Philips 2008 Annual Report Download - page 108

Download and view the complete annual report

Please find page 108 of the 2008 Philips annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

|

|

Details of fiscal risks

Philips is, as mentioned before, exposed to fiscal

uncertainties. This section further describes this

exposure. Please refer to note 6 and note 42 for

additional disclosure relating to income taxes.

Transfer pricing uncertainties

Philips has issued transfer pricing directives, which

are in accordance with guidelines of the Organization

of Economic Co-operation and Development. As

transfer pricing has a cross-border effect, the focus of

local tax authorities on implemented transfer pricing

procedures in a country may have an impact on results

in another country. In order to mitigate the transfer

pricing uncertainties, audits are executed on a regular

basis to safeguard the correct implementation of the

transfer pricing directives.

Tax uncertainties on general service agreements

and specific allocation contracts

Due to the centralization of certain activities in

a limited number of countries (such as research and

development, centralized IT, and corporate functions

and head office), costs are also centralized. As a

consequence, for tax reasons these costs and/or

revenues must be allocated to the beneficiaries,

i.e. the various Philips entities. For that purpose,

apart from specific allocation contracts for costs and

revenues, general service agreements (GSAs) are

signed with a large number of entities. Tax authorities

review the implementation of GSAs, apply benefit

tests for particular countries or audit the use of tax

credits attached to GSAs and royalty payments, and

may reject the implemented procedures. Furthermore,

buy in/out situations in the case of (de)mergers could

affect the tax allocation of GSAs between countries.

The same applies to the specific allocation contracts.

Tax uncertainties due to disentanglements

and acquisitions

When a subsidiary of Philips is disentangled, or a new

company is acquired, related tax uncertainties arise.

Philips creates merger and acquisition (M&A) teams

for these disentanglements or acquisitions. These

teams consist of specialists from various corporate

functions and are formed, amongst other things, to

identify hidden tax uncertainties that could

subsequently surface when companies are acquired

and to avoid tax claims related to disentangled

entities. These tax uncertainties are investigated and

assessed to mitigate tax uncertainties in the future

as much as possible. Several tax uncertainties may

surface from M&A activities. Examples of uncertainties

are: applicability of the participation exemption,

allocation issues, and non-deductibility of parts of

the purchase price.

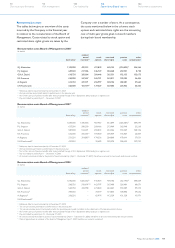

The differences between the first and second bars

in figures 5, 6 and 7 reflect plan changes, changes in

assumptions for discounting future liabilities and

changes in financial market conditions during 2008.

The Funded-Status-at-Risk has decreased compared

to 2007. The additional steps taken during 2008 in the

Netherlands and the US to fully implement their new

investment strategies have led to lower contributions

of interest rate and equity risk. The contribution

of equity risk has also decreased due to the lower

absolute exposure that resulted from negative market

returns in 2008. Nevertheless, equity risk is still a

major source of risk. It results from the relatively

large strategic allocation to equities in the US and

the large absolute exposure to equities in the Dutch

fund. The contribution of interest rate risk results

from the remaining interest rate mismatch between

assets and liabilities. Both in absolute and relative

terms, it is biggest in the US. Credit risk results mainly

from the mismatch between the credit spread risk

exposure of (the discount rate curve used for valuing)

liabilities and the credit exposure of assets (through

defaults, downgrades and changing credit spreads).

The Dutch fund contributes most to inflation risk, due

to its size and its indexation policy. Foreign exchange

risk has increased compared to 2007, as the increased

deficits in the UK and especially the US lead to higher

translation risks. The diversification effect is largely

attributable to the positive correlation between

inflation and interest rates and the negative correlation

between bonds and equities.

The Dutch fund still contributes most to NPPC-at-Risk.

This is a reflection of its size.

Philips Annual Report 2008108

42

Our group performance

18

We care about...

8

Message from

the President

6

Performance highlights

14

Who we are