BB&T 2013 Annual Report Download - page 135

Download and view the complete annual report

Please find page 135 of the 2013 BB&T annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

139 -

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

|

|

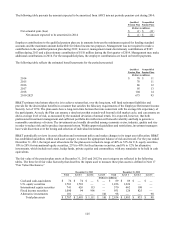

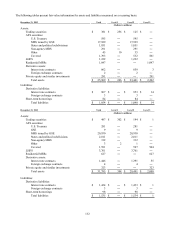

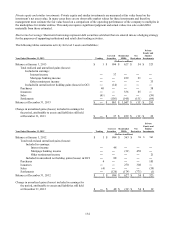

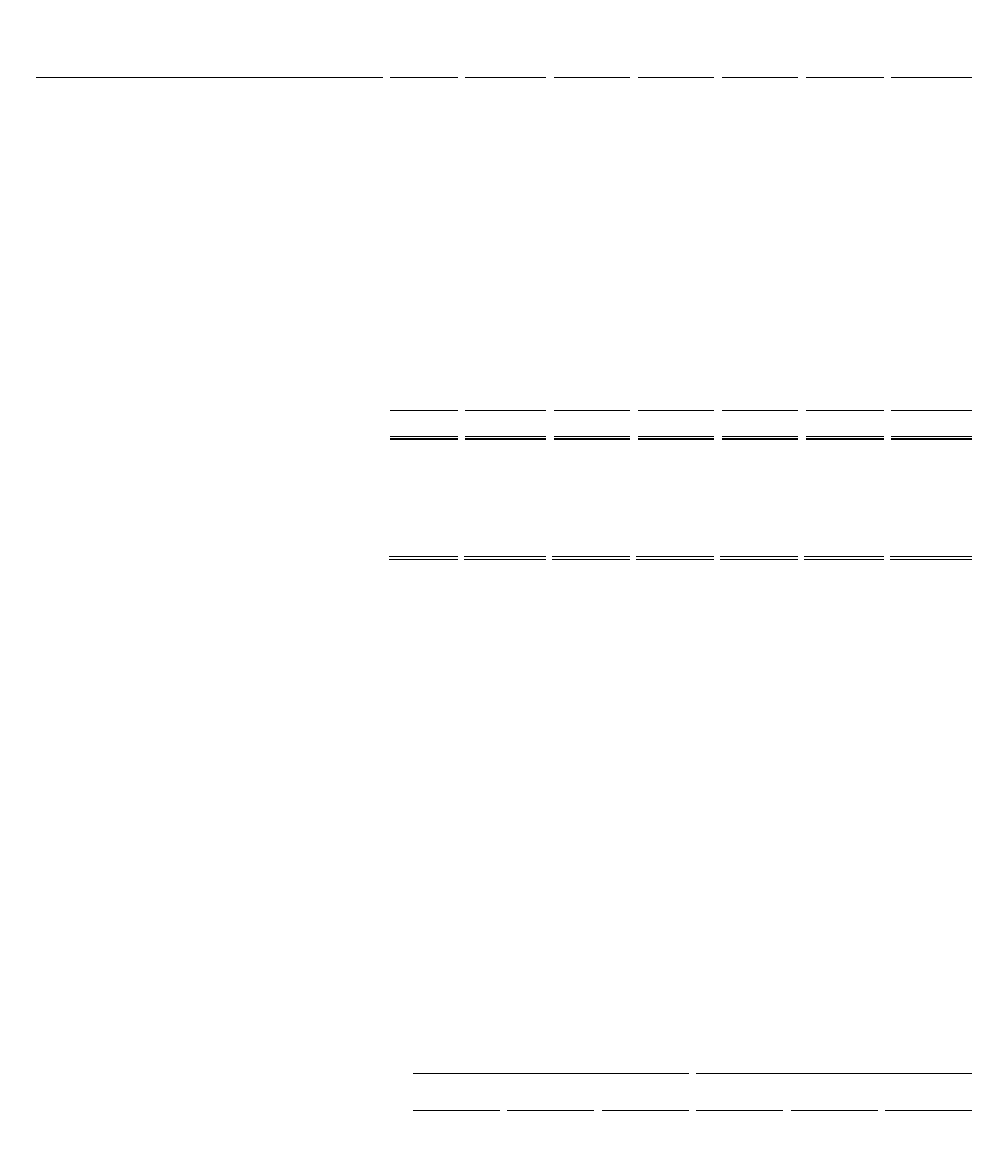

135

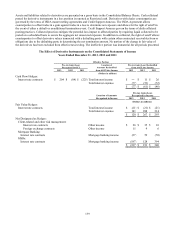

Private

States & Equity and

Political Other Covered Residential Net Similar

Year Ended December 31, 2011 Trading Subdivisions Securities Securities MSRs Derivatives Investments

(Dollars in millions)

Balance at January 1, 2011 $ 11 $ 119 $ 7 $ 954 $ 830 $ (25) $ 266

Total realized and unrealized gains (losses):

Included in earnings:

Interest income ― ― ― 54 ― ― ―

Mortgage banking income ― ― ― ― (341) 151 ―

Other noninterest income (3) ― ― ― ― ― 64

Included in OCI ― (9) (1) 24 ― ― ―

Purchases 7 ― ― ― ― ― 61

Issuances ― ― ― ― 225 110 ―

Sales (14) ― ― ― ― ― (112)

Settlements ― (53) (1) (48) (151) (177) (15)

Transfers into Level 3 ― ― ― ― ― ― 1

Transfers out of Level 3 ― (57) (5) ― ― ― (4)

Balance at December 31, 2011 $ 1 $ ― $ ― $ 984 $ 563 $ 59 $ 261

Change in unrealized gains (losses)

included in earnings for the period,

attributable to assets and liabilities

still held at December 31, 2011 $ ― $ ― $ ― $ 54 $ (341) $ 59 $ 39

BB&T’s policy is to recognize transfers in and transfers out of Levels 1, 2 and 3 as of the end of a reporting period. During

the years ended December 31, 2013 and 2012, BB&T did not have any material transfer of securities between levels in the

fair value hierarchy. During the year ended December 31, 2011, BB&T transferred certain state and political subdivision

securities out of Level 3 as a result of management’s decision to reclassify them from AFS to HTM classification, which is

not recorded at fair value. There were no gains or losses recognized as a result of this transfer.

BB&T’s private equity and similar investments are primarily in SBIC qualified funds, which focus on equity and

subordinated debt investments in privately-held middle market companies. These investments generally are not redeemable

and distributions are received as the underlying assets of the funds liquidate. The timing of distributions, which are expected

to occur on various dates through 2025, is uncertain and dependent on various events such as recapitalizations, refinance

transactions and ownership changes among others. Excluding the investment of future funds, BB&T estimates these

investments have a weighted average remaining life of approximately three years; however, the timing and amount of

distributions may vary significantly. As of December 31, 2013, restrictions on the ability to sell the investments include, but

are not limited to, consent of a majority member or general partner approval for transfer of ownership. BB&T’s investments

are spread over numerous privately-held middle market companies, and thus the sensitivity to a change in fair value for any

single investment is limited. The significant unobservable inputs for these investments are EBITDA multiples that ranged

from 2x to 10x, with a weighted average of 7x, at December 31, 2013.

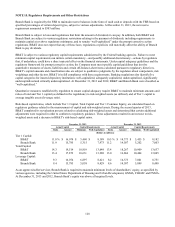

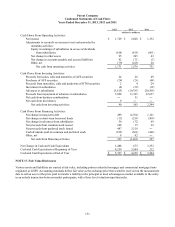

The following table details the fair value and UPB of LHFS that were elected to be carried at fair value:

December 31, 2013 December 31, 2012

Fair Aggregate Fair Aggregate

Value UPB Difference Value UPB Difference

(Dollars in millions)

LHFS reported at fair value $ 1,222 $ 1,223 $ (1) $ 3,761 $ 3,652 $ 109

Excluding government guaranteed, there were no LHFS that were nonaccrual or 90 days or more past due and still accruing

interest.