BB&T 2010 Annual Report Download - page 50

Download and view the complete annual report

Please find page 50 of the 2010 BB&T annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

|

|

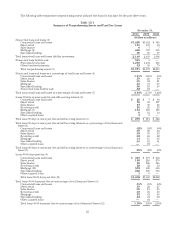

billion at December 31, 2010. This decline has been somewhat offset by increases in commercial and industrial

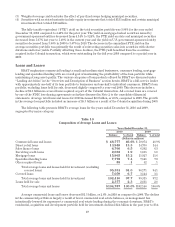

lending. Management has added a number of new producers in the corporate and middle-market banking area in

an effort to increase commercial and industrial lending to better diversify the loan portfolio and capitalize on the

strength of BB&T’s balance sheet during the economic downturn. During the fourth quarter of 2010, commercial

and industrial loans increased an annualized 6.9% compared to the third quarter of 2010.

Average direct retail loans declined 5.3% in 2010 due to continuing difficulties in the residential real estate

market, which decreased demand for home equity loan products. Average sales finance loans and average

revolving credit reflected growth rates of 5.9% and 9.5% during 2010, respectively. BB&T concentrates its efforts

on the highest quality borrowers in both of these product markets.

Average mortgage loans held for investment increased slightly compared to 2009. Management views

mortgage loans as an integral part of BB&T’s relationship-based credit culture. BB&T is a large originator of

residential mortgage loans, with 2010 originations of $24.9 billion. A majority of the mortgage loans originated

were sold in the secondary market during 2010. During the third quarter of 2010, management made the decision

to retain a portion of its 10 to 15 year fixed- and variable-rate production.

Average loans held by BB&T’s specialized lending subsidiaries increased $637 million, or 8.9%, compared to

2009. The growth in the specialized lending portfolio was primarily in nonprime automobile loans and small ticket

finance.

The average annualized FTE yield for 2010 for the total loan portfolio was 5.88% compared to 5.49% for the

prior year. The 39 basis point increase in the FTE yield on the loan portfolio was primarily due to the acquired

loans from the Colonial transaction, which have produced higher yields due to better than expected performance.

In the normal course of business, residential acquisition, development and construction, commercial

construction or commercial land/development loan agreements may include an interest reserve account at

inception. An interest reserve allows the borrower to add interest charges to the outstanding loan balance during

the construction period. Interest reserves provide an effective means to address the cash flow characteristics of a

real estate construction loan. Loan agreements containing an interest reserve generally require more equity to be

contributed by the borrower to the construction project at inception. Loans with interest reserves are subject to

substantially similar underwriting standards as loans without interest reserves.

Loans with interest reserves are closely monitored through physical inspections, reconciliation of draw

requests, review of rent rolls and operating statements and quarterly portfolio reviews performed by senior

management. When appropriate, extensions, renewals and restructurings of loans with interest reserves are

approved after giving consideration to the project’s status, the borrower’s financial condition, and the collateral

protection based on current market conditions. In connection with the extension, renewal or restructuring of a

loan with an interest reserve, additional interest reserves may be funded by the client, partially funded by the

client and BB&T, or fully provided by BB&T. Typically, interest reserves provided by BB&T are secured by

additional collateral and are limited to more conservative advance rates on the pledged collateral. These loans

must also be supported by an analysis of the client’s willingness and capacity to service the debt.

Interest that has been added to the balance of a loan through the use of an interest reserve is recognized as

income only if the collectability of the remaining contractual principal and interest payments is reasonably

assured. If a loan with interest reserves is in default and deemed uncollectible, interest is no longer funded

through the interest reserve. Interest previously recognized from interest reserves generally is not reversed

against current income when a construction loan with interest reserves is placed on nonaccrual status.

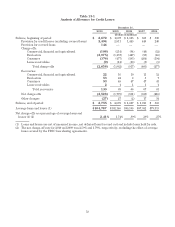

At December 31, 2010, approximately $1.2 billion of BB&T’s construction loan portfolio have active interest

reserves (i.e. current funding of interest charges through a reserve) compared to $2.4 billion at December 31,

2009. Interest income related to loans with active interest reserves was approximately $49 million and represents

less than 1% of total interest income for the year ended December 31, 2010.

50