Bank of America 2015 Annual Report Download - page 55

Download and view the complete annual report

Please find page 55 of the 2015 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

|

|

Bank of America 2015 53

December 31, 2015. Also effective January 1, 2015, Common

equity tier 1 capital is included in the measurement of “well-

capitalized” for depository institutions.

Beginning January 1, 2016, we are subject to a capital

conservation buffer, a countercyclical capital buffer and a global

systemically important bank (G-SIB) surcharge which will be

phased in over a three-year period ending January 1, 2019. Once

fully phased in, the Corporation’s risk-based capital ratio

requirements will include a capital conservation buffer greater than

2.5 percent, plus any applicable countercyclical capital buffer and

G-SIB surcharge in order to avoid certain restrictions on capital

distributions and discretionary bonus payments. The buffers and

surcharge must be composed solely of Common equity tier 1

capital. The countercyclical capital buffer is currently set at zero.

U.S. banking regulators must jointly decide on any increase in the

countercyclical buffer, after which time institutions will have up to

one year for implementation. Based on the Federal Reserve final

rule published in July 2015, we estimate that our G-SIB surcharge

will increase our risk-based capital ratio requirements by 3.0

percent once fully phased in. The G-SIB surcharge is calculated

annually and may differ from this estimate over time. For more

information on our G-SIB surcharge, see Capital Management –

Regulatory Developments on page 57.

Standardized Approach

Total risk-weighted assets under the Basel 3 Standardized

approach consist of credit risk and market risk measures. Credit

risk-weighted assets are measured by applying fixed risk weights

to on- and off-balance sheet exposures (excluding securitizations),

determined based on the characteristics of the exposure, such as

type of obligor, Organization for Economic Cooperation and

Development country risk code and maturity, among others. Off-

balance sheet exposures primarily include financial guarantees,

unfunded lending commitments, letters of credit and potential

future derivative exposures. Market risk applies to covered

positions which include trading assets and liabilities, foreign

exchange exposures and commodity exposures. Market risk

capital is modeled for general market risk and specific risk for

products where specific risk regulatory approval has been granted;

in the absence of specific risk model approval, standard specific

risk charges apply. For securitization exposures, risk-weighted

assets are determined using the Simplified Supervisory Formula

Approach (SSFA). Under the Standardized approach, no distinction

is made for variations in credit quality for corporate exposures,

and the economic benefit of collateral is restricted to a limited list

of eligible securities and cash.

Advanced Approaches

In addition to the credit risk and market risk measures, Basel 3

Advanced approaches include measures of operational risk and

risks related to the credit valuation adjustment (CVA) for over-the-

counter (OTC) derivative exposures. The Advanced approaches rely

on internal analytical models to measure risk weights for credit

risk exposures and allow the use of models to estimate the

exposure at default (EAD) for certain exposure types. Market risk

capital measurements are consistent with the Standardized

approach, except for securitization exposures. For both trading and

non-trading securitization exposures, institutions are permitted to

use the Supervisory Formula Approach (SFA) and would use the

SSFA if the SFA is unavailable for a particular exposure. Non-

securitization credit risk exposures are measured using internal

ratings-based models to determine the applicable risk weight by

estimating the probability of default, loss given default (LGD) and,

in certain instances, EAD. The internal analytical models primarily

rely on internal historical default and loss experience. Operational

risk is measured using internal analytical models which rely on

both internal and external operational loss experience and data.

The calculations require management to make estimates,

assumptions and interpretations, including with respect to the

probability of future events based on historical experience. Actual

results could differ from those estimates and assumptions. Under

the Federal Reserve’s reservation of authority, they may require us

to hold an amount of capital greater than otherwise required under

the capital rules if they determine that our risk-based capital

requirement using our internal analytical models is not

commensurate with our credit, market, operational or other risks.

Supplementary Leverage Ratio

Basel 3 also requires Advanced approaches institutions to

disclose a SLR. The numerator of the SLR is quarter-end Basel 3

Tier 1 capital reflective of Basel 3 numerator transition provisions.

The denominator is total leverage exposure based on the daily

average of the sum of on-balance sheet exposures less permitted

Tier 1 deductions, as well as the simple average of certain off-

balance sheet exposures, as of the end of each month in a quarter.

Off-balance sheet exposures primarily include undrawn lending

commitments, letters of credit, potential future derivative

exposures and repo-style transactions. Total leverage exposure

includes the effective notional principal amount of credit

derivatives and similar instruments through which credit protection

is sold. The credit conversion factors (CCFs) applied to certain off-

balance sheet exposures conform to the graduated CCF utilized

under the Basel 3 Standardized approach, but are subject to a

minimum 10 percent CCF. Effective January 1, 2018, the

Corporation will be required to maintain a minimum SLR of 3.0

percent, plus a supplementary leverage buffer of 2.0 percent, in

order to avoid certain restrictions on capital distributions and

discretionary bonuses. Insured depository institution subsidiaries

of BHCs, including BANA, will be required to maintain a minimum

6.0 percent SLR to be considered “well capitalized” under the PCA

framework.

Capital Composition and Ratios

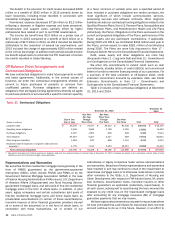

Table 13 presents Bank of America Corporation’s transition and

fully phased-in capital ratios and related information in accordance

with Basel 3 Standardized and Advanced approaches as measured

at December 31, 2015 and 2014. As of December 31, 2015 and

2014, the Corporation meets the definition of “well capitalized”

under current regulatory requirements.