Philips 2008 Annual Report Download - page 82

Download and view the complete annual report

Please find page 82 of the 2008 Philips annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

|

|

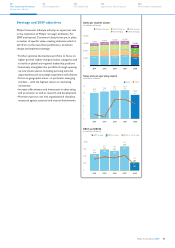

Key data

in millions of euros

2006 2007 2008

Sales 13,108 13,330 11,145

of which Television 6,559 6,270 4,980

Sales growth

% increase (decrease), nominal 42(16)

% increase (decrease), comparable

64(8)

Sales growth excl. Television

% increase (decrease), nominal –8(13)

% increase (decrease), comparable

(3) 10 (6)

EBITA 692 848 281

of which Television 155 (68) (413)

as a % of sales 5.3 6.4 2.5

EBIT 683 832 265

of which Television 155 (68) (413)

as a % of sales 5.2 6.2 2.4

Net operating capital (NOC) 910 890 728

of which Television (185) (255) (245)

Cash flows before financing activities

(39) 772 253

of which Television 207 (41) (489)

Employees (FTEs) 24,419 23,397 17,346

of which Television 7,262 6,855 4,943

For a reconciliation to the most directly comparable US GAAP measures,

see the chapter Reconciliation of non-US GAAP information

2008 financial performance

2008 presented very challenging market conditions for

Consumer Lifestyle. Sales amounted to EUR 11,145 million,

a nominal decline of 16% compared to 2007. Adjusted

for unfavorable currency effects of 3% and portfolio

changes, mainly the divestment of Television in North

America and the sale of the Set-Top Boxes and Mobile

Phones businesses, comparable sales declined by 8%.

Year-on-year declines were seen in all businesses, except

for 4% comparable growth in Domestic Appliances

and Health & Wellness. Television and Audio & Video

Multimedia suffered comparable double-digit declines.

Green Product sales totaled 1,478 million in 2008,

a nominal increase of 41% compared to 2007,

amounting to 13% of sector sales.

From a geographical perspective, Western Europe

and North America, which account for more than

half of the sector’s sales, were heavily impacted by the

economic downturn as well as by selective portfolio

and margin management. Sales growth was strong in

the key emerging markets, led by double-digit growth

in Brazil. Growth in Asia was driven by solid double-

digit growth across the countries in most businesses,

mostly offset by a decline in Television. European

emerging markets declined 14%.

EBITA as a percentage of sales decreased from 6.4%

in 2007 to 2.5% in 2008, due to declines in nearly all

businesses, mainly as a result of lower sales. EBITA

was impacted by EUR 195 million of restructuring

charges, partially offset by the EUR 63 million gain

on the sale of Set-Top Boxes.

EBIT declined from EUR 832 million (6.2% of sales)

in 2007 to EUR 265 million (2.4% of sales) in 2008.

Net operating capital was reduced by EUR 162 million

at the end of 2008 and amounted to EUR 728 million.

Cash flows before financing activities declined from

EUR 772 million in 2007 to an inflow of EUR 253

million, primarily driven by lower earnings.

Philips Annual Report 200882

42

Our group performance

18

We care about...

8

Message from

the President

6

Performance highlights

14

Who we are