Bank of America 2015 Annual Report Download - page 238

Download and view the complete annual report

Please find page 238 of the 2015 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

228 -

229

229 -

230

230 -

231

231 -

232

232 -

233

233 -

234

234 -

235

235 -

236

236 -

237

237 -

238

238 -

239

239 -

240

240 -

241

241 -

242

242 -

243

243 -

244

244 -

245

245 -

246

246 -

247

247 -

248

248 -

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

|

|

236 Bank of America 2015

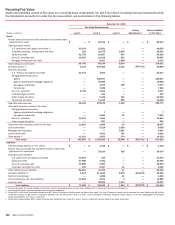

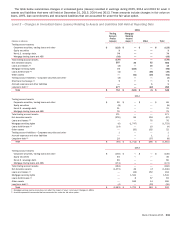

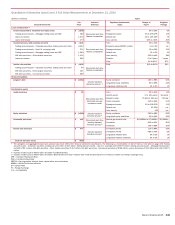

In the tables above, instruments backed by residential and

commercial real estate assets include RMBS, commercial

mortgage-backed securities, whole loans and mortgage CDOs.

Commercial loans, debt securities and other include corporate

CLOs and CDOs, commercial loans and bonds, and securities

backed by non-real estate assets. Structured liabilities primarily

include equity-linked notes that are accounted for under the fair

value option.

The Corporation uses multiple market approaches in valuing

certain of its Level 3 financial instruments. For example, market

comparables and discounted cash flows are used together. For a

given product, such as corporate debt securities, market

comparables may be used to estimate some of the unobservable

inputs and then these inputs are incorporated into a discounted

cash flow model. Therefore, the balances disclosed encompass

both of these techniques.

The level of aggregation and diversity within the products

disclosed in the tables result in certain ranges of inputs being

wide and unevenly distributed across asset and liability categories.

For more information on the inputs and techniques used in the

valuation of MSRs, see Note 23 – Mortgage Servicing Rights.

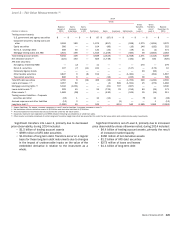

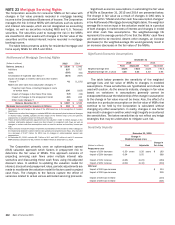

Sensitivity of Fair Value Measurements to Changes in

Unobservable Inputs

Loans and Securities

For instruments backed by residential real estate assets,

commercial real estate assets and commercial loans, debt

securities and other, a significant increase in market yields, default

rates, loss severities or duration would result in a significantly

lower fair value for long positions. Short positions would be

impacted in a directionally opposite way. The impact of changes

in prepayment speeds would have differing impacts depending on

the seniority of the instrument and, in the case of CLOs, whether

prepayments can be reinvested.

For auction rate securities, a significant increase in price would

result in a significantly higher fair value.

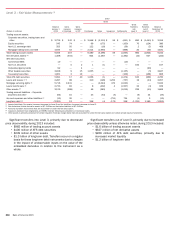

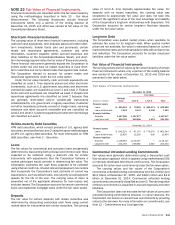

Structured Liabilities and Derivatives

For credit derivatives, a significant increase in market yield,

including spreads to indices, upfront points (i.e., a single upfront

payment made by a protection buyer at inception), credit spreads,

default rates or loss severities would result in a significantly lower

fair value for protection sellers and higher fair value for protection

buyers. The impact of changes in prepayment speeds would have

differing impacts depending on the seniority of the instrument and,

in the case of CLOs, whether prepayments can be reinvested.

Structured credit derivatives, which include tranched portfolio

CDS and derivatives with derivative product company (DPC) and

monoline counterparties, are impacted by credit correlation,

including default and wrong-way correlation. Default correlation is

a parameter that describes the degree of dependence among

credit default rates within a credit portfolio that underlies a credit

derivative instrument. The sensitivity of this input on the fair value

varies depending on the level of subordination of the tranche. For

senior tranches that are net purchases of protection, a significant

increase in default correlation would result in a significantly higher

fair value. Net short protection positions would be impacted in a

directionally opposite way. Wrong-way correlation is a parameter

that describes the probability that as exposure to a counterparty

increases, the credit quality of the counterparty decreases. A

significantly higher degree of wrong-way correlation between a DPC

counterparty and underlying derivative exposure would result in a

significantly lower fair value.

For equity derivatives, commodity derivatives, interest rate

derivatives and structured liabilities, a significant change in long-

dated rates and volatilities and correlation inputs (e.g., the degree

of correlation between an equity security and an index, between

two different commodities, between two different interest rates,

or between interest rates and foreign exchange rates) would result

in a significant impact to the fair value; however, the magnitude

and direction of the impact depends on whether the Corporation

is long or short the exposure.