BB&T 2010 Annual Report Download - page 118

Download and view the complete annual report

Please find page 118 of the 2010 BB&T annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

|

|

ŠWhether dividends have been reduced or eliminated, or scheduled interest payments on debt securities

have not been made; and

ŠAny other relevant available information.

For certain U.S. mortgage-backed securities (and in particular for non-agency Alt-A, Prime and other

mortgage-backed securities that have significant unrealized losses as a percentage of amortized cost), credit

impairment is assessed using a cash flow model that estimates the cash flows on the underlying mortgage pools,

using security-specific structure information. The model estimates cash flows from the underlying mortgage loan

pools and distributes those cash flows to the various tranches of securities, considering the transaction structure

and any subordination and credit enhancements that exist in each structure. The cash flow model projects the

remaining cash flows using a number of assumptions, including default rates, prepayment rates and recovery

rates (on foreclosed properties).

Management reviews the results of the cash flow model in conjunction with historical payment experience in

its estimation of possible future credit losses. If management does not expect to recover the entire amortized cost

basis of a mortgage-backed security, the Company records other-than-temporary impairment based on the

amount of expected credit losses in the mortgage-backed security. The remaining amount of unrealized loss is

recognized as a component of other comprehensive income.

Where a mortgage-backed security is not deemed to be credit impaired, management performs additional

analysis to assess whether it intends to sell and it is more likely than not that the Company will be required to sell

these debt securities before anticipated recovery of the amortized cost basis. In making this determination,

BB&T considers its expected liquidity and capital needs, including its asset/liability management needs,

forecasts, strategies and other relevant information.

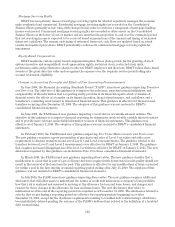

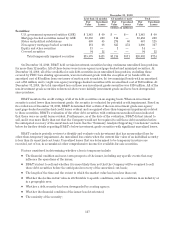

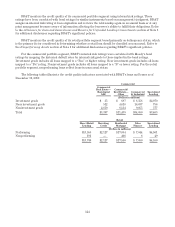

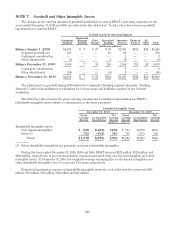

Summary Analysis Supporting Conclusions

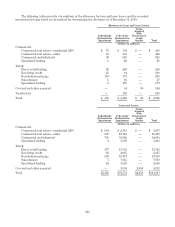

The following table presents a detailed analysis of non-investment grade securities with significant

unrealized losses that are not covered by a loss sharing arrangement. The expected underlying collateral losses

represent losses on the underlying mortgage pools supporting BB&T’s tranche. The benefits from subordination

represent the amount of the expected losses the subordinate security holders are obligated to absorb prior to

BB&T incurring a loss.

Non-investment grade securities with significant unrealized losses

December 31, 2010

(Dollars in millions)

Security Amortized

Cost Fair

Value Unrealized

Loss

Credit Rating Expected Underlying

Collateral Losses(1) Benefit of

Subordination(1)

Moody’s S&P Fitch

Securities with other-than-temporary impairment losses:

RMBS 1 $103 $ 72 $(31) Caa3 CC $16 $15

RMBS 2 47 33 (14) Ca C 7 3

RMBS 3 136 125 (11) Caa3 CC 20 4

RMBS 4 109 74 (35) CCC C 13 13

RMBS 5 52 42 (10) Caa3 CC C 6 3

(1) Estimated underlying collateral losses and benefit of subordination are prior to amounts recorded as other-

than-temporary impairment.

118