BB&T 2013 Annual Report Download - page 138

Download and view the complete annual report

Please find page 138 of the 2013 BB&T annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

139 -

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

146 -

147

147 -

148

148 -

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

|

|

138

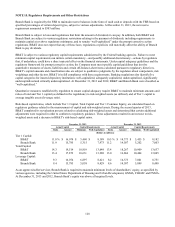

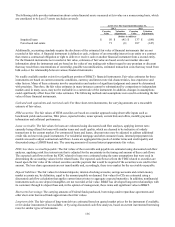

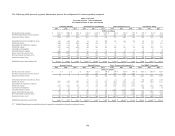

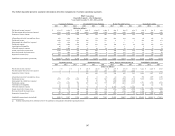

NOTE 18. Derivative Financial Instruments

Derivative Classifications and Hedging Relationships

December 31, 2013 December 31, 2012

Hedged Item or Notional Fair Value Notional Fair Value

Transaction Amount Gain Loss Amount Gain Loss

(Dollars in millions)

Cash flow hedges:

Interest rate contracts:

Pay fixed swaps 3 mo. LIBOR funding $ 4,300 $ ― $ (203) $ 6,035 $ ― $ (298)

Fair value hedges:

Interest rate contracts:

Receive fixed swaps and option trades Long-term debt 6,822 102 (3) 800 182 ―

Pay fixed swaps Commercial loans 178 ― (3) 187 ― (7)

Pay fixed swaps Municipal securities 345 ― (83) 345 ― (153)

Total 7,345 102 (89) 1,332 182 (160)

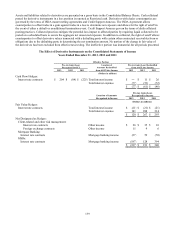

N

ot designated as hedges:

Client-related and other risk management:

Interest rate contracts:

Receive fixed swaps 8,619 370 (37) 9,352 687 ―

Pay fixed swaps 8,401 31 (396) 9,464 ― (717)

Other 2,010 8 (10) 3,400 24 (28)

Foreign exchange contracts 384 2 (3) 534 4 (3)

Total 19,414 411 (446) 22,750 715 (748)

Mortgage banking:

Interest rate contracts:

Interest rate lock commitments 1,869 3 (14) 6,064 55 (1)

When issued securities, forward rate agreements and forward

commitments 3,100 34 (7) 8,886 10 (19)

Other 531 8 (7) 215 6 (2)

Total 5,500 45 (28) 15,165 71 (22)

MSRs:

Interest rate contracts:

Receive fixed swaps 6,139 36 (141) 5,178 110 (27)

Pay fixed swaps 5,449 89 (29) 5,389 7 (94)

Option trades 9,415 181 (31) 14,510 363 (88)

Futures contracts ― ― ― 30 ― ―

When issued securities, forward rate agreements and forward

commitments 1,756 ― (3) 2,406 2 ―

Total 22,759 306 (204) 27,513 482 (209)

Total nonhedging derivatives 47,673 762 (678) 65,428 1,268 (979)

Total derivatives $ 59,318 864 (970) $ 72,795 1,450 (1,437)

Gross amounts not offset in the Consolidated Balance Sheets:

Amounts subject to master netting arrangements not offset due to policy election (514) 514 (797) 797

Cash collateral (received) posted (44) 386 (41) 607

N

et amount $ 306 $ (70) $ 612 $ (33)