Philips 2008 Annual Report Download - page 89

Download and view the complete annual report

Please find page 89 of the 2008 Philips annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

|

|

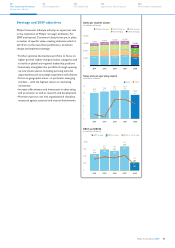

Sales per market cluster

in millions of euros

7,000

6,000

5,000

4,000

3,000

2,000

1,000

0

2004 2005 2006 2007 2008

Western Europe North America other mature

key emerging other emerging

1,773

4,526

1,828

4,775

2,022

5,466

2,436

6,093

2,560

564 652

835

1,012

1,084

845 941

1,072

1,216

1,255

1,051 1,057 1,194 1,125

1,936

7,106

271

293 297 343 304

Sales and net operating capital

in billions of euros

Sales NOC

8

6

4

2

0

4.5

1.5

2004

4.8

2.5

2005

5.5

2.5

2006

6.1

3.9

2007

7.1

5.6

2008

EBIT

a

n

d

EBIT

A

in millions of euro

s

2004 2005 2006 2007 2008

EBITA in valueEBIT in value EBITA as a % of sales

508

499

10.6 608

577

11.1 722

675

11.9

165

542

12.0

541

0

2

00

400

6

00

800

538

7.6

in the automotive and construction segments, partly

offset by positive contributions from acquisitions.

2007 included EUR 55 million of restructuring and

acquisition-related charges.

EBIT amounted to EUR 165 million, compared to

EUR 675 million in 2007. In 2008, a EUR 232 million

non-cash goodwill impairment charge for Lumileds

was recorded, primarily due to weaker demand in

the automotive, displays and mobile phone segments.

Cash flow before financing activities included cash

disbursements of EUR 1,826 million, mainly related to

the acquisition of Genlyte, whereas in 2007 acquisition-

related disbursements amounted to EUR 1,162 million,

mainly in connection with the acquisitions of PLI and

Color Kinetics. Excluding these acquisition-related

payments, cash flow before financing activities increased

by EUR 173 million compared to 2007 thanks to improved

working capital requirements. Net capital expenditures

increased by EUR 54 million compared to 2007, largely

due to higher investments in solid-state lighting solutions.

Strategy and 2009 objectives

Philips Lighting will play an important role in the

realization

of Philips’ strategic ambitions. For 2009 and

beyond, Lighting has put in place a number of specific

value-creating initiatives which it will drive via the axes

Drive performance, Accelerate change and Implement strategy.

The five value drivers that we believe will strengthen

our competitive advantage and help safeguard our

leading position in lighting are:

growth – driven by acquisitions, Green value

•

propositions, innovative solutions, LEDs/solid-state

lighting and emerging markets

segment leadership – by driving the development •

of our market segments through channels and

multi-stakeholder partnerships

brand franchise – by leveraging category •

management and our brand equity

new business models – by creating new ways •

of working and new forms of revenue generation

intellectual property – in particular by developing •

the solid-state lighting market through a dedicated

IP licensing program.

Philips Annual Report 2008 89

122

Performance statements

114

Supervisory Board report

110

Our leadership

94

Risk management

70

Our sector performance

Lighting