BB&T 2013 Annual Report Download - page 64

Download and view the complete annual report

Please find page 64 of the 2013 BB&T annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

|

|

64

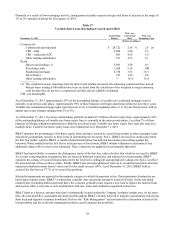

BB&T’s potential problem loans include loans on nonaccrual status or past due as disclosed in Table 22. In addition, for its

commercial portfolio segment, loans that are rated special mention or substandard performing are closely monitored by

management as potential problem loans. Refer to Note 3 “Loans and ACL” in the “Notes to Consolidated Financial

Statements” herein for additional disclosures related to these potential problem loans.

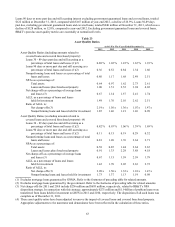

TDRs generally occur when a borrower is experiencing, or is expected to experience, financial difficulties in the near-term.

As a result, BB&T will work with the borrower to prevent further difficulties, and ultimately to improve the likelihood of

recovery on the loan. To facilitate this process, a concessionary modification that would not otherwise be considered may be

granted resulting in classification of the loan as a TDR. Refer to Note 1 “Summary of Significant Accounting Policies” in the

“Notes to Consolidated Financial Statements” for additional policy information regarding TDRs.

BB&T’s performing TDRs, excluding government guaranteed mortgage loans, totaled $1.3 billion at December 31, 2013,

essentially flat compared to the prior year. During 2012, a national bank regulatory agency issued guidance that requires

certain loans, which have been discharged in bankruptcy and not reaffirmed by the borrower, to be accounted for as TDRs

and possibly as nonperforming, regardless of their actual payment history and expected performance. In connection with the

issuance of this guidance, BB&T classified $226 million and $44 million of performing and nonperforming loans,

respectively, as TDRs during the fourth quarter of 2012. All loans subsequently discharged in bankruptcy have been

evaluated and classified as performing or nonperforming TDRs based on an evaluation of historical and expected payment

performance.

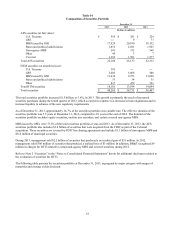

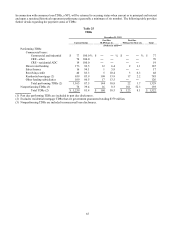

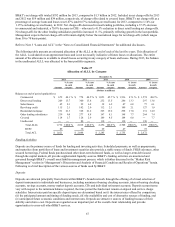

The following table provides a summary of performing TDR activity:

Table 24

Rollforward of Performing TDRs

Years Ended December 31,

2013 2012

(Dollars in millions)

Balance at beginning of year $ 1,327 $ 1,109

Inflows 489 417

Change in regulatory guidance ― 226

Payments and payoffs (208) (187)

Charge-offs (41) (36)

Transfers to nonperforming TDRs, net (65) (50)

Removal due to the passage of time (108) (109)

N

on-concessionary re-modifications (41) (43)

Removed in connection with the sale of a consumer lending subsidiary (24) ―

Balance at end of year $ 1,329 $ 1,327

Payments and payoffs represent cash received from borrowers in connection with scheduled principal payments, prepayments

and payoffs of amounts outstanding. Transfers to nonperforming TDRs represent loans that no longer meet the requirements

necessary to reflect the loan in accruing status and as a result are subsequently classified as a nonperforming TDR.

TDRs may be removed due to the passage of time if they: (1) did not include a forgiveness of principal or interest, (2) have

performed in accordance with the modified terms (generally a minimum of six months), (3) were reported as a TDR over a

year end reporting period, and (4) reflected an interest rate on the modified loan that was no less than a market rate at the date

of modification. These loans were previously considered TDRs as a result of structural concessions such as extended interest-

only terms or an amortization period that did not otherwise conform to normal underwriting guidelines.

In addition, certain transactions may be removed from classification as a TDR as a result of a subsequent non-concessionary

re-modification. Non-concessionary re-modifications represent TDRs that did not contain concessionary terms at the date of a

subsequent renewal/modification and there was a reasonable expectation that the borrower would continue to comply with

the terms of the loan subsequent to the date of the re-modification. A re-modification may be considered for such a re-

classification if the loan has not had a forgiveness of principal or interest and the modified terms qualify as more than minor

such that the re-modified loan is considered a new loan. Alternatively, such loans may be considered for reclassification in

years subsequent to the date of the re-modification based on the passage of time as described in the preceding paragraph.