BB&T 2010 Annual Report Download - page 51

Download and view the complete annual report

Please find page 51 of the 2010 BB&T annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

|

|

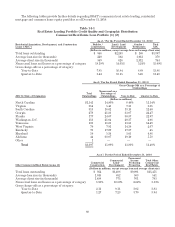

Asset Quality and Credit Risk Management

BB&T has established the following general practices to manage credit risk:

Šlimiting the amount of credit that individual lenders may extend to a borrower;

Šestablishing a process for credit approval accountability;

Šcareful initial underwriting and analysis of borrower, transaction, market and collateral risks;

Šongoing servicing of individual loans and lending relationships;

Šcontinuous monitoring of the portfolio, market dynamics and the economy; and

Šperiodically reevaluating the bank’s strategy and overall exposure as economic, market and other

relevant conditions change.

BB&T’s lending strategy focuses on relationship based lending within its markets. BB&T has continued to

work with its clients that have experienced financial difficulties throughout the economic recession. During the

second quarter of 2010, management implemented a comprehensive nonperforming asset disposition strategy

with a goal of more aggressively reducing BB&T’s exposure to nonperforming loans and foreclosed properties

and to reduce or eliminate any delay in exiting the credit cycle. The strategy was implemented during the second

quarter of 2010 as management believed that pricing for distressed assets had improved. This strategy continued

throughout the third and fourth quarters and into 2011.

The implementation of the nonperforming asset disposition strategy included the identification of problem

assets that were transferred from loans held for investment to loans held for sale. In connection with the

strategy, management transferred loans with a book value of approximately $1.9 billion to loans held for sale

during 2010. This included $1.5 billion of commercial loans, which were primarily in the residential, acquisition

and development and other commercial real estate portfolios, and $388 million of residential mortgage loans. Net

charge-offs of $605 million were recorded upon transfer to loans held for sale. This included $141 million related to

residential mortgage loans and $464 million for commercial loans. BB&T also recognized $90 million of losses and

additional writedowns related to commercial loans held for sale during 2010. As of December 31, 2010, there

remained $521 million of nonaccrual commercial loans held for sale. These loans were carried at average prices

that are consistent with actual sales results. Management expects that these loans will be disposed of in the first

half of 2011.

51