BB&T 2013 Annual Report Download - page 71

Download and view the complete annual report

Please find page 71 of the 2013 BB&T annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

|

|

71

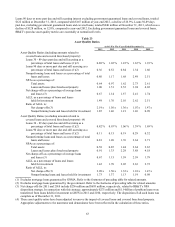

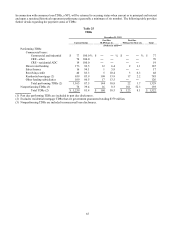

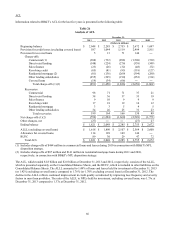

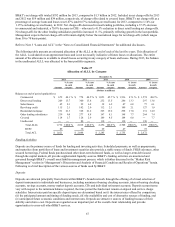

BB&T has established the following general practices to manage credit risk:

limiting the amount of credit that individual lenders may extend to a borrower;

establishing a process for credit approval accountability;

careful initial underwriting and analysis of borrower, transaction, market and collateral risks;

ongoing servicing and monitoring of individual loans and lending relationships;

continuous monitoring of the portfolio, market dynamics and the economy; and

periodically reevaluating the bank’s strategy and overall exposure as economic, market and other relevant conditions

change.

The following discussion presents the principal types of lending conducted by BB&T and describes the underwriting

procedures and overall risk management of BB&T’s lending function.

Underwriting Approach

Recognizing that the loan portfolio is a primary source of profitability and risk, proper loan underwriting is critical to

BB&T’s long-term financial success. BB&T’s underwriting approach is designed to define acceptable combinations of

specific risk-mitigating features that ensure credit relationships conform to BB&T’s risk philosophy. Provided below is a

summary of the most significant underwriting criteria used to evaluate new loans and loan renewals:

Cash flow and debt service coverage—cash flow adequacy is a necessary condition of creditworthiness, meaning

that loans must either be clearly supported by a borrower’s cash flow or, if not, must be justified by secondary

repayment sources.

Secondary sources of repayment—alternative repayment funds are a significant risk-mitigating factor as long as they

are liquid, can be easily accessed and provide adequate resources to supplement the primary cash flow source.

Value of any underlying collateral—loans are generally secured by the asset being financed. Because an analysis of

the primary and secondary sources of repayment is the most important factor, collateral, unless it is liquid, does not

justify loans that cannot be serviced by the borrower’s normal cash flows.

Overall creditworthiness of the customer, taking into account the customer’s relationships, both past and current,

with BB&T and other lenders—BB&T’s success depends on building lasting and mutually beneficial relationships

with clients, which involves assessing their financial position and background.

Level of equity invested in the transaction—in general, borrowers are required to contribute or invest a portion of

their own funds prior to any loan advances.

Commercial Loan and Lease Portfolio

The commercial loan and lease portfolio represents the largest category of the Company’s total loan portfolio. BB&T’s

commercial lending program is generally targeted to serve small-to-middle market businesses with sales of $250 million or

less. In addition, BB&T’s Corporate Banking Group provides lending solutions to large corporate clients. Traditionally,

lending to small and mid-sized businesses has been among BB&T’s strongest market segments.

Commercial and small business loans are primarily originated through BB&T’s Community Bank. In accordance with the

Company’s lending policy, each loan undergoes a detailed underwriting process, which incorporates BB&T’s underwriting

approach, procedures and evaluations described above. Commercial loans are typically priced with an interest rate tied to

market indices, such as the prime rate or LIBOR. Commercial loans are individually monitored and reviewed for any possible

deterioration in the ability of the client to repay the loan. Approximately 90% of BB&T’s commercial loans are secured by

real estate, business equipment, inventories and other types of collateral.