BB&T 2010 Annual Report Download - page 149

Download and view the complete annual report

Please find page 149 of the 2010 BB&T annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

139 -

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

146 -

147

147 -

148

148 -

149

149 -

150

150 -

151

151 -

152

152 -

153

153 -

154

154 -

155

155 -

156

156 -

157

157 -

158

158 -

159

159 -

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

|

|

NOTE 17. Regulatory Requirements and Other Restrictions

Branch Bank and BB&T FSB are required by the Board of Governors of the Federal Reserve System to

maintain reserve balances in the form of vault cash or deposits with the Federal Reserve Bank based on specified

percentages of certain deposit types, subject to various adjustments. At December 31, 2010, the net reserve

requirement amounted to $361 million.

Branch Bank is subject to laws and regulations that limit the amount of dividends it can pay. In addition,

both BB&T and Branch Bank are subject to various regulatory restrictions relating to the payment of dividends,

including requirements to maintain capital at or above regulatory minimums, and to remain “well-capitalized”

under the prompt corrective action regulations. BB&T does not expect that any of these laws, regulations or

policies will materially affect the ability of Branch Bank to pay dividends.

BB&T is subject to various regulatory capital requirements administered by the Federal banking agencies.

Failure to meet minimum capital requirements can initiate certain mandatory—and possibly additional

discretionary—actions by regulators that, if undertaken, could have a direct material effect on BB&T’s financial

statements. Under capital adequacy guidelines and the regulatory framework for prompt corrective action, the

Corporation must meet specific capital guidelines that involve quantitative measures of BB&T’s assets, liabilities

and certain off-balance-sheet items calculated pursuant to regulatory directives. BB&T’s capital amounts and

classification also are subject to qualitative judgments by the regulators about components, risk weightings and

other factors. BB&T is in full compliance with these requirements. Banking regulations also identify five capital

categories for insured depository institutions: well-capitalized, adequately capitalized, undercapitalized,

significantly undercapitalized and critically undercapitalized. At December 31, 2010 and 2009, BB&T and Branch

Bank were classified as “well capitalized”.

Quantitative measures established by regulation to ensure capital adequacy require BB&T to maintain

minimum amounts and ratios of total and Tier 1 capital (as defined in the regulations) to risk-weighted assets (as

defined), and of Tier 1 capital to average tangible assets (leverage ratio).

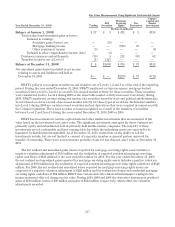

The following table provides summary information regarding regulatory capital for BB&T and Branch Bank

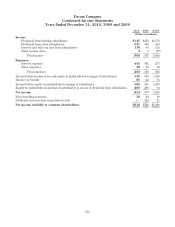

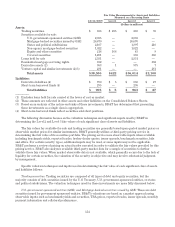

as of December 31, 2010 and 2009:

December 31, 2010 December 31, 2009

Actual Capital Capital Requirements Actual Capital Capital Requirements

Ratio Amount Minimum Well-Capitalized Ratio Amount Minimum Well-Capitalized

(Dollars in millions)

Tier 1 Capital

BB&T 11.8% $13,959 $4,725 $ 7,088 11.5% $13,456 $4,687 $7,030

Branch Bank 13.0 14,650 4,499 6,749 12.1 13,544 4,480 6,720

Total Capital

BB&T 15.5 18,319 9,450 11,813 15.8 18,470 9,373 11,717

Branch Bank 15.5 17,417 8,998 11,248 14.6 16,404 8,960 11,200

Leverage Capital

BB&T 9.1 13,959 6,134 7,667 8.5 13,456 6,322 7,903

Branch Bank 9.9 14,650 4,425 7,375 8.9 13,544 4,566 7,610

As an approved seller/servicer, Branch Bank is required to maintain minimum levels of shareholders’ equity,

as specified by various agencies, including the United States Department of Housing and Urban Development,

Government National Mortgage Association, Federal Home Loan Mortgage Corporation and Federal National

Mortgage Association. At December 31, 2010 and 2009, Branch Bank’s equity was above all required levels.

At December 31, 2010 and 2009, BB&T had segregated cash deposits totaling $309 million and $270 million,

respectively. These deposits relate to monies held for the exclusive benefit of clients, primarily at BB&T’s broker/

dealer subsidiaries.

149