Bank of America 2015 Annual Report Download - page 35

Download and view the complete annual report

Please find page 35 of the 2015 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

|

|

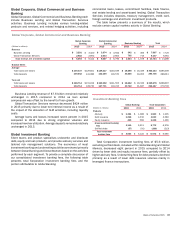

Bank of America 2015 33

During 2015, the total U.S. credit card risk-adjusted margin

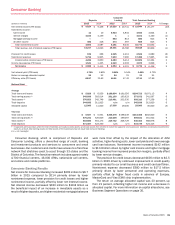

decreased 11 bps due to a decrease in net interest margin and

the net impact of gains on asset sales, partially offset by an

improvement in credit quality in the U.S. Card portfolio. Total U.S.

credit card purchase volumes increased $9.3 billion to $221.4

billion and debit card purchase volumes increased $5.1 billion to

$277.7 billion, reflecting higher levels of consumer spending.

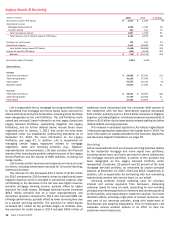

Mortgage Banking Income

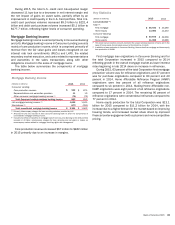

Mortgage banking income is earned primarily in Consumer Banking

and LAS. Mortgage banking income in Consumer Lending consists

mainly of core production income, which is comprised primarily of

revenue from the fair value gains and losses recognized on our

interest rate lock commitments (IRLCs) and LHFS, the related

secondary market execution, and costs related to representations

and warranties in the sales transactions along with other

obligations incurred in the sales of mortgage loans.

The table below summarizes the components of mortgage

banking income.

Mortgage Banking Income

(Dollars in millions) 2015 2014

Consumer Lending:

Core production revenue $ 942 $ 875

Representations and warranties provision 11 10

Other consumer mortgage banking income (1) (70) (72)

Total Consumer Lending mortgage banking income 883 813

LAS mortgage banking income (2) 1,658 1,045

Eliminations (3) (177) (295)

Total consolidated mortgage banking income $ 2,364 $ 1,563

(1) Primarily intercompany charges for loan servicing activities provided by LAS.

(2) Amounts for LAS are included in this Consumer Banking table to show the components of

consolidated mortgage banking income.

(3) Includes the effect of transfers of mortgage loans from Consumer Banking to the ALM portfolio

included in All Other, intercompany charges for loan servicing and net gains or losses on

intercompany trades related to mortgage servicing rights risk management.

Core production revenue increased $67 million to $942 million

in 2015 primarily due to an increase in margins.

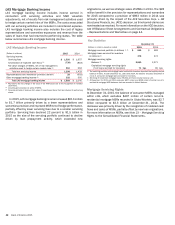

Key Statistics

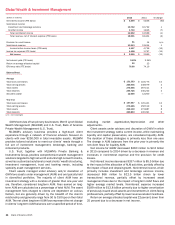

(Dollars in millions) 2015 2014

Loan production (1):

Total (2):

First mortgage $ 56,930 $ 43,290

Home equity 13,060 11,233

Consumer Banking:

First mortgage $ 40,878 $ 32,339

Home equity 11,988 10,286

(1) The above loan production amounts represent the unpaid principal balance of loans and in the

case of home equity, the principal amount of the total line of credit.

(2) In addition to loan production in Consumer Banking, there is also first mortgage and home equity

loan production in GWIM.

First mortgage loan originations in Consumer Banking and for

the total Corporation increased in 2015 compared to 2014

reflecting growth in the overall mortgage market as lower interest

rates beginning in late 2014 drove an increase in refinances.

During 2015, 63 percent of the total Corporation first mortgage

production volume was for refinance originations and 37 percent

was for purchase originations compared to 60 percent and 40

percent in 2014. Home Affordable Refinance Program (HARP)

originations were two percent of all refinance originations

compared to six percent in 2014. Making Home Affordable non-

HARP originations were eight percent of all refinance originations

compared to 17 percent in 2014. The remaining 90 percent of

refinance originations were conventional refinances compared to

77 percent in 2014.

Home equity production for the total Corporation was $13.1

billion for 2015 compared to $11.2 billion for 2014, with the

increase due to a higher demand in the market based on improving

housing trends, and increased market share driven by improved

financial center engagement with customers and more competitive

pricing.