BB&T 2013 Annual Report Download - page 128

Download and view the complete annual report

Please find page 128 of the 2013 BB&T annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

|

|

128

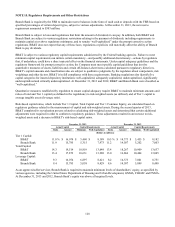

NOTE 15. Regulatory Requirements and Other Restrictions

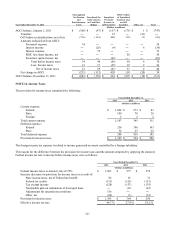

Branch Bank is required by the FRB to maintain reserve balances in the form of vault cash or deposits with the FRB based on

specified percentages of certain deposit types, subject to various adjustments. At December 31, 2013, the net reserve

requirement amounted to $303 million.

Branch Bank is subject to laws and regulations that limit the amount of dividends it can pay. In addition, both BB&T and

Branch Bank are subject to various regulatory restrictions relating to the payment of dividends, including requirements to

maintain capital at or above regulatory minimums, and to remain “well-capitalized” under the prompt corrective action

regulations. BB&T does not expect that any of these laws, regulations or policies will materially affect the ability of Branch

Bank to pay dividends.

BB&T is subject to various regulatory capital requirements administered by the Federal banking agencies. Failure to meet

minimum capital requirements can initiate certain mandatory—and possibly additional discretionary—actions by regulators

that, if undertaken, could have a direct material effect on the financial statements. Under capital adequacy guidelines and the

regulatory framework for prompt corrective action, the Company must meet specific capital guidelines that involve

quantitative measures of assets, liabilities and certain off-balance-sheet items calculated pursuant to regulatory directives.

BB&T’s capital amounts and classification also are subject to qualitative judgments by the regulators about components, risk

weightings and other factors. BB&T is in full compliance with these requirements. Banking regulations also identify five

capital categories for insured depository institutions: well-capitalized, adequately capitalized, undercapitalized, significantly

undercapitalized and critically undercapitalized. At December 31, 2013 and 2012, BB&T and Branch Bank were classified as

“well-capitalized.”

Quantitative measures established by regulation to ensure capital adequacy require BB&T to maintain minimum amounts and

ratios of total and Tier 1 capital (as defined in the regulations) to risk-weighted assets (as defined), and of Tier 1 capital to

average tangible assets (leverage ratio).

Risk-based capital ratios, which include Tier 1 Capital, Total Capital and Tier 1 Common Equity, are calculated based on

regulatory guidance related to the measurement of capital and risk-weighted assets. During the second quarter of 2013,

BB&T completed its reevaluation process related to calculating risk-weighted assets and determined that certain additional

adjustments were required in order to conform to regulatory guidance. These adjustments resulted in an increase to risk-

weighted assets and a decrease in BB&T’s risk-based capital ratios.

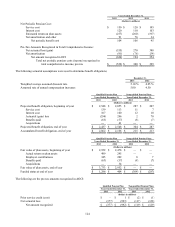

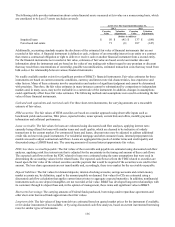

December 31, 2013 December 31, 2012

Actual Capital Capital Requirements Actual Capital Capital Requirements

Ratio Amount Minimum Well-Capitalized Ratio Amount Minimum Well-Capitalized

(Dollars in millions)

Tier 1 Capital:

BB&T 11.8 % $ 16,074 $ 5,460 $ 8,189 10.5 % $ 14,373 $ 5,455 $ 8,182

Branch Bank 11.9 15,785 5,315 7,973 11.2 14,587 5,202 7,803

Total Capital:

BB&T 14.3 19,514 10,919 13,649 13.4 18,267 10,909 13,637

Branch Bank 13.4 17,872 10,631 13,288 13.0 16,866 10,404 13,005

Leverage Capital:

BB&T 9.3 16,074 6,897 8,621 8.2 14,373 7,001 8,751

Branch Bank 9.4 15,785 5,058 8,429 8.6 14,587 5,099 8,498

As an approved seller/servicer, Branch Bank is required to maintain minimum levels of shareholders’ equity, as specified by

various agencies, including the United States Department of Housing and Urban Development, GNMA, FHLMC and FNMA.

At December 31, 2013 and 2012, Branch Bank’s equity was above all required levels.