Bank of America 2015 Annual Report Download - page 178

Download and view the complete annual report

Please find page 178 of the 2015 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

168 -

169

169 -

170

170 -

171

171 -

172

172 -

173

173 -

174

174 -

175

175 -

176

176 -

177

177 -

178

178 -

179

179 -

180

180 -

181

181 -

182

182 -

183

183 -

184

184 -

185

185 -

186

186 -

187

187 -

188

188 -

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

|

|

176 Bank of America 2015

The table below presents the December 31, 2015, 2014 and

2013 unpaid principal balance and carrying value of commercial

loans that were modified as TDRs during 2015, 2014 and 2013,

and net charge-offs that were recorded during the period in which

the modification occurred. The table below includes loans that

were initially classified as TDRs during the period and also loans

that had previously been classified as TDRs and were modified

again during the period.

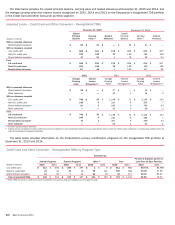

Commercial – TDRs Entered into During 2015, 2014 and

2013

December 31, 2015 2015

(Dollars in millions)

Unpaid

Principal

Balance

Carrying

Value

Net

Charge-offs

U.S. commercial $ 853 $ 779 $ 28

Commercial real estate 42 42 —

Non-U.S. commercial 329 326 —

U.S. small business commercial (1) 14 11 3

Total $ 1,238 $ 1,158 $ 31

December 31, 2014 2014

U.S. commercial $ 818 $ 785 $ 49

Commercial real estate 346 346 8

Non-U.S. commercial 44 43 —

U.S. small business commercial (1) 3 3 —

Total $ 1,211 $ 1,177 $ 57

December 31, 2013 2013

U.S. commercial $ 926 $ 910 $ 33

Commercial real estate 483 425 3

Non-U.S. commercial 61 44 7

U.S. small business commercial (1) 891

Total $ 1,478 $ 1,388 $ 44

(1) U.S. small business commercial TDRs are comprised of renegotiated small business card loans.

A commercial TDR is generally deemed to be in payment default

when the loan is 90 days or more past due, including delinquencies

that were not resolved as part of the modification. U.S. small

business commercial TDRs are deemed to be in payment default

during the quarter in which a borrower misses the second of two

consecutive payments. Payment defaults are one of the factors

considered when projecting future cash flows, along with

observable market prices or fair value of collateral when measuring

the allowance for loan and lease losses. TDRs that were in payment

default had a carrying value of $105 million, $103 million and $55

million for U.S. commercial and $25 million, $211 million and

$128 million for commercial real estate at December 31, 2015,

2014 and 2013, respectively.

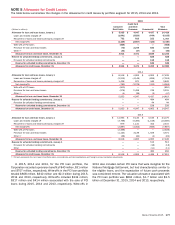

Purchased Credit-impaired Loans

PCI loans are acquired loans with evidence of credit quality

deterioration since origination for which it is probable at purchase

date that the Corporation will be unable to collect all contractually

required payments.

The following table shows activity for the accretable yield on

PCI loans, which include the Countrywide Financial Corporation

(Countrywide) portfolio and loans repurchased in connection with

the 2013 settlement with FNMA. The amount of accretable yield

is affected by changes in credit outlooks, including metrics such

as default rates and loss severities, prepayment speeds, which

can change the amount and period of time over which interest

payments are expected to be received, and the interest rates on

variable rate loans. The reclassifications from nonaccretable

difference during 2015 and 2014 were primarily due to lower

expected loss rates and a decrease in the forecasted prepayment

speeds. Changes in the prepayment assumption affect the

expected remaining life of the portfolio which results in a change

to the amount of future interest cash flows.

Rollforward of Accretable Yield

(Dollars in millions)

Accretable yield, January 1, 2014 $ 6,694

Accretion (1,061)

Disposals/transfers (506)

Reclassifications from nonaccretable difference 481

Accretable yield, December 31, 2014 5,608

Accretion (861)

Disposals/transfers (465)

Reclassifications from nonaccretable difference 287

Accretable yield, December 31, 2015 $ 4,569

During 2015, the Corporation sold PCI loans with a carrying

value of $1.4 billion, which excludes the related allowance of $234

million. For more information on PCI loans, see Note 1 – Summary

of Significant Accounting Principles, and for the carrying value and

valuation allowance for PCI loans, see Note 5 – Allowance for Credit

Losses.

Loans Held-for-sale

The Corporation had LHFS of $7.5 billion and $12.8 billion at

December 31, 2015 and 2014. Cash and non-cash proceeds from

sales and paydowns of loans originally classified as LHFS were

$41.2 billion, $40.1 billion and $81.0 billion for 2015, 2014 and

2013, respectively. Cash used for originations and purchases of

LHFS totaled $38.7 billion, $40.1 billion and $65.7 billion for

2015, 2014 and 2013, respectively.