RBS 2005 Annual Report Download - page 131

Download and view the complete annual report

Please find page 131 of the 2005 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

139 -

140

140 -

141

141 -

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

|

|

section

02

Governance

129

Directors’ remuneration report

Annual Report and Accounts 2005

Directors’ pension arrangements

During the year, Sir Fred Goodwin, Gordon Pell, Iain Robertson

and Fred Watt participated in The Royal Bank of Scotland

Group Pension Fund (“the RBS Fund”). The RBS Fund is a

defined benefit fund which provides pensions and other

benefits within Inland Revenue limits.

The pension entitlements of Sir Fred Goodwin, Mr Pell, Mr

Robertson and Mr Watt within the RBS Fund are restricted

by Inland Revenue limits as set out in the Finance Act 1989.

Additional life assurance cover in excess of these limits is

provided by a separate arrangement. Arrangements have been

made to provide Sir Fred Goodwin and Mr Pell with additional

pension benefits on a defined benefit basis outwith the RBS

Fund. The figures shown below include the accrual in respect

of these arrangements. Mr Watt was provided with additional

pension benefits on a defined contribution basis and

contributions made in the year are shown below.

No changes are proposed to the level or form of pension

benefits for any of the current directors as a result of the

changes in pension legislation which come into force in April

2006 although as stated above directors will be able to opt out

of tax-approved pension provision if they wish and receive a

salary supplement in lieu. In addition consideration will be

given to funding a greater proportion of the benefits.

Of the total transfer value as at 31 December 2005 shown,

25% relates to benefits in funded pension schemes.

Sir George Mathewson receives life insurance cover under an

individual arrangement. The non-executive directors do not

accrue pension benefits, other than Mr Robertson who

continued to accrue benefits in the RBS Fund after his

appointment as a non-executive director.

Lawrence Fish accrues pension benefits under a number of

arrangements in the US. Defined benefits are built up under

the Citizens’ Qualified Plan, Excess Plan and Supplemental

Executive Retirement Arrangement. In addition, he is a

member of two defined contribution arrangements – a

Qualified 401(k) Plan and an Excess 401(k) Plan.

As in the 2004 Report and Accounts, disclosure of these

benefits has been made in accordance with the United Kingdom

Listing Authority Listing Rules and the Combined Code and with

the Directors’ Remuneration Report Regulations 2002.

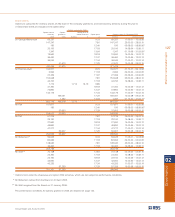

Transfer value

Additional Additional for the additional

pension pension Increase pension

earned earned in transfer earned

Accrued during the during the Transfer Transfer value during during the

entitlement at year ended year ended value as at value as at year ended year ended

Age at 31 December 31 December 31 December 31 December 31 December 31 December 31 December

31 December 2005 2005 2005* 2005 2004 2005 2005*

Defined benefit arrangements 2005 000 p.a. 000 p.a. 000 p.a. 000 000 000 000

Sir Fred Goodwin 47 £444 £63 £51 £5,119 £3,591 £1,528 £592

Mr Pell 55 £302 £55 £47 £5,092 £3,592 £1,500 £790

Mr Robertson 60 £37 £4 £3 £676 £565 £111 £48

Mr Watt 45 £9 £2 £2 £96 £62 £34 £19

Mr Fish 61 $1,384 $244 $244 $13,347 $10,046 $3,301 $2,350

* net of statutory revaluation applying to deferred pensions

Notes:

(1) There is a significant difference in the form of disclosure required by the Combined Code and the Directors’ Remuneration Report Regulations 2002. The former requires the

disclosure of the additional pension earned during the year and the transfer value equivalent to this pension based on stock market conditions at the end of the year. The latter

requires the disclosure of the difference between the transfer value at the start and end of the year and is therefore dependent on the change in stock market conditions over

the course of the year. The above disclosure has been made in accordance with the Combined Code and the Directors’ Remuneration Report Regulations 2002.

(2) Mr Robertson continued to accrue pension during his service with the Group in 2005 after resignation as a director. The figures above include the pension accrued during this

subsequent service.

(3) The transfer values disclosed above do not represent a sum paid or payable to the individual director. Instead they represent a potential liability of the company /pension scheme.

(4) No allowance is made in these transfer values for any enhanced benefits that may become payable on early retirement.

(5) The proportion of benefits represented by funded pension schemes for Sir Fred Goodwin, Gordon Pell and Lawrence Fish is 3%, 69% and 3% respectively. All benefits for

Iain Robertson and Fred Watt are in funded pension schemes.

(6) Following Mr Pell’s appointment as Executive Chairman, Retail Markets, he was awarded enhanced pension benefits.

(7) In accordance with US market practice, Mr Fish’s pensionable remuneration is limited to $4 million per annum.

Contributions and allowances paid in the year ended 31 December 2005 under defined contribution arrangements were:

2005 2004

000 000

Mr Watt £144 £128

Mr Fish $139 $91

Bob Scott

Chairman of the Remuneration Committee

27 February 2006