BB&T 2010 Annual Report Download - page 27

Download and view the complete annual report

Please find page 27 of the 2010 BB&T annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

|

|

indicated by prevailing delinquency rates. These estimates may be adjusted to reflect current economic

conditions and portfolio trends. The remaining portion of the allowance related to the retail lending portfolio

relates to loans that have been deemed impaired based on their classification as a restructuring at the balance

sheet date. BB&T establishes reserves related to these restructured loans using an expected cash flow approach.

Acquired Loans

For loans acquired in a business combination after December 31, 2008, BB&T has generally aggregated the

purchased loans into pools of loans with common risk characteristics. In determining the allowance for loan and

lease losses, BB&T performs an analysis each period to estimate the expected cash flows for each of the loan

pools. To the extent that the expected cash flows of a loan pool have decreased since the acquisition date, BB&T

establishes an allowance for loan loss.

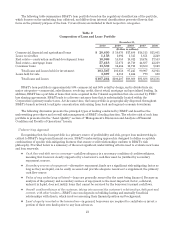

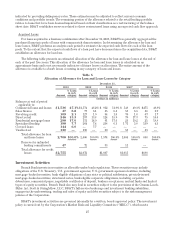

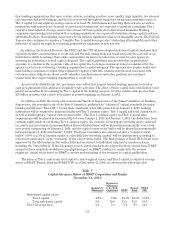

The following table presents an estimated allocation of the allowance for loan and lease losses at the end of

each of the past five years. This allocation of the allowance for loan and lease losses is calculated on an

approximate basis and is not necessarily indicative of future losses or allocations. The entire amount of the

allowance is available to absorb losses occurring in any category of loans and leases.

Table 5

Allocation of Allowance for Loan and Lease Losses by Category

December 31,

2010 2009 2008 2007 2006

Amount

% Loans

in each

category Amount

% Loans

in each

category Amount

% Loans

in each

category Amount

% Loans

in each

category Amount

% Loans

in each

category

(Dollars in millions)

Balances at end of period

applicable to:

Commercial loans and leases $1,536 47.1% $1,574 48.2% $ 912 51.9% $ 548 49.3% $475 49.8%

Sales finance 47 6.8 77 6.1 55 6.5 58 6.6 58 6.9

Revolving credit 109 2.1 127 1.9 94 1.8 70 1.8 67 1.7

Direct retail 246 13.3 297 13.8 124 15.9 79 17.3 75 18.5

Residential mortgage loans 298 17.0 131 14.9 91 17.6 25 19.2 21 18.8

Specialized lending 198 7.7 264 7.4 238 6.3 1 71 5.8 139 4.3

Covered loans 144 6.0 — 7.7—— —— — —

Unallocated 130 — 130 — 60 — 53 — 53 —

Total allowance for loan

and lease losses 2,708 100.0% 2,600 100.0% 1,574 100.0% 1,004 100.0% 888 100.0%

Reserve for unfunded

lending commitments 47 72 33 11 —

Total allowance for credit

losses $2,755 $2,672 $1,607 $1,015 $888

Investment Activities

Branch Bank invests in securities as allowable under bank regulations. These securities may include

obligations of the U.S. Treasury, U.S. government agencies, U.S. government-sponsored entities, including

mortgage-backed securities, bank eligible obligations of any state or political subdivision, privately-issued

mortgage-backed securities, structured notes, bank eligible corporate obligations, including corporate

debentures, commercial paper, negotiable certificates of deposit, bankers acceptances, mutual funds and limited

types of equity securities. Branch Bank also may deal in securities subject to the provisions of the Gramm-Leach-

Bliley Act. Scott & Stringfellow, LLC, BB&T’s full-service brokerage and investment banking subsidiary,

engages in the underwriting, trading and sales of equity and debt securities subject to the risk management

policies of the Corporation.

BB&T’s investment activities are governed internally by a written, board-approved policy. The investment

policy is carried out by the Corporation’s Market Risk and Liquidity Committee (“MRLC”), which meets

27