BB&T 2010 Annual Report Download - page 21

Download and view the complete annual report

Please find page 21 of the 2010 BB&T annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

|

|

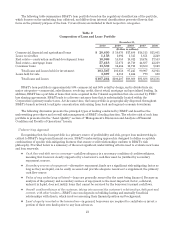

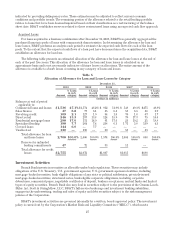

The following table summarizes BB&T’s loan portfolio based on the regulatory classification of the portfolio,

which focuses on the underlying loan collateral, and differs from internal classifications presented herein that

focus on the primary purpose of the loan. Covered loans are included in their respective categories.

Table 2

Composition of Loan and Lease Portfolio

December 31,

2010 2009 2008 2007 2006

(Dollars in millions)

Commercial, financial and agricultural loans $ 20,490 $ 19,076 $17,489 $14,515 $11,061

Lease receivables 1,158 1,092 1,315 1,651 2,249

Real estate—construction and land development loans 10,969 15,353 18,012 19,474 17,553

Real estate—mortgage loans 57,418 55,671 48,719 44,687 42,219

Consumer loans 13,532 12,464 11,710 10,580 9,829

Total loans and leases held for investment 103,567 103,656 97,245 90,907 82,911

Loans held for sale 3,697 2,551 1,424 779 680

Total loans and leases $107,264 $106,207 $98,669 $91,686 $83,591

BB&T’s loan portfolio is approximately 50% commercial and 50% retail by design, and is divided into six

major categories—commercial, sales finance, revolving credit, direct retail, mortgage and specialized lending. In

addition, BB&T has a portfolio of loans that were acquired in the Colonial acquisition that are covered by FDIC

loss sharing agreements. BB&T lends to a diverse customer base that is substantially located within the

Corporation’s primary market area. At the same time, the loan portfolio is geographically dispersed throughout

BB&T’s branch network to mitigate concentration risk arising from local and regional economic downturns.

The following discussion presents the principal types of lending conducted by BB&T and describes the

underwriting procedures and overall risk management of BB&T’s lending function. The relative risk of each loan

portfolio is presented in the “Asset Quality” section of “Management’s Discussion and Analysis of Financial

Condition and Results of Operations” herein.

Underwriting Approach

Recognizing that the loan portfolio is a primary source of profitability and risk, proper loan underwriting is

critical to BB&T’s long-term financial success. BB&T’s underwriting approach is designed to define acceptable

combinations of specific risk-mitigating features that ensure credit relationships conform to BB&T’s risk

philosophy. Provided below is a summary of the most significant underwriting criteria used to evaluate new loans

and loan renewals:

ŠCash flow and debt service coverage—cash flow adequacy is a necessary condition of creditworthiness,

meaning that loans not clearly supported by a borrower’s cash flow must be justified by secondary

repayment sources.

ŠSecondary sources of repayment—alternative repayment funds are a significant risk-mitigating factor as

long as they are liquid, can be easily accessed and provide adequate resources to supplement the primary

cash flow source.

ŠValue of any underlying collateral—loans are generally secured by the asset being financed. Because an

analysis of the primary and secondary sources of repayment is the most important factor, collateral,

unless it is liquid, does not justify loans that cannot be serviced by the borrower’s normal cash flows.

ŠOverall creditworthiness of the customer, taking into account the customer’s relationships, both past and

current, with other lenders—BB&T’s success depends on building lasting and mutually beneficial

relationships with clients, which involves assessing their financial position and background.

ŠLevel of equity invested in the transaction—in general, borrowers are required to contribute or invest a

portion of their own funds prior to any loan advances.

21