Philips 2008 Annual Report Download - page 11

Download and view the complete annual report

Please find page 11 of the 2008 Philips annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

2 -

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

|

|

Take decisive steps to structurally deal with

unsatisfactory EBITA margins in Connected

Displays (Television)

In North America we entered into a five-year

minimum brand licensing agreement with Funai

Electric Company of Japan, under which Funai will

assume responsibility for all Philips-branded consumer

television activities in the United States and Canada.

Toward the end of the year this agreement was

extended, adding audio-video categories in the US

and TV and audio-video categories in Mexico.

... decisive action to address profitability ...

We drove further portfolio reductions around the

world, for instance in Australia, New Zealand and

South Africa, and announced our withdrawal from

plasma-based TVs. We also signed a letter of intent

regarding our PC Monitors business, creating a brand

licensing agreement with TPV Technology for the

global distribution and marketing of IT Display products.

Given the current economic turmoil, we will continue

to evaluate whether more action is required in 2009.

Going forward, we have a solid TV business – with

leadership positions in selected geographic markets

– that is driven by innovation and margin rather

than volume.

Improve productivity as a driver for margin

expansion

Our progress on this point was limited as our efficiency

programs were mitigated by lower earnings in our

operational sectors due to the economic downturn.

The restructuring and change programs across our

sectors will put us in a stronger position, but productivity

remains a key focus point for management.

Step up resource investment in developing

markets to accelerate growth in excess of 2x GDP

In 2008, we further increased our talent, marketing

and R&D investments towards the emerging markets.

In addition, we made a number of acquisitions in

Brazil, China and India, designed to strengthen our

position in healthcare in emerging markets.

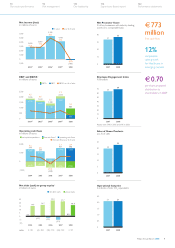

... emerging market sales growth of 12% and 8%

in Healthcare and Lighting respectively ...

Excluding Television, which we manage for margin

instead of volume, our sales growth in emerging markets

amounted to 6%, approximately in line with the latest

2x world GDP growth estimates. I am particularly

pleased with the way our Healthcare and Lighting

businesses weathered the economic downturn, with

comparable sales growth of 12% and 8% respectively

in the emerging markets for the year.

Increase innovation focus in support of Philips’

growth ambition

In 2008, sales of innovative products – i.e. products

introduced within the last year (for B2C products)

or three years (for B2B products) – amounted to 58%

of total sales, again up 2 percentage points and more

than double the 2003 level, but still not giving us the

amount of new business we are looking for.

In difficult economic times like these, innovation is

more crucial than ever to provide a competitive edge.

In 2009 we will therefore – notwithstanding our focus

on cash management – sustain our spending levels on

R&D and marketing, while intensifying our efforts to

increase the speed and productivity of innovation.

Sustainability continues to be a key driver of

innovation. Sales of Green Products rose

to 23%

of overall sales, up from 20% in 2007, representing

an

important, growing part of our revenue stream.

Our investment in Green Innovations amounted to

over EUR 280 million in 2008, on track for a cumulative

amount of EUR 1 billion to be invested by 2012.

Continue to drive a culture of superior

customer experience

Ensuring a superior customer experience is absolutely

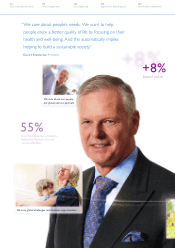

crucial to the realization of our ambitions. The Net

Promoter Score (NPS) is our single key metric of

customer experience. NPS measures the answer to

one simple question: “How likely is it that you would

recommend this company/product to a friend or

colleague?” Compared to 2007, we achieved NPS

leadership in an additional 4% of our businesses on

a comparable basis. During 2008, we also expanded

the NPS measurement to now cover all our strategic

areas, and at present 47% of our key businesses have

industry-leading scores. Especially notable is our strong

performance in the emerging markets such as Brazil,

Russia, India and China. We are still committed to

reach our 2010 NPS target and to this end we will drive

customer experience improvement and execute strategic

moves to continue to secure leading NPS positions.

We also realized 8% growth of our total brand value

in the annual ranking of the top-100 global brands

compiled by Interbrand – the fifth increase in a row.

In 2004, when we launched our “sense and simplicity”

brand campaign, Philips’ total brand value was USD

4.4 billion. This has steadily increased to a total value

of USD 8.3 billion in 2008. Such consistent improvement

clearly illustrates that our “sense and simplicity”

brand promise, founded on deep, validated insights

into customer and end-user needs, continues to

resonate with customers.

23%

of sales came from

Green Products

58%

of sales came from

innovative products

introduced in the

last three years

Philips Annual Report 2008 11

122

Performance statements

114

Supervisory Board report

110

Our leadership

94

Risk management

70

Our sector performance