BB&T 2010 Annual Report Download - page 37

Download and view the complete annual report

Please find page 37 of the 2010 BB&T annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

|

|

that banking organizations that meet certain criteria, including excellent asset quality, high liquidity, low interest

rate exposure and good earnings, and that have received the highest regulatory rating must maintain a ratio of

Tier 1 capital to total adjusted average assets of at least 3%. Institutions not meeting these criteria, as well as

institutions with supervisory, financial or operational weaknesses, are expected to maintain a minimum Tier 1

capital to total adjusted average assets ratio at least 100 basis points above that stated minimum. Holding

companies experiencing internal growth or making acquisitions are expected to maintain strong capital positions

substantially above the minimum supervisory levels without significant reliance on intangible assets. The Federal

Reserve also continues to consider a “tangible Tier 1 capital leverage ratio” (deducting all intangibles) and other

indicators of capital strength in evaluating proposals for expansion or new activity.

In addition, the Federal Reserve, the FDIC and the OTS all have adopted risk-based capital standards that

explicitly identify concentrations of credit risk and the risk arising from non-traditional activities, as well as an

institution’s ability to manage these risks, as important factors to be taken into account by each agency in

assessing an institution’s overall capital adequacy. The capital guidelines also provide that an institution’s

exposure to a decline in the economic value of its capital due to changes in interest rates be considered by the

agency as a factor in evaluating a banking organization’s capital adequacy. The agencies also require banks and

bank holding companies to adjust their regulatory capital to take into consideration the risk associated with

certain recourse obligations, direct credit subsidies, residual interest and other positions in securitized

transactions that expose banking organizations to credit risk.

As part of the Dodd-Frank Act, provisions were added that require federal banking agencies to develop

capital requirements that address systemically risky activities. The effect of these capital rules will disallow trust

preferred securities from counting as Tier 1 capital at the holding company level for entities with greater than

$15 billion in assets with a three-year phase-in period beginning on January 1, 2013.

In addition, in 2010, the Group of Governors and Heads of Supervisors of the Basel Committee on Banking

Supervision, the oversight body of the Basel Committee, published its “calibrated” capital standards for major

banking institutions (“Basel III”). Under these standards, when fully phased in on January 1, 2019, banking

institutions will be required to maintain heightened Tier 1 common equity, Tier 1 capital and total capital ratios,

as well as maintaining a “capital conservation buffer.” The Tier 1 common equity and Tier 1 capital ratio

requirements will be phased in incrementally between January 1, 2013 and January 1, 2015; the deductions from

common equity made in calculating Tier 1 common equity (for example, for mortgage servicing assets, deferred

tax assets and investments in unconsolidated financial institutions) will be phased in incrementally over a four-

year period commencing on January 1, 2014; and the capital conservation buffer will be phased in incrementally

between January 1, 2016 and January 1, 2019. The Basel Committee also announced that a “countercyclical

buffer” of 0% to 2.5% of common equity or other fully loss-absorbing capital “will be implemented according to

national circumstances” as an “extension” of the conservation buffer. The final package of Basel III reforms were

approved by the G20 leaders in November 2010 and are subject to individual adoption by member nations,

including the United States. If the foregoing revised capital standards are adopted in their current form, BB&T

estimates these standards would have a negligible impact on BB&T’s ability to comply with the revised

regulatory capital ratios based on BB&T’s current understanding of the revisions to capital qualification.

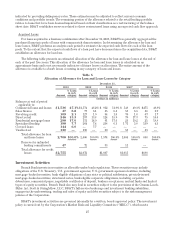

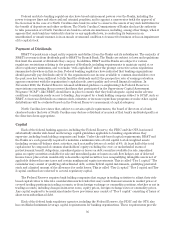

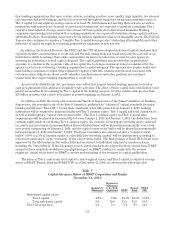

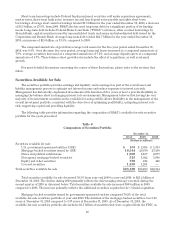

The ratios of Tier 1 capital and total capital to risk-weighted assets, and Tier 1 capital to adjusted average

assets of BB&T, Branch Bank and BB&T FSB as of December 31, 2010, are shown in the following table.

Table 7

Capital Adequacy Ratios of BB&T Corporation and Banks

December 31, 2010

Regulatory

Minimums

Regulatory

Minimums

to be Well-

Capitalized BB&T Branch

Bank BB&T

FSB

Risk-based capital ratios:

Tier 1 capital 4.0% 6.0% 11.8% 13.0% 15.0%

Total risk-based capital 8.0 10.0 15.5 15.5 16.3

Tier 1 leverage ratio 3.0 5.0 9.1 9.9 14.3

37