BB&T 2010 Annual Report Download - page 155

Download and view the complete annual report

Please find page 155 of the 2010 BB&T annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

145 -

146

146 -

147

147 -

148

148 -

149

149 -

150

150 -

151

151 -

152

152 -

153

153 -

154

154 -

155

155 -

156

156 -

157

157 -

158

158 -

159

159 -

160

160 -

161

161 -

162

162 -

163

163 -

164

164 -

165

165 -

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

|

|

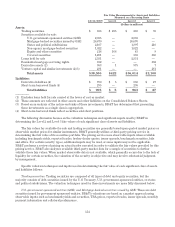

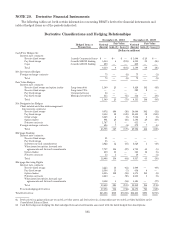

States and political subdivisions: These are debt securities issued by states and political subdivisions.

BB&T’s valuations are primarily based on a market approach using observable inputs such as benchmark yields,

MSRB reported trades, material event notices and new issue data.

Non-agency mortgage-backed securities: BB&T’s valuation for these debt securities is based on a market

approach using observable inputs such as benchmark yields and securities, TBA prices, reported trades, monthly

payment information and collateral performance.

Equity and other securities: These securities consist primarily of equities, mutual funds and corporate bonds.

These securities are valued based on a review of quoted market prices for identical and similar assets as well as

through the various other inputs discussed previously.

Covered securities: Covered securities are covered by FDIC loss sharing agreements and consist of re-remic

non-agency mortgage-backed securities and municipal securities. The covered state and political subdivision

securities and certain non-agency mortgage-backed securities are valued in a manner similar to the approach

described above for these asset classes. The re-remic non-agency mortgage-backed securities, which are

categorized as Level 3, were valued based on broker dealer quotes that reflected certain unobservable market

inputs.

Loans held for sale: BB&T originates certain mortgage loans to be sold to investors. These loans are carried

at fair value based on BB&T’s election of the Fair Value Option. The fair value is primarily based on quoted

market prices for securities backed by similar types of loans. The changes in fair value of these assets are largely

driven by changes in interest rates subsequent to loan funding and changes in the fair value of servicing

associated with the mortgage loan held for sale.

Residential mortgage servicing rights: BB&T estimates the fair value of residential mortgage servicing

rights (“MSRs”) using an option adjusted spread (“OAS”) valuation model to project MSR cash flows over

multiple interest rate scenarios, which are then discounted at risk-adjusted rates. The OAS model considers

portfolio characteristics, contractually specified servicing fees, prepayment assumptions, delinquency rates, late

charges, other ancillary revenue, costs to service and other economic factors. When available, fair value estimates

and assumptions are compared to observable market data and to recent market activity and actual portfolio

experience.

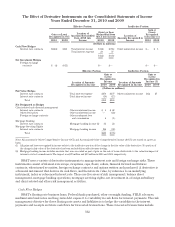

Derivative assets and liabilities: BB&T uses derivatives to manage various financial risks. The fair values of

derivative financial instruments are determined based on quoted market prices, dealer quotes and internal

pricing models that are primarily sensitive to market observable data. The fair value of interest rate lock

commitments, which are related to mortgage loan commitments, is based on quoted market prices adjusted for

commitments that BB&T does not expect to fund and includes the value attributable to the net servicing fee.

Venture capital and similar investments: BB&T has venture capital and similar investments that are carried

at fair value. In many cases there are no observable market values for these investments and therefore

management must estimate the fair value based on a comparison of the operating performance of the company to

multiples in the marketplace for similar entities. This analysis requires significant judgment and actual values in

a sale could differ materially from those estimated.

Short-term borrowed funds: Short-term borrowed funds represent debt securities sold short. These are

entered into through BB&T’s brokerage subsidiary Scott & Stringfellow, LLC. These trades are executed as a

hedging strategy for the purposes of supporting institutional and retail client trading activities.

155