BB&T 2010 Annual Report Download - page 53

Download and view the complete annual report

Please find page 53 of the 2010 BB&T annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

|

|

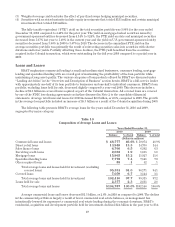

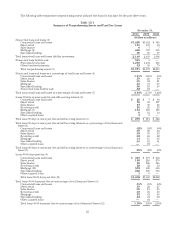

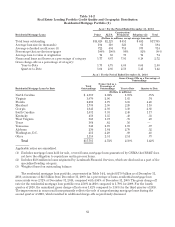

(3) Excludes foreclosed real estate totaling $313 million and $160 million as of December 31, 2010 and

December 31, 2009, respectively, that are covered by FDIC loss sharing agreements.

(4) Excludes mortgage loans guaranteed by GNMA that BB&T does not have the obligation to repurchase.

(5) Excludes loans past due 90 days or more that are covered by FDIC loss sharing agreements totaling $1.1

billion and $1.4 billion at December 31, 2010 and December 31, 2009, respectively.

(6) Excludes mortgage loans past due 90 days or more that are government guaranteed totaling $153 million, $8

million, $7 million, $1 million and $2 million at December 31, 2010, December 31, 2009, December 31, 2008,

December 31, 2007 and December 31, 2006, respectively.

(7) Excludes loans totaling $363 million and $391 million past due 30-89 days at December 31, 2010 and

December 31, 2009, respectively, that are covered by FDIC loss sharing agreements.

(8) Excludes mortgage loans past due 30-89 days that are government guaranteed totaling $83 million, $23

million, $25 million, $7 million and $5 million at December 31, 2010, December 31, 2009, December 31, 2008,

December 31, 2007 and December 31, 2006, respectively.

(9) These asset quality ratios have been adjusted to remove the impact of covered loans and covered foreclosed

property. Appropriate adjustments to the numerator and denominator have been reflected in the calculation

of these ratios. Management believes the inclusion of acquired loans in certain asset quality ratios that

include nonperforming assets, past due loans or net charge-offs in the numerator or denominator results in

distortion of these ratios and they may not be comparable to other periods presented or to other portfolios

that were not impacted by purchase accounting.

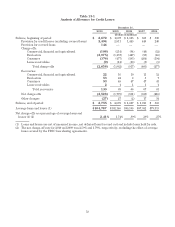

Substantially all of the loans acquired in the Colonial acquisition are covered by loss sharing agreements with

the FDIC, whereby the FDIC reimburses BB&T for the majority of the losses incurred. In addition, all of the

loans acquired were recorded at fair value as of the acquisition date without regard to the loss sharing

agreements. Loans were evaluated and assigned to loan pools based on common risk characteristics. The

determination of the fair value of the loans resulted in a significant write-down in the carrying amount of the

loans, which was assigned to an accretable or nonaccretable balance, with the accretable balance being recognized

as interest income over the remaining term of the loan. In accordance with the acquisition method of accounting,

there was no allowance brought forward on any of the acquired loans, as the credit losses evident in the loans

were included in the determination of the fair value of the loans at the acquisition date and are represented by the

nonaccretable balance. The majority of the nonaccretable balance is expected to be received from the FDIC in

connection with the loss sharing agreements and is recorded as a separate asset from the covered loans and

reflected on the Consolidated Balance Sheets. As a result, all of the loans acquired in the Colonial acquisition

were considered to be accruing loans as of the acquisition date. In accordance with regulatory reporting

standards, covered loans that are contractually past due will continue to be reported as past due and still accruing

based on the number of days past due.

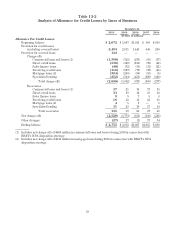

Given the significant amount of acquired loans that are past due but still accruing, BB&T believes the

inclusion of these loans in certain asset quality ratios including “Loans 30-89 days past due and still accruing as a

percentage of total loans and leases,” “Loans 90 days or more past due and still accruing as a percentage of total

loans and leases,” “Nonperforming loans and leases as a percentage of total loans and leases” and certain other

asset quality ratios that reflect nonperforming assets in the numerator or denominator (or both) results in

significant distortion to these ratios. In addition, because charge-offs related to the acquired loans are recorded

against the nonaccretable balance, the net charge-off ratio including the acquired loans is lower for portfolios that

have significant amounts of acquired loans. The inclusion of these loans in the asset quality ratios described above

could result in a lack of comparability across quarters or years, and could negatively impact comparability with

other portfolios that were not impacted by acquisition accounting. BB&T believes that the presentation of asset

quality measures excluding covered loans and related amounts from both the numerator and denominator

provides better perspective into underlying trends related to the quality of its loan portfolio. Accordingly, the

asset quality measures in Table 11 present asset quality information both on a consolidated basis as well as

excluding the covered assets and related amounts.

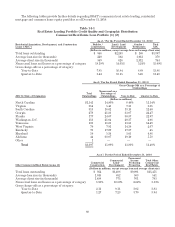

Consistent with BB&T’s belief that the presentation of certain asset quality measures excluding the impact

of covered loans is more meaningful, certain information reflected in Tables 12-1, 12-2, 14-1, 14-2 and 14-3 has

been adjusted to exclude the impact of covered loans and foreclosed property. These adjustments have been

identified and explained in the footnotes to each table.

53