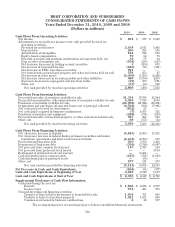

BB&T 2010 Annual Report Download - page 112

Download and view the complete annual report

Please find page 112 of the 2010 BB&T annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

|

|

Mortgage Servicing Rights

BB&T has two primary classes of mortgage servicing rights for which it separately manages the economic

risks: residential and commercial. Residential mortgage servicing rights are recorded on the Consolidated

Balance Sheets primarily at fair value with changes in fair value recorded as a component of mortgage banking

income each period. Commercial mortgage servicing rights are recorded as other assets on the Consolidated

Balance Sheets at the lower of cost or market and are amortized in proportion to, and over the estimated period,

that net servicing income is expected to be received based on projections of the amount and timing of estimated

future net cash flows. The amount and timing of estimated future net cash flows are updated based on actual

results and updated projections. BB&T periodically evaluates its commercial mortgage servicing rights for

impairment.

Equity-Based Compensation

BB&T maintains various equity-based compensation plans. These plans provide for the granting of stock

options (incentive and nonqualified), stock appreciation rights, restricted stock, restricted stock units,

performance units and performance shares to selected BB&T employees and directors. BB&T values share-based

awards at the grant date fair value and recognizes the expense over the requisite service period taking into

account retirement eligibility.

Changes in Accounting Principles and Effects of New Accounting Pronouncements

In June 2009, the Financial Accounting Standards Board (“FASB”) issued new guidance impacting Transfers

and Servicing. The objective of this guidance is to improve the relevance, representational faithfulness, and

comparability of the information that a reporting entity provides in its financial reports about a transfer of

financial assets; the effects of a transfer on its financial position, financial performance, and cash flows; and a

transferor’s continuing involvement in transferred financial assets. This guidance is effective for financial asset

transfers occurring after December 31, 2009. The adoption of this guidance was not material to BB&T’s

consolidated financial statements.

In June 2009, the FASB issued new guidance impacting Consolidation of variable interest entities. The

objective of this guidance is to improve financial reporting by enterprises involved with variable interest entities

and to provide more relevant and reliable information to users of financial statements. This guidance was

effective as of January 1, 2010. The adoption of this guidance was not material to BB&T’s consolidated financial

statements.

In February 2010, the FASB issued new guidance impacting Fair Value Measurements and Disclosures.

The new guidance requires a gross presentation of purchases and sales of Level 3 activities and adds a new

requirement to disclose transfers in and out of Level 1 and Level 2 measurements. The guidance related to the

transfers between Level 1 and Level 2 measurements was effective for BB&T on January 1, 2010. The guidance

that requires increased disaggregation of the level 3 activities is effective for BB&T on January 1, 2011. The new

disclosures required by this guidance are included in Note 19 to these consolidated financial statements.

In March 2010, the FASB issued new guidance impacting Receivables. The new guidance clarifies that a

modification to a loan that is part of a pool of loans that were acquired with deteriorated credit quality should not

result in the removal of the loan from the pool. This guidance is effective for any modifications of loans accounted

for within a pool in the first interim or annual reporting period ending after July 15, 2010. The adoption of this

guidance was not material to BB&T’s consolidated financial statements.

In July 2010, the FASB issued new guidance impacting Receivables. The new guidance requires additional

disclosures that will allow users to understand the nature of credit risk inherent in a company’s loan portfolios,

how that risk is analyzed and assessed in arriving at the allowance for loan and lease losses, and changes and

reasons for those changes in the allowance for loan and lease losses. The new disclosures that relate to

information as of the end of the reporting period are required as of December 31, 2010. The disclosures related to

activity that occurs during a reporting period are effective for reporting periods beginning on or after

December 15, 2010, except for the disclosure requirements relating to troubled debt restructurings, which have

been indefinitely delayed pending the outcome of the FASB’s deliberations related to the definition of a troubled

debt restructuring.

112