Bank of America 2015 Annual Report Download - page 25

Download and view the complete annual report

Please find page 25 of the 2015 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

|

|

Bank of America 2015 23

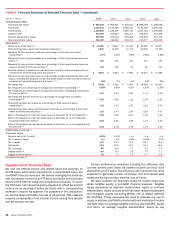

Noninterest Income

Table 3 Noninterest Income

(Dollars in millions) 2015 2014

Card income $ 5,959 $ 5,944

Service charges 7,381 7,443

Investment and brokerage services 13,337 13,284

Investment banking income 5,572 6,065

Equity investment income 261 1,130

Trading account profits 6,473 6,309

Mortgage banking income 2,364 1,563

Gains on sales of debt securities 1,091 1,354

Other income 818 1,203

Total noninterest income $ 43,256 $ 44,295

Noninterest income decreased $1.0 billion to $43.3 billion for

2015 compared to 2014. The following highlights the significant

changes.

Investment banking income decreased $493 million driven by

lower debt and equity issuance fees, partially offset by higher

advisory fees.

Equity investment income decreased $869 million as 2014

included a gain on the sale of a portion of an equity investment

and gains from an initial public offering (IPO) of an equity

investment in Global Markets.

Trading account profits increased $164 million. Excluding DVA,

trading account profits decreased $330 million driven by

declines in credit-related products reflecting lower client activity,

partially offset by strong performance in equity derivatives,

increased client activity in equities in the Asia-Pacific region,

improvement in currencies on higher client flows and increased

volatility. For more information on trading account profits, see

Global Markets on page 38.

Mortgage banking income increased $801 million primarily due

to lower provision for representations and warranties in 2015

compared to 2014, and to a lesser extent, improved mortgage

servicing rights (MSR) net-of-hedge performance and an

increase in core production revenue, partially offset by a decline

in servicing fees.

Other income decreased $385 million primarily due to DVA gains

of $407 million in 2014 compared to DVA losses of $633 million

in 2015, partially offset by higher gains on asset sales and lower

U.K. consumer payment protection insurance (PPI) costs in

2015. For more information on the accounting change related

to DVA, see Executive Summary – Recent Events on page 20.

Provision for Credit Losses

Table 4 Credit Quality Data

(Dollars in millions) 2015 2014

Provision for credit losses

Consumer $ 2,208 $ 1,482

Commercial 953 793

Total provision for credit losses $ 3,161 $ 2,275

Net charge-offs (1) $ 4,338 $ 4,383

Net charge-off ratio (2) 0.50% 0.49%

(1) Net charge-offs exclude write-offs in the purchased credit-impaired loan portfolio.

(2) Net charge-off ratios are calculated as net charge-offs divided by average outstanding loans

and leases excluding loans accounted for under the fair value option.

The provision for credit losses increased $886 million to $3.2

billion for 2015 compared to 2014. The provision for credit losses

was $1.2 billion lower than net charge-offs for 2015, resulting in

a reduction in the allowance for credit losses. The provision for

credit losses in 2014 included $400 million of additional costs

associated with the consumer relief portion of the settlement with

the U.S. Department of Justice (DoJ). Excluding these additional

costs, the provision for credit losses in the consumer portfolio

increased $1.1 billion compared to 2014 due to a slower pace of

portfolio improvement than in 2014, and also due to a lower level

of recoveries on nonperforming loan sales and other recoveries in

2015. The provision for credit losses for the commercial portfolio

increased $160 million in 2015 compared to 2014 driven by

energy sector exposure and higher unfunded balances. The

decrease in net charge-offs was primarily due to credit quality

improvement in the consumer portfolio, partially offset by higher

net charge-offs in the commercial portfolio primarily due to lower

net recoveries in commercial real estate and higher energy-related

net charge-offs.

As we look at 2016, reserve releases are expected to decrease

from 2015 levels. All else equal, this would result in increased

provision expense, assuming sustained stability in underlying

asset quality. For more information on the provision for credit

losses, see Provision for Credit Losses on page 86.