BB&T 2010 Annual Report Download - page 78

Download and view the complete annual report

Please find page 78 of the 2010 BB&T annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

|

|

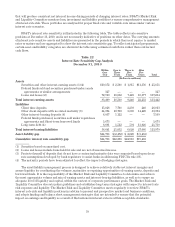

that will produce consistent net interest income during periods of changing interest rates. BB&T’s Market Risk

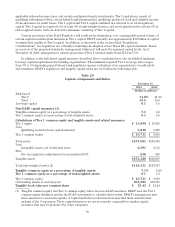

and Liquidity Committee monitors loan, investment and liability portfolios to ensure comprehensive management

of interest rate risk. These portfolios are analyzed for proper fixed-rate and variable-rate mixes under various

interest rate scenarios.

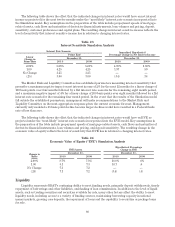

BB&T’s interest rate sensitivity is illustrated in the following table. The table reflects rate-sensitive

positions at December 31, 2010, and is not necessarily indicative of positions on other dates. The carrying amounts

of interest rate sensitive assets and liabilities are presented in the periods in which they next reprice to market

rates or mature and are aggregated to show the interest rate sensitivity gap. To reflect anticipated prepayments,

certain asset and liability categories are shown in the table using estimated cash flows rather than contractual

cash flows.

Table 22

Interest Rate Sensitivity Gap Analysis

December 31, 2010

Within

One

Year

One to

Three

Years

Three to

Five

Years

After

Five

Years Total

(Dollars in millions)

Assets

Securities and other interest-earning assets (1)(4) $10,172 $ 2,508 $ 1,815 $11,356 $ 25,851

Federal funds sold and securities purchased under resale

agreements or similar arrangements 327 — — — 327

Loans and leases (2) 72,910 16,052 7,425 10,877 107,264

Total interest-earning assets 83,409 18,560 9,240 22,233 133,442

Liabilities

Client time deposits 15,826 7,708 2,239 240 26,013

Other client deposits with no stated maturity (3) 24,394 10,700 3,880 14,420 53,394

Other interest-bearing deposits (4) 6,057 1,112 — — 7,169

Federal funds purchased, securities sold under repurchase

agreements and Short-term borrowed funds 5,673 — — — 5,673

Long-term debt (4) 6,691 1,512 501 13,026 21,730

Total interest-bearing liabilities 58,641 21,032 6,620 27,686 113,979

Asset-liability gap $24,768 $ (2,472) $ 2,620 $ (5,453)

Cumulative interest rate sensitivity gap $24,768 $22,296 $24,916 $19,463

(1) Securities based on amortized cost.

(2) Loans and leases include loans held for sale and are net of unearned income.

(3) Projected runoff of deposits that do not have a contractual maturity date was computed based upon decay

rate assumptions developed by bank regulators to assist banks in addressing FDICIA rule 305.

(4) The maturity periods have been adjusted to reflect the impact of hedging strategies.

The asset/liability management process is designed to achieve relatively stable net interest margins and

assure liquidity by coordinating the volumes, maturities or repricing opportunities of earning assets, deposits and

borrowed funds. It is the responsibility of the Market Risk and Liquidity Committee to determine and achieve

the most appropriate volume and mix of earning assets and interest-bearing liabilities, as well as to ensure an

adequate level of liquidity and capital, within the context of corporate performance goals. The Market Risk and

Liquidity Committee also sets policy guidelines and establishes long-term strategies with respect to interest rate

risk exposure and liquidity. The Market Risk and Liquidity Committee meets regularly to review BB&T’s

interest rate risk and liquidity positions in relation to present and prospective market and business conditions,

and adopts funding and balance sheet management strategies that are intended to ensure that the potential

impact on earnings and liquidity as a result of fluctuations in interest rates is within acceptable standards.

78