BB&T 2013 Annual Report Download - page 141

Download and view the complete annual report

Please find page 141 of the 2013 BB&T annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

139 -

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

146 -

147

147 -

148

148 -

149

149 -

150

150 -

151

151 -

152

-

153

-

154

-

155

-

156

-

157

-

158

|

|

141

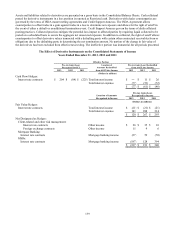

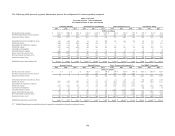

The following table presents information about BB&T's cash flow hedges:

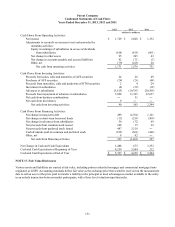

December 31,

2013 2012

(Dollars in millions)

Cash flow hedges:

N

et unrecognized afte

r

-tax gain (loss), including both active and terminated

hedges, on derivatives classified as cash flow hedges recorded in OCI $ 2 $ (173)

Estimated after-tax gain (loss) to be reclassified from OCI into earnings during the

next 12 months, including active hedges and hedges that were terminated

early for which the forecasted transactions are still probable (50) (37)

Maximum length of time over which the entity has hedged a portion of its

variability in future cash flows for forecasted transactions excluding those

transactions relating to the payment of variable interest on existing financial

instruments. 7 yrs ― yrs

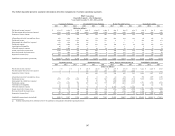

The following table presents information about BB&T's terminated hedge activity:

Year Ended December 31,

2013 2012

(Dollars in millions)

Cash flow hedges:

Pre-tax deferred gain from terminated cash flow hedges recorded in OCI $ 198 $ ―

Fair value hedges:

Pre-tax deferred gain from terminated fair value hedges related to long-term debt ― 85

Pre-tax reduction of interest expense recognized from previously

unwound fair value debt hedges 89 256

Derivatives Credit Risk – Dealer Counterparties

Credit risk related to derivatives arises when amounts receivable from a counterparty exceed those payable to the same

counterparty. The risk of loss is addressed by subjecting dealer counterparties to credit reviews and approvals similar to those

used in making loans or other extensions of credit and by requiring collateral. Dealer counterparties operate under agreements

to provide cash and/or liquid collateral when unsecured loss positions exceed negotiated limits.

Derivative contracts with dealer counterparties settle on a monthly, quarterly or semiannual basis, with daily movement of

collateral between counterparties required within established netting agreements. BB&T only transacts with dealer

counterparties that are national market makers with strong credit ratings.

Derivatives Credit Risk – Central Clearing Parties

Certain derivatives are cleared through central clearing parties that require initial margin collateral, as well as additional

collateral for trades in a net loss position. Initial margin collateral requirements are established by central clearing parties on

varying bases, with such amounts generally designed to offset the risk of non-payment. Initial margin is generally calculated

by applying the maximum loss experienced in value over a specified time horizon to the portfolio of existing trades. The

central clearing party used for TBA transactions does not post variation margin to the bank.