Bank of America 2015 Annual Report Download - page 165

Download and view the complete annual report

Please find page 165 of the 2015 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

155 -

156

156 -

157

157 -

158

158 -

159

159 -

160

160 -

161

161 -

162

162 -

163

163 -

164

164 -

165

165 -

166

166 -

167

167 -

168

168 -

169

169 -

170

170 -

171

171 -

172

172 -

173

173 -

174

174 -

175

175 -

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

|

|

Bank of America 2015 163

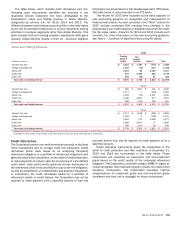

December 31, 2014

(Dollars in millions)

30-59 Days

Past Due (1)

60-89 Days

Past Due (1)

90 Days or

More

Past Due (2)

Total Past

Due 30

Days

or More

Total

Current or

Less Than

30 Days

Past Due (3)

Purchased

Credit-

impaired (4)

Loans

Accounted

for Under

the Fair

Value Option

Total

Outstandings

Consumer real estate

Core portfolio

Residential mortgage $ 1,847 $ 700 $ 5,561 $ 8,108 $ 154,112 $ 162,220

Home equity 218 105 744 1,067 50,820 51,887

Legacy Assets & Servicing portfolio

Residential mortgage (5) 2,008 1,060 10,513 13,581 25,244 $ 15,152 53,977

Home equity 374 174 1,166 1,714 26,507 5,617 33,838

Credit card and other consumer

U.S. credit card 494 341 866 1,701 90,178 91,879

Non-U.S. credit card 49 39 95 183 10,282 10,465

Direct/Indirect consumer (6) 245 71 65 381 80,000 80,381

Other consumer (7) 11 2 2 15 1,831 1,846

Total consumer 5,246 2,492 19,012 26,750 438,974 20,769 486,493

Consumer loans accounted for under the

fair value option (8) $ 2,077 2,077

Total consumer loans and leases 5,246 2,492 19,012 26,750 438,974 20,769 2,077 488,570

Commercial

U.S. commercial 320 151 318 789 219,504 220,293

Commercial real estate (9) 138 16 288 442 47,240 47,682

Commercial lease financing 121 41 42 204 24,662 24,866

Non-U.S. commercial 5 4 — 9 80,074 80,083

U.S. small business commercial 88 45 94 227 13,066 13,293

Total commercial 672 257 742 1,671 384,546 386,217

Commercial loans accounted for under

the fair value option (8) 6,604 6,604

Total commercial loans and leases 672 257 742 1,671 384,546 6,604 392,821

Total loans and leases $ 5,918 $ 2,749 $ 19,754 $ 28,421 $ 823,520 $ 20,769 $ 8,681 $ 881,391

Percentage of outstandings 0.67% 0.31% 2.24% 3.22% 93.44% 2.36% 0.98% 100.00%

(1) Consumer real estate loans 30-59 days past due includes fully-insured loans of $2.1 billion and nonperforming loans of $392 million. Consumer real estate loans 60-89 days past due includes fully-

insured loans of $1.1 billion and nonperforming loans of $332 million.

(2) Consumer real estate includes fully-insured loans of $11.4 billion.

(3) Consumer real estate includes $3.6 billion and direct/indirect consumer includes $27 million of nonperforming loans.

(4) PCI loan amounts are shown gross of the valuation allowance.

(5) Total outstandings includes pay option loans of $3.2 billion. The Corporation no longer originates this product.

(6) Total outstandings includes auto and specialty lending loans of $37.7 billion, unsecured consumer lending loans of $1.5 billion, U.S. securities-based lending loans of $35.8 billion, non-U.S. consumer

loans of $4.0 billion, student loans of $632 million and other consumer loans of $761 million.

(7) Total outstandings includes consumer finance loans of $676 million, consumer leases of $1.0 billion and consumer overdrafts of $162 million.

(8) Consumer loans accounted for under the fair value option were residential mortgage loans of $1.9 billion and home equity loans of $196 million. Commercial loans accounted for under the fair value

option were U.S. commercial loans of $1.9 billion and non-U.S. commercial loans of $4.7 billion. For additional information, see Note 20 – Fair Value Measurements and Note 21 – Fair Value Option.

(9) Total outstandings includes U.S. commercial real estate loans of $45.2 billion and non-U.S. commercial real estate loans of $2.5 billion.

The Corporation has entered into long-term credit protection

agreements with FNMA and FHLMC on loans totaling $3.7 billion

and $17.2 billion at December 31, 2015 and 2014, providing full

credit protection on residential mortgage loans that become

severely delinquent. All of these loans are individually insured and

therefore the Corporation does not record an allowance for credit

losses related to these loans.

Nonperforming Loans and Leases

The Corporation classifies junior-lien home equity loans as

nonperforming when the first-lien loan becomes 90 days past due

even if the junior-lien loan is performing. At December 31, 2015

and 2014, $484 million and $800 million of such junior-lien home

equity loans were included in nonperforming loans.

The Corporation classifies consumer real estate loans that

have been discharged in Chapter 7 bankruptcy and not reaffirmed

by the borrower as TDRs, irrespective of payment history or

delinquency status, even if the repayment terms for the loan have

not been otherwise modified. The Corporation continues to have

a lien on the underlying collateral. At December 31, 2015,

nonperforming loans discharged in Chapter 7 bankruptcy with no

change in repayment terms were $785 million of which $457

million were current on their contractual payments, while $285

million were 90 days or more past due. Of the contractually current

nonperforming loans, more than 80 percent were discharged in

Chapter 7 bankruptcy more than 12 months ago, and more than

60 percent were discharged 24 months or more ago. As

subsequent cash payments are received on these nonperforming

loans that are contractually current, the interest component of the

payments is generally recorded as interest income on a cash basis

and the principal component is recorded as a reduction in the

carrying value of the loan.