assurance business are presented as a single contribution

to profit before tax.

Changes in embedded value determined on a post-tax basis

are grossed up for inclusion in the income statement.

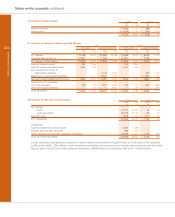

45 Transition to IFRS

(1) Significant differences between the Group’s UK GAAP accounting policies applied in its 2004 financial statements

and its IFRS accounting policies

IFRS

Goodwill is recorded at cost less any accumulated impairment

losses. Goodwill is tested annually for impairment or more

frequently if events or changes in circumstances indicate that it

might be impaired.

The carrying amount of goodwill in the Group’s opening IFRS

balance sheet (as at 1 January 2004) was £13,131 million, its

carrying value under UK GAAP as at 31 December 2003.

Computer software development costs are capitalised if they

create an identifiable intangible asset. They are amortised over

their estimated useful life of three years. Net computer

software development costs of £818 million were recognised

on transition to IFRS.

An intangible asset is recognised as an asset separately from

goodwill if it is separable or if it arises from contractual or

other legal rights regardless of whether these rights are

transferable or separable.

Core deposit intangibles of £268 million, mortgage servicing

rights of £81 million, customer relationships of £162 million

and other intangibles of £18 million were recognised in

business combinations that took place in 2004.

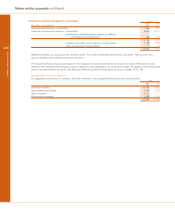

IFRS requires a level rate of return on the net investment in the

lease. Tax cash flows are not reflected in the pattern of income

recognition.

Assets held on operating leases are depreciated on a straight-

line basis.

Dividends are recorded in the period in which they are

declared.

All entities controlled by the Group are consolidated together

with special purpose entities (SPEs) where the substance of

the relationship between the reporting entity and the SPE

indicates that it is controlled by the reporting entity.

Assets, liabilities, income and expense of life assurance

business are consolidated on a line-by-line basis.

Movements in embedded value are not grossed up, instead

they are included net of tax in profit before tax.

Notes on the accounts continued