Philips 2008 Annual Report Download - page 107

Download and view the complete annual report

Please find page 107 of the 2008 Philips annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

|

|

The aggregate Funded Status is least sensitive to

interest rate risk. This reflects the LDI strategies in

the Netherlands and the UK and the relatively large

fixed income allocations in Germany. The biggest

sensitivity to interest rates exists in the US plan. This

is attributable to the interest rate mismatch between

its assets and liabilities. The overall sensitivity to

longevity is comparable to the sensitivity to equity

prices. The Dutch fund contributes most, which is due

to its size.

The aggregate NPPC is particularly sensitive to

changes in interest rates and inflation expectations.

This can be explained by the interest and inflation

sensitivity of NPPC in the Netherlands. NPPC is less

sensitive to changes in equity valuations and longevity.

Due to its absolute exposure to equities, the biggest

sensitivity to equities still exists in the Netherlands.

The biggest sensitivity to longevity also exists in

the Netherlands.

Stochastic analysis

The sensitivities described above reflect the

impacts of separate changes in equity prices, interest

rates, etc. As such changes are unlikely to happen

simultaneously, a simple summation of the above-

mentioned sensitivities would overestimate the

total risk exposure. The difference between the total

risk and that summation represents the so-called

diversification effect. It results from the less than

perfect (or even negative) correlation between the

respective risk factors. The diversification effect may

be captured by a stochastic analysis, i.e. by analyzing

the outcomes of a large number of simulations.

These simulations are based on the volatility of and

correlations between the respective risk factors

over the past 30 years. The bar charts on the right

show the maximum deviations from the expected

aggregate Funded Status as per year-end 2008 and

year-end 2009, and the expected NPPC for 2009 and

2010, if the 5% worst possible outcomes are excluded.

These “Funded-Status-at-Risk” and “NPPC-at-Risk”

measures are based on the valuations of plan assets

and liabilities on December 31, 2007 and December

31, 2008, respectively, and may therefore be seen as

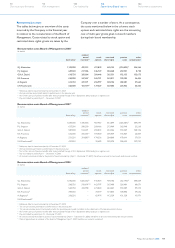

indicators of the risks on these same dates. Figure 5

shows both the contribution of the separate risk

factors and the diversification effect. Contrary to

figures 1 and 2, it excludes the impact of longevity

risk, but it includes the impact of credit risk (for 2008

only) and foreign exchange risk. Figures 6 and 7 show

both the contributions of the risk exposures in the

four biggest pension countries and the diversification

between them.

Figure 5

Factor decomposition of the 5%

Funded-Status-at-Risk

in millions of euros

(

1,500

)

(

1,000

)

(

500

)

0

5

0

0

1

,

000

1

,5

00

2

,

000

2,

5

00

20082007

diversi

f

ication

t

ota

l

r

i

s

k

equ

i

ty r

i

s

k

i

nterest rate r

i

s

k

forei

g

n exchan

g

e ris

k

i

n

f

lation risk

c

redit ris

k

Figure 6

Country decomposition of the 5%

Funded-Status-at-Risk

in millions of euros

(1

,

000)

(

500

)

0

500

1,000

1

,5

00

2,

000

20082007

t

ota

l

r

i

s

k

d

iversi

f

icatio

n

United Kingdom

N

etherland

s

U

nited State

s

G

erman

y

Figure 7

Country decomposition of the 5% NPPC-at-Risk

in millions of euros

total

r

isk

20082007

diversi

f

ication United Kingdom

N

etherland

s

(

75

)

0

75

150

22

5

U

nited States

G

erman

y

Philips Annual Report 2008 107

122

Performance statements

114

Supervisory Board report

110

Our leadership

94

Risk management

70

Our sector performance