BB&T 2013 Annual Report Download - page 15

Download and view the complete annual report

Please find page 15 of the 2013 BB&T annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

|

|

15

U.S. Implementation of Basel III

In July 2013, the FRB published final rules establishing a new comprehensive capital framework for U.S. banking

organizations. These rules implement the BCBS's December 2010 framework, known as “Basel III,” for strengthening

international capital standards as well as certain provisions of the Dodd-Frank Act. The rules substantially revise the risk-

based capital requirements applicable to BHCs and depository institutions, including BB&T and Branch Bank, compared to

the current U.S. risk-based capital rules. The rules define the components of capital and address other issues affecting the

numerator in banking institutions' regulatory capital ratios. The rules also address risk weights and other issues affecting the

denominator in banking institutions' regulatory capital ratios and replace the existing risk-weighting approach, which was

derived from Basel I capital accords of the BCBS, with a more risk-sensitive approach based, in part, on the standardized

approach in the BCBS's 2004 “Basel II” capital accords. The Basel III rules also implement the requirements of Section 939A

of the Dodd-Frank Act to remove references to credit ratings from the federal banking agencies' rules. At December 31, 2013,

BB&T would be considered a standardized approach banking organization and must comply with the new requirements

beginning on January 1, 2015. Institutions with greater than $250 billion in assets or $10 billion in foreign assets would be

considered an advanced approach banking organization, which requires a more conservative calculation of risk-weighted

assets, with a compliance date of January 1, 2014.

The Basel III rules, among other things, (1) introduce a new capital measure referred to as common equity Tier 1; (2) specify

that Tier 1 capital consist of Tier 1 common equity and additional Tier 1 capital instruments meeting specified requirements;

(3) define Tier 1 common equity narrowly by requiring that most deductions/adjustments to regulatory capital measures be

made to Tier 1 common equity and not to the other components of capital; and (4) expand the scope of the

deductions/adjustments from capital as compared to existing regulations.

The Basel III rules prescribe a standardized approach for risk weightings that expand the risk-weighting categories from the

current four Basel I-derived categories (0%, 20%, 50% and 100%) to a much larger and more risk-sensitive number of

categories, depending on the nature of the assets, generally ranging from 0% for U.S. government and agency securities, to

600% for certain equity exposures, resulting in higher risk weights for a variety of asset categories. More conservative risk-

weighting of certain residential mortgage loans and the requirement to recognize in capital the value of unrecognized gains

and losses in AFS securities were not retained. In addition, the rules provide more advantageous risk weights for derivatives

and repurchase-style transactions cleared through a qualifying central counterparty and increase the scope of eligible

guarantors and eligible collateral for purposes of credit risk mitigation.

The Basel III rules revise the “prompt corrective action” directives by establishing certain ratio levels for well-capitalized

status. In addition to the minimum risk-based capital requirements, all banks must hold additional capital, the capital

conservation buffer, to avoid being subject to limits on capital distributions, such as dividend payments, discretionary

payments on Tier 1 instruments, share buybacks, and certain discretionary bonus payments to executive officers, including

heads of major business lines and similar employees. The required amount of the capital conservation buffer will be phased-

in annually through January 1, 2019.

In November 2013, the FDIC, FRB and OCC released a joint statement providing a notice of proposed rulemaking

concerning the U.S. implementation of the liquidity coverage ratio rule. BB&T is currently evaluating the impact and has

developed a program to ensure compliance with the applicable requirements. BB&T is implementing balance sheet changes

to support its compliance with the rule. These actions include changing the mix of its investment portfolio to include more

GNMA and U.S. Treasury securities, which qualify as Level 1 under the rule, and changing its deposit mix to reduce public

funds deposits and increase retail and commercial deposits.

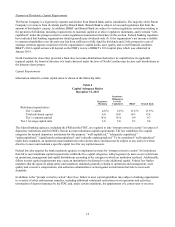

The following table summarizes the capital requirements and BB&T’s internal targets under Basel III:

Table 3

Capital Under Basel III

Minimum Well- Minimum Capital Plus Capital Conservation Buffer BB&T

Capital Capitalized 2016 2017 2018 2019 (1) Target

Common equity Tier 1 to risk-weighted assets 4.5 % 6.5 % 5.125 % 5.750 % 6.375 % 7.000 % 8.5 %

Tier 1 capital to risk-weighted assets 6.0 8.0 6.625 7.250 7.875 8.500 10.0

Total capital to risk-weighted assets 8.0 10.0 8.625 9.250 9.875 10.500 12.0

Leverage ratio 4.0 5.0 N/A N/A N/A N/A 7.0

(1) Represents BB&T's goal upon the effective date of Basel III on January 1, 2015.