Philips 2008 Annual Report Download - page 8

Download and view the complete annual report

Please find page 8 of the 2008 Philips annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

2 -

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

|

|

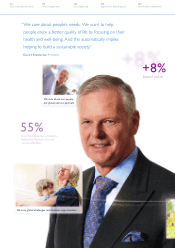

Message from

the President

Dear stakeholder

2008 was not exactly the year of progress that you

and I had envisaged for Philips 12 months ago. Our

company’s transformation over the last few years has

definitely produced a balanced, stronger and more

resilient set of businesses active in the field of health

and well-being, and these continued to improve their

position in the market in 2008. But the acceleration

of the economic downturn in the course of the year,

particularly in the fourth quarter, took an increasing

toll on several of our businesses that are sensitive

to early cycle effects, especially those with direct

or indirect consumer market exposure, requiring

us to take decisive action.

Nevertheless there has been progress on several

fronts. With the successful integration of the two

largest acquisitions in Philips’ history – Respironics

and Genlyte – more than 50% of our revenue is

generated from businesses with global leadership

positions; up from less than 40% in 2007. And a

steady 31% of our sales continues to come from

emerging markets. All that supported by a quality

brand that gained 8% in value in 2008 alone and

a workforce

reaching high-performance benchmark

engagement levels.

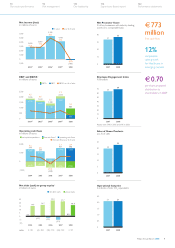

Performance

The increased strength and resilience of our business

portfolio was particularly evident in Healthcare,

which, in a very challenging operating environment,

achieved excellent results – higher comparable sales

and an improvement in underlying EBITA – and is on

the way to becoming our largest sector.

The strong downturn in the latter part of 2008

affected the Group’s top line, particularly at Consumer

Lifestyle and in our OEM businesses in Lighting, partly

offset by continued healthy growth at Healthcare,

leading to a moderate overall sales decline of 2.7%.

EBITA was down on 2007, largely due to a decline

in sales-driven earnings at Consumer Lifestyle and

Lighting, as well as an asbestos-related settlement

charge. We also extended and accelerated the

restructuring and change programs across our

Healthcare, Consumer Lifestyle and Lighting sectors,

further impacting EBITA. These programs are on

track to deliver cost savings of approximately

EUR 400 million on an annual basis, with effect

from the second half of 2009.

We also moved quickly to extend our cash management

initiatives, including rigorous management of working

capital. This enabled us to end the year with a robust

balance sheet supported by strong operating cash

flows of almost EUR 1.5 billion.

Furthermore, we continued with the responsible

sell-down of our non-core financial holdings by

divesting our final holding in TSMC, as well as further

reducing our stake in LG Display. The economic

malaise affected the market value of our remaining

financial stakes, causing us to write down EUR

1.4

billion on the value of our current financial holdings.

The road ahead

We remain fully committed to our primary financial

objective of doubling EBITA per share, and will

continue to drive forward our plans in this respect.

However, the rapid and severe deterioration in the

business environment means we no longer expect

to be able to realize this goal in 2010.

We remain fully committed to our primary

financial objective – to double EBITA per share

For the mature markets in Western Europe and the

US – and most emerging markets – we foresee very

difficult conditions throughout 2009. Nonetheless,

I firmly believe that the overall strength of our business

portfolio, coupled with our strong balance sheet and

tight focus on cost and cash management, will enable

us to weather the current turmoil and make the most

of the economic upturn when it comes.

69%

Employee Engagement Index

Philips Annual Report 20088

18

We care about...

8

Message from

the President

6

Performance highlights

14

Who we are

42

Our group performance