BB&T 2010 Annual Report Download - page 163

Download and view the complete annual report

Please find page 163 of the 2010 BB&T annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

153 -

154

154 -

155

155 -

156

156 -

157

157 -

158

158 -

159

159 -

160

160 -

161

161 -

162

162 -

163

163 -

164

164 -

165

165 -

166

166 -

167

167 -

168

168 -

169

169 -

170

170 -

171

171 -

172

172 -

173

173 -

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

|

|

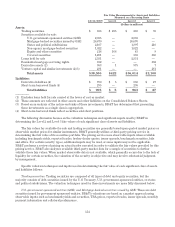

interest receipts on commercial loans and interest payments on 3 month LIBOR funding. All of BB&T’s current

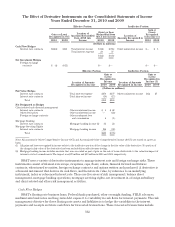

cash flow hedges are hedging exposure to variability in future cash flows for forecasted transactions related to

the payment of variable interest on then existing financial instruments. At December 31, 2010 and 2009, the

maximum length of time over which BB&T is hedging its exposure on such transactions is 6.6 years.

For a qualifying cash flow hedge, the portion of changes in the fair value of the derivatives that has been

highly effective is recognized in other comprehensive income (loss) until the related cash flows from the hedged

item are recognized in earnings. If a derivative designated as a cash flow hedge is terminated or ceases to be

highly effective, the gain or loss in other comprehensive income (loss) is amortized to earnings over the period the

forecasted hedged transactions impact earnings. If a hedged forecasted transaction is no longer probable of

occurring during the forecast period or within a short period thereafter, hedge accounting is ceased and any gain

or loss included in other comprehensive income (loss) is reported in earnings immediately. During the year ended

December 31, 2010 and 2009, BB&T amortized approximately $24 million and $49 million of unrecognized pre-tax

gains from accumulated other comprehensive income (loss) into net interest income.

At December 31, 2010, BB&T had $47 million of unrecognized losses on derivatives classified as cash flow

hedges recorded in other comprehensive income (loss), compared to $107 million of unrecognized gains at

December 31, 2009. The estimated amount to be reclassified from other comprehensive income (loss) into

earnings during the next 12 months is a loss totaling approximately $30 million. This includes gains and losses

related to hedges that were terminated early for which the forecasted transactions are still probable. The

proceeds from these terminations were included in cash flows from financing activities.

All cash flow hedges were highly effective for the year ended December 31, 2010, and the change in fair value

attributed to hedge ineffectiveness was not material.

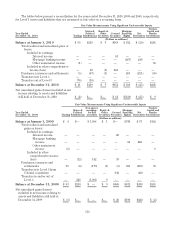

Fair Value Hedges

BB&T’s fixed rate long term debt, certificates of deposit, FHLB advances, loan and municipal security assets

result in exposure to losses in value as interest rates change. The risk management objective for hedging fixed

rate assets and liabilities is to convert the fixed rate paid or received to a floating rate. BB&T accomplishes its

risk management objective by hedging exposure to changes in fair value of fixed rate financial instruments

primarily through the use of swaps. For a qualifying fair value hedge, changes in the value of the derivatives that

have been highly effective as hedges are recognized in current period earnings along with the corresponding

changes in the fair value of the designated hedged item attributable to the risk being hedged.

During the years ended December 31, 2010 and 2009, BB&T terminated certain fair value hedges primarily

related to its long-term debt and received proceeds of $314 million and $131 million, respectively. When hedged

debt/other financial instruments are retired or redeemed, the amounts associated with the hedge are included as

a component of the gain or loss on termination. When a hedge is terminated but the hedged item remains

outstanding, the proceeds from the termination of these hedges have been reflected as part of the carrying value

of the underlying debt/other financial instrument and are being amortized to earnings over its remaining life. The

proceeds from these terminations were included in cash flows from financing activities. During 2009, BB&T

recognized $24 million in gains on debt retirement associated with previous hedges. There were no hedge

unwinds associated with debt retirement during 2010. During the years ended December 31, 2010 and 2009,

BB&T recognized pre-tax benefits of $64 million and $21 million respectively through reductions of interest

expense from previous hedge unwinds.

Derivatives Not Designated As Hedges

Derivatives not designated as a hedge include those that are entered into as either balance sheet risk

management instruments or to facilitate client needs. Balance sheet risk management hedges are those hedges

that do not qualify to be treated as either a cash flow hedge, a fair value hedge or a foreign currency hedge for

accounting purposes, but are necessary to economically manage the risk associated with an asset or liability.

This category of hedges includes derivatives that hedge mortgage banking operations and mortgage

servicing rights (“MSRs”). For mortgage loans originated for sale, BB&T is exposed to changes in market rates

163