BB&T 2013 Annual Report Download - page 70

Download and view the complete annual report

Please find page 70 of the 2013 BB&T annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

|

|

70

Shareholders’ Equity

Shareholders’ equity totaled $22.8 billion at December 31, 2013, an increase of $1.6 billion, or 7.5%, from year-end 2012.

Book value per common share at December 31, 2013 was $28.52, compared to $27.21 at December 31, 2012.

The increase in shareholders’ equity during 2013 includes $487 million in net proceeds from the issuance of Tier 1 qualifying

non-cumulative perpetual preferred stock. See Note 9 “Shareholders’ Equity” in the “Notes to Consolidated Financial

Statements” herein for additional information. In addition, shareholders’ equity increased $915 million due to net income in

excess of dividends declared, and $233 million as a result of the issuance of additional shares and other transactions in

connection with equity-based compensation plans, the 401(k) plan and the dividend reinvestment plan. The net loss in AOCI

increased $34 million, primarily due to a $640 million after-tax net decrease in the value of the AFS securities portfolio,

partially offset by improvements of $411 million related to pensions and other post-retirement benefit plans and $175 million

related to changes in unrealized net gains on cash flow hedges.

Tangible book value per common share at December 31, 2013 was $18.08 compared to $16.53 at December 31, 2012. As of

December 31, 2013, measures of tangible capital were not required by the regulators and, therefore, were considered non-

GAAP measures. Refer to the section titled “Capital” herein for a discussion of how BB&T calculates and uses these

measures in the evaluation of the Company.

Risk Management

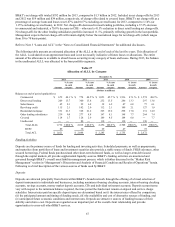

BB&T has defined and established an enterprise-wide risk culture that places an emphasis on effective risk management

through a strong tone at the top by the Board of Directors and Executive Management, accountability at all levels of the

organization, an effective challenge environment and incentives to encourage strong risk management behavior. The risk

culture promotes judicious risk-taking and discourages rampant revenue generation without consideration of corresponding

risks. It is part of BB&T’s mission statement that risk is managed to optimize the long-term return to shareholders, while

providing a safe and sound investment. Risk management begins with the LOBs, and as such, BB&T has established clear

expectations for the LOBs in regards to the identification, monitoring, reporting and response to current and emerging risks.

Centrally, risk oversight is managed at the corporate level through oversight, policies and reporting.

The Board of Directors and Executive Management established BB&T’s risk culture and promoted appropriate risk-taking

behaviors. It is the responsibility of senior leadership to clearly communicate the organizational values that support the

desired risk culture, recognize and reward behavior that reflects the defined risk culture and monitor and assess the current

risk culture of BB&T. Regardless of financial gain or loss, employees are held accountable if they do not follow the

established risk management policies and procedures. BB&T’s risk culture encourages transparency and open dialogue

between all levels in the performance of bank functions, such as the development, marketing and implementation of a product

or service. An effective challenge environment is reflected in BB&T’s decision-making processes.

The Chief Risk Officer leads the RMO, which designs, organizes and manages BB&T’s risk framework. The RMO is

responsible for ensuring effective risk management oversight, measurement, monitoring, reporting and consistency. The

RMO has direct access to the Board of Directors and Executive Management to communicate any risk issues (identified or

emerging) as well as the performance of the risk management activities throughout the Company. The principal types of

inherent risk include regulatory, credit, liquidity, market, operational, reputation and strategic risks.

Compliance risk

Compliance risk is the risk to earnings, capital, or reputation arising from violations of, or noncompliance with, current and

changing laws, regulations, supervisory guidance or regulatory expectations.

Credit risk

Credit risk is the risk to earnings or capital arising from the default, inability or unwillingness of a borrower, obligor, or

counterparty to meet the terms of any financial obligation with BB&T or otherwise perform as agreed. Credit risk exists in all

activities where success depends on the performance of a borrower, obligor, or counterparty. Credit risk arises when BB&T

funds are extended, committed, invested, or otherwise exposed through actual or implied contractual agreements, whether on

or off the balance sheet. Credit risk also occurs when the credit quality of an issuer whose securities or other instruments the

bank holds deteriorates.