BB&T 2013 Annual Report Download - page 14

Download and view the complete annual report

Please find page 14 of the 2013 BB&T annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

|

|

14

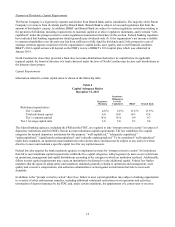

Payment of Dividends; Capital Requirements

The Parent Company is a legal entity separate and distinct from Branch Bank and its subsidiaries. The majority of the Parent

Company’s revenue is from dividends paid by Branch Bank. Branch Bank is subject to laws and regulations that limit the

amount of dividends it can pay. In addition, BB&T and Branch Bank are subject to various regulatory restrictions relating to

the payment of dividends, including requirements to maintain capital at or above regulatory minimums, and to remain “well-

capitalized” under the prompt corrective action regulations summarized elsewhere in this section. Federal banking regulators

have indicated that banking organizations should generally pay dividends only if (1) the organization’s net income available

to common shareholders over the past year has been sufficient to fully fund the dividends and (2) the prospective rate of

earnings retention appears consistent with the organization’s capital needs, asset quality and overall financial condition.

BB&T’s 2014 capital actions will depend on the FRB’s review of BB&T’s 2014 capital plan, which was submitted in

January 2014.

North Carolina law states that, provided a bank does not make distributions that reduce its capital below its applicable

required capital, the board of directors of a bank chartered under the laws of North Carolina may declare such distributions as

the directors deem proper.

Capital Requirements

Information related to certain capital ratios is shown in the following table:

Table 2

Capital Adequacy Ratios

December 31, 2013

Regulatory

Minimum

Regulatory

Minimum to

be Well-

Capitalized BB&T Branch Bank

Risk-based capital ratios:

Tier 1 capital 4.0 % 6.0 % 11.8 % 11.9 %

Total risk-based capital 8.0 10.0 14.3 13.4

Tier 1 common capital N/A N/A 9.9 9.7

Tier 1 leverage capital ratio 3.0 5.0 9.3 9.4

The federal banking agencies, including the FRB and the FDIC, are required to take “prompt corrective action” in respect of

depository institutions and their BHCs that do not meet minimum capital requirements. The law establishes five capital

categories for insured depository institutions for this purpose: “well-capitalized,” “adequately capitalized,”

“undercapitalized,” “significantly undercapitalized” and “critically undercapitalized.” To be considered “well-capitalized”

under these standards, an institution must maintain the ratios shown above and must not be subject to any order or written

directive to meet and maintain a specific capital level for any capital measure.

Federal law also requires the bank regulatory agencies to implement systems for “prompt corrective action” for institutions

that fail to meet minimum capital requirements within the five capital categories, with progressively more severe restrictions

on operations, management and capital distributions according to the category in which an institution is placed. Additionally,

failure to meet capital requirements may cause an institution to be directed to raise additional capital. Federal law further

mandates that the agencies adopt safety and soundness standards generally relating to operations and management, asset

quality and executive compensation, and authorizes administrative action against an institution that fails to meet such

standards.

In addition to the “prompt corrective action” directives, failure to meet capital guidelines may subject a banking organization

to a variety of other enforcement remedies, including additional substantial restrictions on its operations and activities,

termination of deposit insurance by the FDIC and, under certain conditions, the appointment of a conservator or receiver.