BB&T 2013 Annual Report Download - page 73

Download and view the complete annual report

Please find page 73 of the 2013 BB&T annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

|

|

73

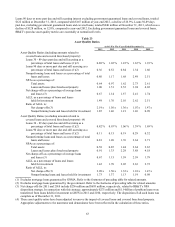

BB&T’s other lending subsidiaries adhere to the same overall underwriting approach as the commercial and consumer

lending portfolio and also utilize automated credit scoring to assist with underwriting credit risk. The majority of these loans

are relatively homogenous and no single loan is individually significant in terms of its size and potential risk of loss. The

majority of the loans are secured by real estate, automobiles, equipment or unearned insurance premiums. As of December

31, 2013, included in the other lending subsidiaries portfolio are loans to nonprime borrowers of approximately $2.8 billion,

or 2.4% of the total BB&T loan and lease portfolio.

Covered Loan Portfolio

BB&T has $2.0 billion of loans covered by loss sharing agreements with the FDIC, which are primarily CRE and residential

mortgage loans. Refer to Note 3 “Loans and ACL” in the “Notes to Consolidated Financial Statements” in this report for

additional disclosures related to BB&T’s covered loans.

Liquidity risk

Liquidity risk is the risk to ongoing operations arising from the inability to accommodate liability maturities or deposit

withdrawals, fund asset growth, or meet contractual obligations when they come due. For additional information concerning

BB&T’s management of liquidity risk, see the “Liquidity” section of “Management’s Discussion and Analysis” herein.

Market risk

Market risk is the risk to earnings or capital arising from changes in the market value of portfolios, securities, or other

financial instruments due to changes in the level, volatility, or correlations among financial market rates or prices, including

interest rates, foreign exchange rates, equity prices, or other relevant rates or prices. For additional information concerning

BB&T’s management of market risk, see the “Market Risk Management” section of “Management’s Discussion and

Analysis” herein.

Operational risk

Operational risk is the risk to earnings or capital arising from inadequate or failed internal processes, people and systems or

from external events. This definition includes legal risk, which is the risk of loss arising from defective transactions, litigation

or claims made, or the failure to adequately protect company-owned assets.

Reputation risk

Reputation risk is the risk to earnings, capital, enterprise value, the BB&T brand, and public confidence arising from negative

publicity or public opinion, whether real or perceived, regarding BB&T’s business practices, products and services,

transactions, or other activities undertaken by BB&T, its representatives, or its partners. Reputation risk may impact BB&T’s

clients, employees, communities or shareholders, and is often a residual risk that arises when other risks are not managed

properly.

Strategic risk

Strategic risk is the risk to earnings, capital, enterprise value, and to the achievement of BB&T’s Vision, Mission, Purpose,

and business objectives that arises from BB&T’s business strategy, adverse business decisions, improper or ineffective

implementation of decisions, or lack of responsiveness to changes in business environment. Strategic risk is a function of the

compatibility of BB&T’s strategic goals, the business strategies developed to achieve those goals, the resources deployed

against these goals, and the quality of implementation.

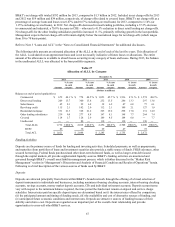

Market Risk Management

The effective management of market risk is essential to achieving BB&T’s strategic financial objectives. As a financial

institution, BB&T’s most significant market risk exposure is interest rate risk in its balance sheet; however, market risk also

includes product liquidity risk, price risk and volatility risk in BB&T’s LOBs. The primary objectives of market risk

management are to minimize any adverse effect that changes in market risk factors may have on net interest income, net

income and capital and to offset the risk of price changes for certain assets recorded at fair value. At BB&T, market risk

management also includes the enterprise-wide IPV function.