Philips 2008 Annual Report Download - page 214

Download and view the complete annual report

Please find page 214 of the 2008 Philips annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

204 -

205

205 -

206

206 -

207

207 -

208

208 -

209

209 -

210

210 -

211

211 -

212

212 -

213

213 -

214

214 -

215

215 -

216

216 -

217

217 -

218

218 -

219

219 -

220

220 -

221

221 -

222

222 -

223

223 -

224

224 -

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

|

|

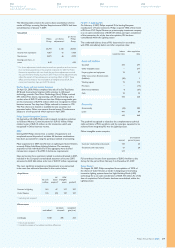

IFRIC Interpretation 11 ‘Group and Treasury Share Transactions

IFRIC 11 requires a share-based payment arrangement in which an

entity receives goods or services as consideration for its own equity

instruments to be accounted for as an equity-settled share-based

payment transaction, regardless of how the equity instruments are

obtained. IFRIC 11 was applied by the Company in its 2008 financial

statements. The application of IFRIC 11 did not have any impact

on the Company’s consolidated financial statements.

IFRIC Interpretation 12 ‘Service Concession Arrangements’

IFRIC 12 provides guidance on certain recognition and measurement

issues that arise in accounting for public-to-private service concession

arrangements. IFRIC 12 was applied by the Company on January 1,

2008. IFRIC 12 did not have a material impact on the Company’s

consolidated financial statements.

IFRIC Interpretation 14 ‘The Limit on a Defined Benefit Asset, Minimum

Funding Requirements and their Interaction’

IFRIC 14 addresses (1) when refunds or reductions in future

contributions should be regarded as ‘available’ in the context

of paragraph 58 of IAS 19 Employee Benefits; (2) how a minimum

funding requirement might affect the availability of reductions in

future contributions; and (3) when a minimum funding requirement

might give rise to a liability. This interpretation was applied by the

Company on January 1, 2008. The effect of the application of this

Interpretation is disclosed in Note 56 to the IFRS financial statements.

IFRS accounting standards effective as from 2009 and onwards

A number of amendments and revisions to standards and interpretations

are not yet effective for the year ended December 31, 2008, and have

not been applied in preparing these consolidated financial statements:

Amendments to IAS 1 ‘Presentation of Financial Statements’

The amendments to IAS 1 mainly concern the presentation of

changes in equity, in which changes as a result of the transaction with

shareholders should be presented separately and for which a different

format of the overview of the changes in equity can be selected.

Furthermore, an opening balance sheet of the corresponding period

is presented where restatements have occurred. Philips has chosen

to present all non-owner changes in equity in two statements

(a separate income statement and a statement of comprehensive

income). This Standard is applicable to the Company on January 1, 2009.

Amendments to IAS 32 ‘Financial instruments: Presentation’ and IAS 1

‘Presentation of Financial Statements - Puttable Financial Instruments

and Obligations Arising on Liquidation’

The amendments to IAS 32 and IAS 1 are relevant to entities

that have issued financial instruments that are (i) puttable financial

instruments or (ii) instruments, or components of instruments, that

impose on the entity an obligation to deliver to another party a

pro-rata share of the net assets of the entity on liquidation. Under

the revised IAS 32, subject to specified criteria being met, these

instruments will be classified equity. These amendments are applicable

to the Company on January 1, 2009. The Company expects that

application of this amendment will not have a material impact on

the Company’s consolidated financial statements.

Amendment to IAS 39 ‘Financial Instruments: Recognition and

Measurement – Eligible Hedged Items’

The amendment to IAS 39 provides additional guidance on the

designation of a hedged item. The amendment clarifies how the

existing principles underlying hedge accounting should be applied

in two particular situations. It clarifies the designation of a one-sided

risk in a hedged item and inflation in a financial hedged item. This

amendment is applicable to the Company on January 1, 2010. The

application of this amendment will not have a material impact on

the Company’s consolidated financial statements.

Amendments to IFRS 1 and IAS 27 ‘Cost of an investment

on first-time adoption’

The amendments to IFRS 1 and IAS 27, which will be applicable to

the Company on January 1, 2009, allows first-time adopters to use a

deemed cost of either fair value or the carrying amount under previous

accounting practice to measure the initial cost of investments in

subsidiaries, jointly controlled entities and associates in the separate

financial statements. The amendment also removed the definition

of the cost method from IAS 27 and replaced with a requirement to

present dividends as income in the separate financial statements of

the investor. This standard does not have any impact on the Company’s

consolidated financial statements.

Revision to IFRS 1 ‘First-time Adoption of IFRSs’

The revision to IFRS 1 improves the structure of the Standard

but does contain any technical changes. The revisions are designed

to make the Standard clearer and easier to follow and to better

accommodate future changes to the Standard. This revision is

applicable to the Company on January 1, 2010 but will not have

an impact on the Company’s consolidated financial statements.

Amendments to IFRS 2 ‘Share-based Payment - Vesting Conditions

and Cancellations’

The amendments to IFRS 2, which will be applicable to the Company

on January 1, 2009, clarify the definition of vesting conditions and

the accounting treatment of cancellations by the counterparty to

a shared-based arrangement. The Company expects that this

amendment will not have a material impact on the Company’s

consolidated financial statements.

Revision to IFRS 3 ‘Business Combinations’

The revised standard incorporates the following changes that

are likely to be relevant to the Company’s operations:

The definition of a business has been broadened, which is likely to

•

result in more acquisitions being treated as business combinations.

Contingent consideration will be measured at fair value, with the

•

subsequent changes therein recognized in statement of income.

Transaction costs, other than share and debt issue costs, will be

•

expensed as incurred.

Any pre-existing interest in the acquiree will be measured at fair

•

value with gain or loss recognized in the income statement.

Any non-controlling (minority) interest will be measured at either

•

fair value, or at its proportionate interest in the identifiable assets

and liabilities of the acquiree, on a transaction-by-transaction basis.

The revision to IFRS 3 is mandatory for the Company’s business

combinations beginning January 1, 2010 and will have no impact

on prior periods.

Amendments to IAS 27 ‘Consolidated and Separate Financial Statements’

The amendments to IAS 27 require accounting for changes in ownership

interest by the Company in a subsidiary, while maintaining control, to

be recognized as an equity transaction. When the Company loses

control of a subsidiary, any interest retained in the former subsidiary

will be measured at fair value with the gain or loss recognized in the

statement of income. The amendments to IAS 27 will be applicable

to the Company on January 1, 2010. These are not expected to have

significant impact on the consolidated financial statements.

Improvements to IFRS 2008

The improvements published under the IASB’s annual improvement

process are intended to deal with non-urgent, minor amendments

to the standards. Most of the improvements are applicable to the

Company on January 1, 2010, some on January 1, 2009.

The improvements to IFRS 2008 relate mainly to the following:

Disclosure requirements: Classification as held for sale of the

•

assets and liabilities of a subsidiary where the parent is commited

to a plan to sell its controlling interest but intends to retain a

non-controlling interest.

Reclass to inventories of PP&E previously held for rental when the

•

assets cease to be rented and are held for sale, and the recognition

of the proceeds of disposal of such assets as revenue.

Recognition of a government grant arising from government

•

loans at below-market interest.

Recognition of advertising and promotional expenditure as an

•

asset is not permitted beyond the point at which the entity has

the right to access the goods purchased or services received.

Classification of property under construction for investment •

purposes as investment property under IAS 40.

The Company has not yet determined the potential impact of those

improvements.

IFRIC Interpretation 13 ‘Customer Loyalty Programmes’

IFRIC 13 addresses recognition and measurement of the obligation to

provide free or discounted goods or services in the future. This

interpretation will be applicable to the Company on January 1, 2009.

The application of this interpretation will not have a material impact

on the Company’s consolidated financial statements.

Philips Annual Report 2008214

180

Sustainability performance

244

Company financial statements

124

US GAAP financial statements

192

IFRS financial statements

Significant IFRS accounting policies