BB&T 2013 Annual Report Download - page 57

Download and view the complete annual report

Please find page 57 of the 2013 BB&T annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

|

|

57

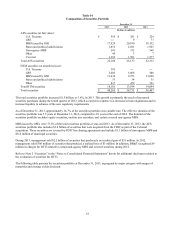

Lending Activities

The primary goal of the BB&T lending function is to help clients achieve their financial goals by providing quality loan

products that are fair to the client and profitable to the Company. Management believes that this purpose can best be

accomplished by building strong, profitable client relationships over time, with BB&T becoming an important contributor to

the prosperity and well-being of its clients. In addition to the importance placed on client knowledge and continuous

involvement with clients, BB&T’s lending process incorporates the standards of a consistent company-wide credit culture

and an in-depth local market knowledge. Furthermore, the Company employs strict underwriting criteria governing the

degree of assumed risk and the diversity of the loan portfolio in terms of type, industry and geographical concentration. In

this context, BB&T strives to meet the credit needs of businesses and consumers in its markets while pursuing a balanced

strategy of loan profitability, loan growth and loan quality.

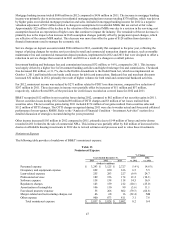

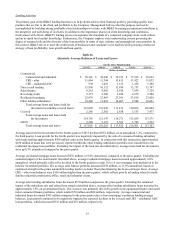

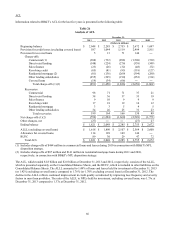

Table 16

Quarterly Average Balances of Loans and Leases

For the Three Months Ended

12/31/13 9/30/13 6/30/13 3/31/13 12/31/12

(Dollars in millions)

Commercial:

Commercial and industrial $ 38,101 $ 38,446 $ 38,359 $ 37,916 $ 38,022

CRE - other 11,494 11,344 11,411 11,422 11,032

CRE - residential ADC 970 1,022 1,121 1,238 1,398

Direct retail lending 15,998 16,112 15,936 15,757 15,767

Sales finance 9,262 8,992 8,520 7,838 7,724

Revolving credit 2,357 2,308 2,268 2,279 2,280

Residential mortgage 23,979 23,403 23,391 23,618 23,820

Other lending subsidiaries 10,448 11,018 10,407 9,988 10,051

Total average loans and leases held for

investment (excluding covered loans) 112,609 112,645 111,413 110,056 110,094

Covered 2,186 2,502 2,858 3,133 3,477

Total average loans and leases held

for investment 114,795 115,147 114,271 113,189 113,571

LHFS 2,206 3,118 3,581 3,792 3,532

Total average loans and leases $ 117,001 $ 118,265 $ 117,852 $ 116,981 $ 117,103

Average loans held for investment for the fourth quarter of 2013 declined $352 million, or an annualized 1.2%, compared to

the third quarter. Loan growth for the fourth quarter was negatively impacted by the sale of a consumer lending subsidiary

with loans totaling approximately $500 million early in the fourth quarter. In connection with this transaction, approximately

$230 million of loans that were previously reported within the other lending subsidiaries portfolio were transferred to the

residential mortgage loan portfolio. Excluding the impact of the loan sale described above, average loans held for investment

were up 0.3% annualized compared to the prior quarter.

Average residential mortgage loans increased $576 million, or 9.8% annualized, compared to the prior quarter. Excluding the

estimated impact of the loan transfer described above, average residential mortgage loans increased approximately 6.0%

annualized, which primarily reflects the decision in the fourth quarter to retain 10 to 15 year mortgage loan production in the

held for investment portfolio. The average sales finance portfolio increased $270 million, or 11.9% annualized, based on

continued strength in the prime automobile lending market as dealer floor plan financing has been a strategic focus. Average

CRE – other loan balances were $150 million higher than the prior quarter, which reflects growth in lending related to multi-

family residential construction, office, retail and industrial clients.

Average other lending subsidiaries loans decreased $570 million compared to the prior quarter. Excluding the estimated

impact of the subsidiary sale and related loan transfer described above, average other lending subsidiaries loans increased by

approximately 3.5% on an annualized basis. This increase was primarily driven by growth in the equipment finance and small

ticket consumer finance portfolios, which totaled $70 million and $84 million, respectively. Average commercial and

industrial loans decreased $345 million compared to the prior quarter due to lower mortgage warehouse lending average

balances. Loan growth continued to be negatively impacted by expected declines in the covered and CRE – residential ADC

loan portfolios, which decreased $316 million and $52 million, respectively.