Bank of America 2015 Annual Report Download - page 167

Download and view the complete annual report

Please find page 167 of the 2015 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

157 -

158

158 -

159

159 -

160

160 -

161

161 -

162

162 -

163

163 -

164

164 -

165

165 -

166

166 -

167

167 -

168

168 -

169

169 -

170

170 -

171

171 -

172

172 -

173

173 -

174

174 -

175

175 -

176

176 -

177

177 -

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

|

|

Bank of America 2015 165

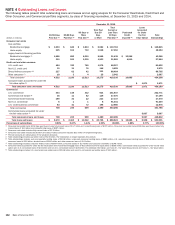

The following tables present certain credit quality indicators for the Corporation’s Consumer Real Estate, Credit Card and Other

Consumer, and Commercial portfolio segments, by class of financing receivables, at December 31, 2015 and 2014.

Consumer Real Estate – Credit Quality Indicators (1)

December 31, 2015

(Dollars in millions)

Core Portfolio

Residential

Mortgage (2)

Legacy Assets

& Servicing

Residential

Mortgage (2)

Residential

Mortgage PCI (3)

Core Portfolio

Home Equity (2)

Legacy Assets

& Servicing

Home Equity (2)

Home

Equity PCI

Refreshed LTV (4)

Less than or equal to 90 percent $ 109,869 $ 16,646 $ 8,655 $ 44,006 $ 15,666 $ 2,003

Greater than 90 percent but less than or equal to 100 percent 4,251 2,007 1,403 1,652 2,382 852

Greater than 100 percent 2,783 3,212 2,008 2,606 5,017 1,764

Fully-insured loans (5) 28,942 8,135 — — — —

Total consumer real estate $ 145,845 $ 30,000 $ 12,066 $ 48,264 $ 23,065 $ 4,619

Refreshed FICO score

Less than 620 $ 3,465 $ 4,408 $ 3,798 $ 1,898 $ 2,785 $ 729

Greater than or equal to 620 and less than 680 5,792 3,438 2,586 3,242 3,817 825

Greater than or equal to 680 and less than 740 22,017 5,605 3,187 9,203 6,527 1,356

Greater than or equal to 740 85,629 8,414 2,495 33,921 9,936 1,709

Fully-insured loans (5) 28,942 8,135 — — — —

Total consumer real estate $ 145,845 $ 30,000 $ 12,066 $ 48,264 $ 23,065 $ 4,619

(1) Excludes $1.9 billion of loans accounted for under the fair value option.

(2) Excludes PCI loans.

(3) Includes $2.0 billion of pay option loans. The Corporation no longer originates this product.

(4) Refreshed LTV percentages for PCI loans are calculated using the carrying value net of the related valuation allowance.

(5) Credit quality indicators are not reported for fully-insured loans as principal repayment is insured.

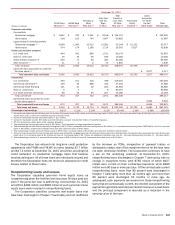

Credit Card and Other Consumer – Credit Quality Indicators

December 31, 2015

(Dollars in millions)

U.S. Credit

Card

Non-U.S.

Credit Card

Direct/Indirect

Consumer

Other

Consumer (1)

Refreshed FICO score

Less than 620 $ 4,196 $ — $ 1,244 $ 217

Greater than or equal to 620 and less than 680 11,857 — 1,698 214

Greater than or equal to 680 and less than 740 34,270 — 10,955 337

Greater than or equal to 740 39,279 — 29,581 1,149

Other internal credit metrics (2, 3, 4) — 9,975 45,317 150

Total credit card and other consumer $ 89,602 $ 9,975 $ 88,795 $ 2,067

(1) Twenty-seven percent of the other consumer portfolio is associated with portfolios from certain consumer finance businesses that the Corporation previously exited.

(2) Other internal credit metrics may include delinquency status, geography or other factors.

(3) Direct/indirect consumer includes $43.7 billion of securities-based lending which is overcollateralized and therefore has minimal credit risk and $567 million of loans the Corporation no longer

originates, primarily student loans.

(4) Non-U.S. credit card represents the U.K. credit card portfolio which is evaluated using internal credit metrics, including delinquency status. At December 31, 2015, 98 percent of this portfolio was

current or less than 30 days past due, one percent was 30-89 days past due and one percent was 90 days or more past due.

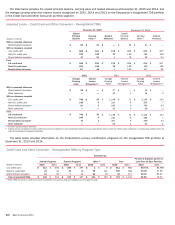

Commercial – Credit Quality Indicators (1)

December 31, 2015

(Dollars in millions)

U.S.

Commercial

Commercial

Real Estate

Commercial

Lease

Financing

Non-U.S.

Commercial

U.S. Small

Business

Commercial (2)

Risk ratings

Pass rated $ 243,922 $ 56,688 $ 26,050 $ 87,905 $ 571

Reservable criticized 8,849 511 1,320 3,644 96

Refreshed FICO score (3)

Less than 620 184

Greater than or equal to 620 and less than 680 543

Greater than or equal to 680 and less than 740 1,627

Greater than or equal to 740 3,027

Other internal credit metrics (3, 4) 6,828

Total commercial $ 252,771 $ 57,199 $ 27,370 $ 91,549 $ 12,876

(1) Excludes $5.1 billion of loans accounted for under the fair value option.

(2) U.S. small business commercial includes $670 million of criticized business card and small business loans which are evaluated using refreshed FICO scores or internal credit metrics, including

delinquency status, rather than risk ratings. At December 31, 2015, 98 percent of the balances where internal credit metrics are used was current or less than 30 days past due.

(3) Refreshed FICO score and other internal credit metrics are applicable only to the U.S. small business commercial portfolio.

(4) Other internal credit metrics may include delinquency status, application scores, geography or other factors.