BB&T 2013 Annual Report Download - page 80

Download and view the complete annual report

Please find page 80 of the 2013 BB&T annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

|

|

80

Related Party Transactions

The Company may extend credit to its officers and directors in the ordinary course of business. These loans are made under

substantially the same terms as comparable third-party lending arrangements and are in compliance with applicable banking

regulations.

Capital

The maintenance of appropriate levels of capital is a management priority and is monitored on a regular basis. BB&T’s

principal goals related to the maintenance of capital are to provide adequate capital to support BB&T’s risk profile consistent

with the Board-approved risk appetite, provide financial flexibility to support future growth and client needs, comply with

relevant laws, regulations, and supervisory guidance, achieve optimal credit ratings for BB&T and its subsidiaries and

provide a competitive return to shareholders.

Management regularly monitors the capital position of BB&T on both a consolidated and bank level basis. In this regard,

management’s overriding policy is to maintain capital at levels that are in excess of the operating capital guidelines, which

are above the regulatory “well capitalized” levels. Management has implemented stressed capital ratio minimum guidelines

to evaluate whether capital ratios calculated with planned capital actions are likely to remain above minimums specified by

the FRB for the annual CCAR. Breaches of stressed minimum guidelines prompt a review of the planned capital actions

included in BB&T’s capital plan.

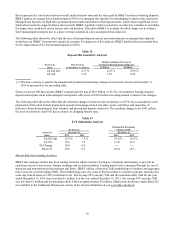

Table 36

BB&T's Internal Capital Guidelines Prior to Basel III

Operating Stressed

Tier 1 Capital Ratio 10.0 % 7.5 %

Total Capital Ratio 12.0 9.5

Tier 1 Leverage Capital Ratio 7.0 5.0

Tangible Capital Ratio 6.0 4.0

Tier 1 Common Equity Ratio 8.5 6.0

Payments of cash dividends to BB&T’s shareholders and repurchases of common shares are the methods used to manage any

excess capital generated. In addition, management closely monitors the Parent Company’s double leverage ratio (investments

in subsidiaries as a percentage of shareholders’ equity) with the intention of maintaining the ratio below 125%. The active

management of the subsidiaries’ equity capital, as described above, is the process used to manage this important driver of

Parent Company liquidity and is a key element in the management of BB&T’s capital position.

The capital of BB&T’s subsidiaries is regularly monitored to determine if the levels that management believes are the most

beneficial and efficient for their operations are maintained. Management intends to maintain capital at Branch Bank at levels

that will result in classification as “well-capitalized” for regulatory purposes. Secondarily, it is management’s intent to

maintain Branch Bank’s capital at levels that result in regulatory risk-based capital ratios that are generally comparable with

peers of similar size, complexity and risk profile. If the capital levels of Branch Bank increase above these guidelines, excess

capital may be transferred to the Parent Company, subject to regulatory and other operating considerations, in the form of

special dividend payments.

While nonrecurring events or management decisions may result in the Company temporarily falling below its operating

minimum guidelines for one or more of these ratios, it is management’s intent through capital planning to return to these

targeted operating minimums within a reasonable period of time. Such temporary decreases below the operating minimums

shown above are not considered an infringement of BB&T’s overall capital policy provided a return above the minimums is

forecast to occur within a reasonable time period.

On March 14, 2013, the FRB informed BB&T that it objected to certain qualitative elements of its capital plan. BB&T

resubmitted its plan on June 11, 2013. On August 23, 2013, BB&T announced that the FRB did not object to the Company’s

revised plan.

Risk-based capital ratios, which include Tier 1 Capital, Total Capital and Tier 1 Common Equity, are calculated based on

regulatory guidance related to the measurement of capital and risk-weighted assets.

BB&T’s Tier 1 common equity ratio was 9.9% at December 31, 2013 compared to 9.0% at December 31, 2012. The increase

in regulatory capital was primarily due to strong capital generation during 2013.