BB&T 2010 Annual Report Download - page 159

Download and view the complete annual report

Please find page 159 of the 2010 BB&T annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

149 -

150

150 -

151

151 -

152

152 -

153

153 -

154

154 -

155

155 -

156

156 -

157

157 -

158

158 -

159

159 -

160

160 -

161

161 -

162

162 -

163

163 -

164

164 -

165

165 -

166

166 -

167

167 -

168

168 -

169

169 -

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

|

|

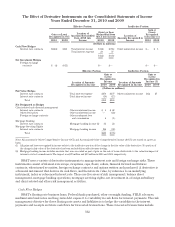

Loans receivable: The fair values for loans are estimated using discounted cash flow analyses, applying

interest rates currently being offered for loans with similar terms and credit quality. The interest rates being

offered by BB&T for new loans with similar terms and credit quality are reflective of credit risk and liquidity

spreads inherent in an orderly transaction in the current market. For commercial loans and leases, internal credit

risk models are used to adjust discount rates for risk migration and expected losses. For residential mortgage and

other consumer loans, internal prepayment risk models are used to adjust contractual cash flows. Loans are

aggregated into pools of similar terms and credit quality and discounted using a LIBOR based rate. The carrying

amounts of accrued interest approximate fair values.

Deposit liabilities: The fair values for demand deposits, interest-checking accounts, savings accounts and

certain money market accounts are, by definition, equal to the amount payable on demand at the reporting date.

Fair values for certificates of deposit are estimated using a discounted cash flow calculation that applies current

interest rates to aggregate expected maturities. In addition, nonfinancial instruments such as core deposit

intangibles are not recorded at fair value. BB&T has developed long-term relationships with its customers

through its deposit base and in the opinion of management, these items add significant value to BB&T.

Federal funds purchased, securities sold under repurchase agreements and short-term borrowed funds: The

carrying amounts of Federal funds purchased, borrowings under repurchase agreements and short-term

borrowed funds approximate their fair values.

Long-term debt: The fair values of long-term debt are estimated based on quoted market prices for the

instrument if available, or for similar instruments if not available, or by using discounted cash flow analyses,

based on BB&T’s current incremental borrowing rates for similar types of instruments.

Contractual commitments: The fair values of commitments are estimated using the fees charged to enter

into similar agreements, taking into account the remaining terms of the agreements and the present

creditworthiness of the counterparties. For fixed-rate loan commitments, fair values also consider the difference

between current levels of interest rates and the committed rates. The fair values of guarantees and letters of

credit are estimated based on the counterparties’ creditworthiness and average default rates for loan products

with similar risks. The fair values of commitments to fund affordable housing investments are estimated using

the net present value of future commitments.

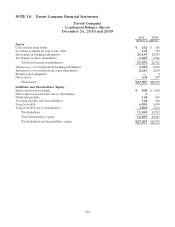

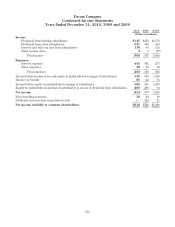

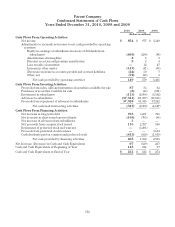

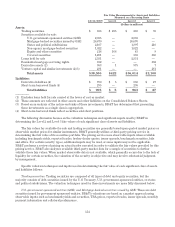

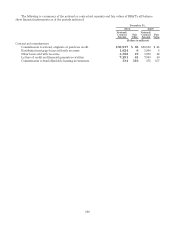

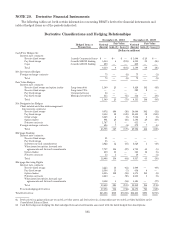

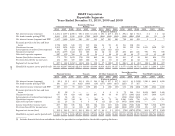

The following is a summary of the carrying amounts and fair values of those financial assets and liabilities

that BB&T has not recorded at fair value:

December 31,

2010 2009

Carrying

Amount Fair Value Carrying

Amount Fair

Value

(Dollars in millions)

Financial assets:

Loans and leases (1)(2) $101,380 $100,360 $101,056 $100,794

Financial liabilities:

Deposits 107,213 104,091 114,965 112,917

Long-term debt 21,730 22,733 21,376 21,018

(1) Includes loans held for sale carried at the lower of cost or market.

(2) The carrying value is net of the allowance for loan and lease losses.

159