BB&T 2010 Annual Report Download - page 69

Download and view the complete annual report

Please find page 69 of the 2010 BB&T annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

|

|

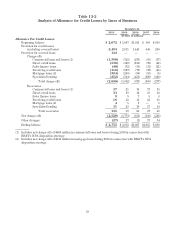

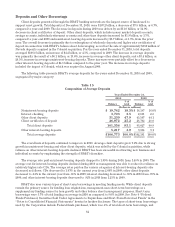

Provision for Credit Losses

A provision for credit losses is charged against earnings in order to maintain an allowance for loan and lease

losses and a reserve for unfunded lending commitments that reflects management’s best estimate of probable

losses inherent in the credit portfolios at the balance sheet date. The amount of the provision is based on

continuing assessments of nonperforming and “watch list” loans and associated unfunded credit commitments,

analytical reviews of loss experience in relation to outstanding loans and funded credit commitments, loan charge-

offs, nonperforming asset trends and management’s judgment with respect to current and expected economic

conditions and their impact on the loan portfolio and outstanding unfunded credit commitments. The methodology

used is described in the “Overview and Description of Business” section under the heading “Allowance for Loan

and Lease Losses and Reserve for Unfunded Credit Commitments.” The provision for credit losses recorded by

BB&T in 2010 was $2.6 billion, compared with $2.8 billion in 2009 and $1.4 billion in 2008.

The provision for credit losses decreased 6.2% during 2010 while total loans and leases held for investment

was relatively flat compared to the balance outstanding at the end of 2009. Included in the provision for credit

losses during 2010 was $144 million related to covered loans. The provision for credit losses recorded for covered

loans reflects lower expected cash flows on certain loan pools compared to the original estimates. Approximately

80% of this provision for credit losses is offset through a credit to noninterest income based on the provisions of

the FDIC loss sharing agreements. Net charge-offs were 2.41% of average loans and leases (or 2.59% excluding

covered loans) for 2010 compared to 1.74% of average loans and leases (or 1.79% excluding covered loans) during

2009. The allowance for loan and lease losses was 2.62% of loans and leases held for investment (or 2.63%

excluding covered loans) and was 1.26x total nonaccrual loans and leases held for investment (or 1.19x excluding

covered loans) at year-end 2010, compared to 2.51% (or 2.72% excluding covered loans) and .98x, respectively, at

December 31, 2009. The decrease in the provision for credit losses during 2010 compared to 2009 was primarily

due to the improving economic outlook that began to materialize in the latter part of 2010. The 94.5% increase in

the provision for credit losses during 2009 compared to 2008 was primarily driven by ongoing challenges in

residential real estate markets and the overall economy with the largest concentration of credit issues occurring

in Georgia, Florida, and metro Washington D.C., with some deterioration in the coastal areas of the Carolinas.

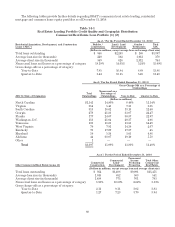

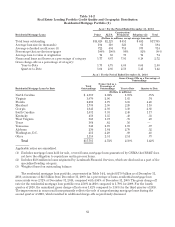

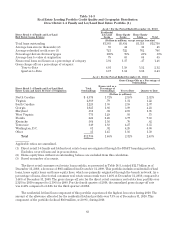

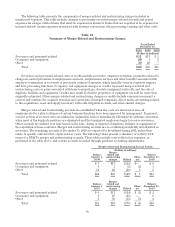

Additional disclosures related to BB&T’s real estate lending by product type and geographic distribution can be

found in Table 14 herein.

Noninterest Income

Noninterest income has become, and will continue to be, a significant contributor to BB&T’s financial

success. Noninterest income includes insurance income, service charges on deposit accounts, mortgage banking

income, investment banking and brokerage fees and commissions, trust and investment advisory revenues, gains

and losses on securities transactions, and commissions and fees derived from other activities. Noninterest income

as a percentage of total FTE revenues totaled 42.0% for 2010. Exceeding 40% on this measure has been a

management objective for several years. Management continues to focus on diversifying its sources of revenue to

further reduce BB&T’s reliance on traditional spread-based interest income, as fee-based activities are a

relatively stable revenue source during periods of changing interest rates.

69