BB&T 2010 Annual Report Download - page 124

Download and view the complete annual report

Please find page 124 of the 2010 BB&T annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

|

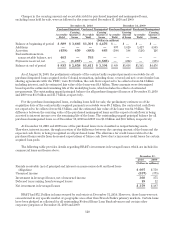

|

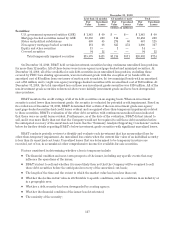

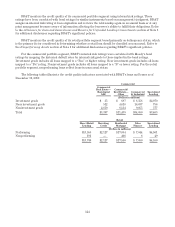

BB&T monitors the credit quality of its commercial portfolio segment using internal risk ratings. These

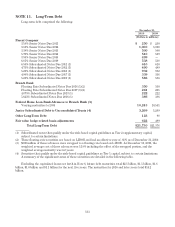

ratings have been correlated with bond ratings for similar instruments based on management’s judgment. BB&T

assigns an internal risk rating at loan origination and reviews the relationship again on an annual basis or at any

point management becomes aware of information affecting the borrower’s ability to fulfill their obligations. Refer

to the Allowance for Loan and Lease Losses and Reserve for Unfunded Lending Commitments section of Note 1

for additional disclosures regarding BB&T’s significant policies.

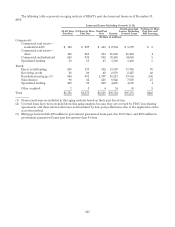

BB&T monitors the credit quality of its retail portfolio segment based primarily on delinquency status, which

is the primary factor considered in determining whether a retail loan should be classified as nonaccrual. Refer to

the Nonperforming Assets section of Note 1 for additional disclosures regarding BB&T’s significant policies.

For the commercial portfolio segment, BB&T’s internal risk ratings were correlated with Moody’s bond

ratings by mapping the historical default rates by internal risk grade to those implied in the bond ratings.

Investment grade includes all loans mapped to a “Baa” or higher rating. Near investment grade includes all loans

mapped to a “Ba” rating. Noninvestment grade includes all loans mapped to a “B” or lower rating. For the retail

portfolio segment, nonperforming loans reflect loans in nonaccrual status.

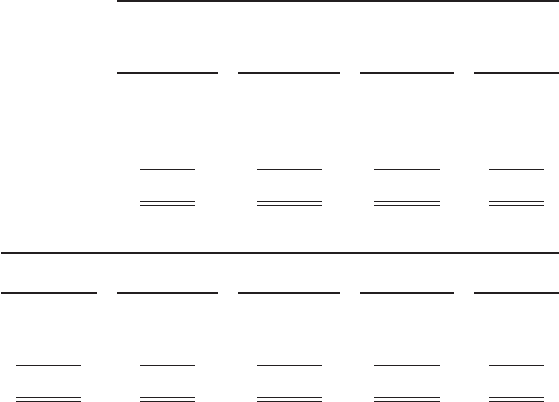

The following tables illustrate the credit quality indicators associated with BB&T’s loans and leases as of

December 31, 2010:

Commercial

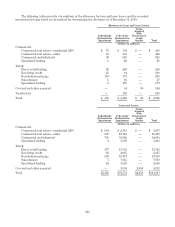

Commercial

Real Estate—

Residential

ADC

Commercial

Real Estate—

Other Commercial

& Industrial Specialized

Lending

(Dollars in millions)

Investment grade $ 35 $ 687 $ 8,358 $2,070

Near investment grade 512 4,618 16,637 756

Noninvestment grade 2,850 6,134 9,055 577

Total $3,397 $11,439 $34,050 $3,403

Retail

Direct Retail

Lending Revolving

Credit Residential

Mortgage Sales

Finance Specialized

Lending

(Dollars in millions)

Performing $13,558 $2,127 $17,084 $ 7,044 $4,501

Nonperforming 191 — 466 6 49

$13,749 $2,127 $17,550 $ 7,050 $4,550

124