Bank of America 2015 Annual Report Download - page 49

Download and view the complete annual report

Please find page 49 of the 2015 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

|

|

Bank of America 2015 47

Estimated Range of Possible Loss

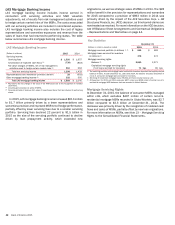

We currently estimate that the range of possible loss for

representations and warranties exposures could be up to $2 billion

over existing accruals at December 31, 2015. We treat claims that

are time-barred as resolved and do not consider such claims in

the estimated range of possible loss. The estimated range of

possible loss reflects principally exposures related to loans in

private-label securitization trusts. It represents a reasonably

possible loss, but does not represent a probable loss, and is based

on currently available information, significant judgment and a

number of assumptions that are subject to change.

For more information on the methodology used to estimate the

representations and warranties liability, the corresponding

estimated range of possible loss and the types of losses not

considered in such estimates, see Item 1A. Risk Factors of our

2015 Annual Report on Form 10-K and Note 7 – Representations

and Warranties Obligations and Corporate Guarantees to the

Consolidated Financial Statements and, for more information

related to the sensitivity of the assumptions used to estimate our

liability for representations and warranties, see Complex

Accounting Estimates – Representations and Warranties Liability

on page 102.

Department of Justice Settlement

On August 20, 2014, we reached a comprehensive settlement with

the DoJ and certain federal and state agencies (DoJ Settlement).

As part of the DoJ Settlement, we paid civil monetary penalties

and compensatory remediation payments in 2014. In 2014 and

2015, we provided creditable consumer relief activities primarily

in the form of mortgage modifications, including first-lien principal

forgiveness and forbearance modifications and second- and junior-

lien extinguishments, low- to moderate-income mortgage

originations, and community reinvestment and neighborhood

stabilization efforts, with initiatives focused on communities

experiencing, or at risk of, blight. Also, we have provided support

for the expansion of available affordable rental housing. Our

actions are well ahead of the DoJ agreement calling for us to

complete delivery of the consumer relief by no later than August

31, 2018. The consumer relief requirements are subject to

oversight by an independent monitor.

Other Mortgage-related Matters

We continue to be subject to additional borrower and non-borrower

litigation and governmental and regulatory scrutiny and

investigations related to our past and current origination, servicing,

transfer of servicing and servicing rights, servicing compliance

obligations, foreclosure activities, and MI and captive reinsurance

practices with mortgage insurers. The ongoing environment of

additional regulation, increased regulatory compliance obligations,

and enhanced regulatory enforcement, combined with ongoing

uncertainty related to the continuing evolution of the regulatory

environment, has resulted in increased operational and

compliance costs and may limit our ability to continue providing

certain products and services. For more information on

management’s estimate of the aggregate range of possible loss

and on regulatory investigations, see Note 12 – Commitments and

Contingencies to the Consolidated Financial Statements.

Managing Risk

Overview

Risk is inherent in all our business activities. Sound risk

management enables us to serve our customers and deliver for

our shareholders. If not managed well, risks can result in financial

loss, regulatory sanctions and penalties, and damage to our

reputation, each of which may adversely impact our ability to

execute our business strategies. The Corporation takes a

comprehensive approach to risk management with a defined Risk

Framework and an articulated Risk Appetite Statement which are

approved annually by the Enterprise Risk Committee (ERC) and

the Corporation’s Board of Directors (the Board).

The seven types of risk faced by the Corporation are strategic,

credit, market, liquidity, compliance, operational and reputational

risks.

Strategic risk is the risk resulting from incorrect assumptions

about external or internal factors, inappropriate business plans,

ineffective business strategy execution, or failure to respond in

a timely manner to changes in the regulatory, macroeconomic

or competitive environments.

Credit risk is the risk of loss arising from the inability or failure

of a borrower or counterparty to meet its obligations.

Market risk is the risk that changes in market conditions may

adversely impact the value of assets or liabilities, or otherwise

negatively impact earnings.

Liquidity risk is the potential inability to meet expected or

unexpected cash flow and collateral needs while continuing to

support our business and customer needs under a range of

economic conditions.

Compliance risk is the risk of legal or regulatory sanctions,

material financial loss or damage to the reputation of the

Corporation arising from the failure of the Corporation to comply

with the requirements of applicable laws, rules, regulations and

related self-regulatory organizations’ standards and codes of

conduct.

Operational risk is the risk of loss resulting from inadequate or

failed internal processes, people and systems, or from external

events.

Reputational risk is the risk that negative perceptions of the

Corporation’s conduct or business practices will adversely affect

its profitability or operations through an inability to establish or

maintain existing customer/client relationships.

The following sections address in more detail the specific

procedures, measures and analyses of the major categories of

risk. This discussion of managing risk focuses on the 2016 Risk

Framework (Risk Framework) that, as part of its annual review

process, was approved by the ERC and the Board in December

2015. The key enhancements from the 2015 Risk Framework

include further increasing the focus on our strong risk culture and

emphasizing our risk identification practices and the involvement

and input of Front Line Units (FLUs) and control functions. It

continues to recognize the same seven key risk types as discussed

above and our risk management approach as outlined below.

A strong risk culture is fundamental to our values and operating

principles. It requires us to focus on risk in all activities and

encourages the necessary mindset and behavior to enable

effective risk management, and promotes sound risk-taking within

our risk appetite. Sustaining a strong risk culture throughout the

organization is critical to the success of the Corporation and is a

clear expectation of our executive management team and the

Board.