BB&T 2010 Annual Report Download - page 57

Download and view the complete annual report

Please find page 57 of the 2010 BB&T annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

|

|

evaluation must include consideration of the borrower’s sustained historical repayment performance for a

reasonable period (generally a minimum of six months) prior to the date on which the loan is returned to accrual

status. Sustained historical repayment performance for a reasonable time prior to the restructuring may be taken

into account.

In connection with consumer loan restructurings, a nonperforming loan will be returned to accruing status

when current as to principal and interest and upon a sustained historical repayment performance (generally a

minimum of six months).

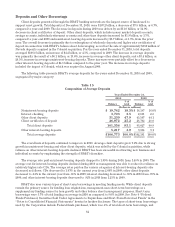

BB&T’s performing restructured loans, excluding government guaranteed mortgage loans, totaled $1.5

billion at December 31, 2010, an increase of $406 million compared with December 31, 2009. The majority of

BB&T’s commercial lending loan modifications that are considered restructurings involve an extension of the

term of the loan without a corresponding adjustment to the risk premium reflected in the interest rate. BB&T

does not typically lower the interest rate and rarely forgives principal or interest as part of a commercial loan

modification. In addition, BB&T frequently obtains additional collateral or guarantor support when modifying

such loans. For commercial loans, performing restructured loans totaled $657 million at December 31, 2010. These

loans are typically residential acquisition, development and construction loans where BB&T has extended the

maturity of the loan for less than one year without a sufficient corresponding increase in the interest rate, or

principal payments have been deferred to assist the borrower. The majority of BB&T’s mortgage and consumer

loan modifications that are considered restructurings involve a reduction in the interest rate to a below market

rate and/or an increase in the term of the loan without a corresponding adjustment to the risk premium reflected

in the interest rate. These modifications rarely result in the forgiveness of principal or interest.

Allowance for Loan and Lease Losses and Reserve for Unfunded Lending Commitments

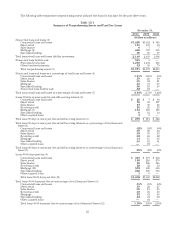

The allowance for loan and lease losses and the reserve for unfunded lending commitments compose BB&T’s

allowance for credit losses. The allowance for credit losses totaled $2.8 billion at December 31, 2010, an increase of

3.1% compared to $2.7 billion at the end of 2009. The allowance for loan and lease losses, as a percentage of loans

and leases held for investment, was 2.62% at December 31, 2010 (or 2.63% excluding covered loans), compared to

2.51% (or 2.72% excluding covered loans) at year-end 2009. The decline in the allowance as a percentage of loans

held for investment, excluding covered loans, reflects the improvement in the overall quality of the loan portfolio.

Please refer to Note 5 “Allowance for Loan and Lease Losses and Reserve for Unfunded Lending Commitments”

in the “Notes to Consolidated Financial Statements” for additional disclosures.

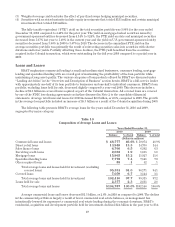

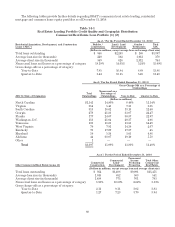

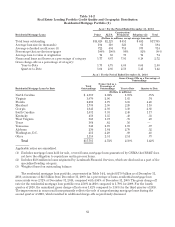

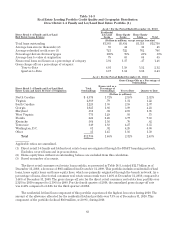

Information relevant to BB&T’s allowance for loan and lease losses for the last five years is presented in the

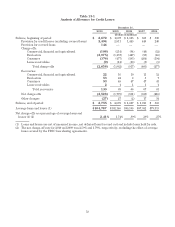

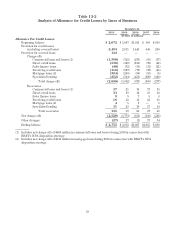

following tables. Table 13-1 is presented using regulatory classifications, which focuses on the underlying loan

collateral, and differs from internal classifications presented herein that focus on the lines of business that

generate the loans. Table 13-2 is presented based upon the lines of business, as discussed herein.

57