BB&T 2010 Annual Report Download - page 56

Download and view the complete annual report

Please find page 56 of the 2010 BB&T annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

|

|

(1) Covered and other acquired loans are considered to be performing due to the application of the accretion method. Covered

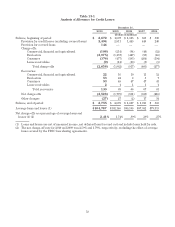

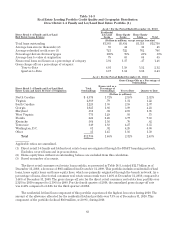

loans that are contractually past due are noted in the footnotes below.

(2) Excludes nonaccrual mortgage loans that are government guaranteed totaling $55 million and $17 million as of December 31,

2009 and December 31, 2008, respectively. BB&T revised its nonaccrual policy related to FHA/VA guaranteed loans during

2010. The change in policy resulted in a decrease in nonaccrual mortgage loans and an increase in mortgage loans 90 days

past due and still accruing of approximately $79 million.

(3) Excludes foreclosed real estate totaling $313 million and $160 million as of December 31, 2010 and December 31, 2009,

respectively, that are covered by FDIC loss sharing agreements.

(4) These asset quality ratios have been adjusted to remove the impact of covered loans and covered foreclosed property.

Appropriate adjustments to the numerator and denominator have been reflected in the calculation of these ratios.

Management believes the inclusion of acquired loans in certain asset quality ratios that include nonperforming assets, past

due loans or net charge-offs in the numerator or denominator results in distortion of these ratios and they may not be

comparable to other periods presented or to other portfolios that were not impacted by purchase accounting.

(5) Including loans covered by FDIC loss sharing agreements, nonaccrual loans and leases as a percentage of total loans and

leases were 2.49% and 2.51%, as of December 31, 2010 and December 31, 2009, respectively.

(6) Excludes mortgage loans guaranteed by GNMA that BB&T does not have the obligation to repurchase.

(7) Excludes mortgage loans past due 90 days or more that are government guaranteed totaling $153 million, $8 million and $7

million at December 31, 2010, December 31, 2009 and December 31, 2008, respectively.

(8) Excludes loans past due 90 days or more that are covered by FDIC loss sharing agreements totaling $1.1 billion and $1.4

billion at December 31, 2010 and December 31, 2009, respectively.

(9) Including loans covered by FDIC loss sharing agreements, loans past due 90 days or more and still accruing as a percentage

of total loans and leases were 1.34% and 1.60% as of December 31, 2010 and December 31, 2009, respectively.

(10) Excludes mortgage loans past due 30-89 days that are government guaranteed totaling $83 million, $23 million and $25

million at December 31, 2010, December 31, 2009 and December 31, 2008, respectively.

(11) Excludes loans totaling $363 million and $391 million past due 30-89 days at December 31, 2010 and December 31, 2009,

respectively, that are covered by FDIC loss sharing agreements.

(12) Including loans covered by FDIC loss sharing agreements, loans past due 30-89 days as a percentage of total loans and leases

were 1.65% and 1.93% as of December 31, 2010 and December 31, 2009, respectively.

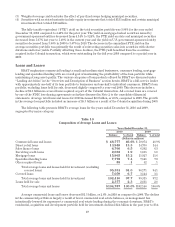

Table 12-2

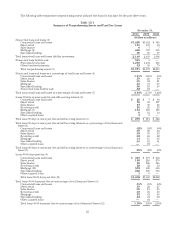

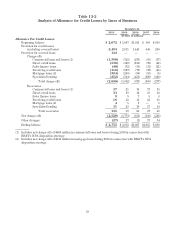

Troubled Debt Restructurings

December 31, 2010

Current Status Past Due 30-89 Days Past Due 90+ Days Total

(Dollars in millions)

Performing restructurings: (1) (2) (3)

Commercial loans $ 637 97.0 % $ 20 3.0 % $— — % $ 657

Direct retail loans 129 91.5 10 7.1 2 1.4 141

Sales finance loans — — 1 20.0 4 80.0 5

Revolving credit loans 48 77.4 8 12.9 6 9.7 62

Residential mortgage loans (4) 454 77.6 108 18.5 23 3.9 585

Specialized lending loans 23 88.5 3 11.5 — — 26

Total performing restructurings 1,291 87.5 150 10.2 35 2.4 1,476

Nonperforming restructurings (5) 132 27.6 60 12.5 287 59.9 479

Total restructurings $1,423 72.8 $210 10.6 $322 16.5 $1,955

(1) Excludes restructured covered and other acquired loans accounted for under the accretion method.

(2) Past due performing restructurings are included in past due disclosures.

(3) Excludes restructured mortgage loans that are government guaranteed totaling $14 million included in loans

held for sale.

(4) Excludes restructured mortgage loans that are government guaranteed totaling $115 million.

(5) Nonperforming restructurings are included in nonaccrual loan disclosures.

Troubled debt restructurings (“restructurings”) generally occur when a borrower is experiencing, or is

expected to experience, financial difficulties in the near-term. As a result, BB&T will work with the borrower to

prevent further difficulties, and ultimately to improve the likelihood of recovery on the loan. To facilitate this

process, a concessionary modification that would not otherwise be considered may be granted resulting in

classification of the loan as a restructuring. Restructurings can involve loans remaining on nonaccrual, moving to

nonaccrual, or continuing on accruing status, depending on the individual facts and circumstances of the

borrower. In circumstances where the restructuring involves charging off a portion of the loan balance, BB&T

typically classifies these restructurings as nonaccrual. With respect to commercial restructurings, an analysis of

the credit evaluation, in conjunction with an evaluation of the borrower’s performance prior to the restructuring,

are considered when evaluating the borrower’s ability to meet the restructured terms of the loan agreement.

Restructured nonaccrual loans may be returned to accrual status based on a current, well-documented credit

evaluation of the borrower’s financial condition and prospects for repayment under the modified terms. This

56