Philips 2009 Annual Report Download - page 116

Download and view the complete annual report

Please find page 116 of the 2009 Philips annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

|

|

As of December 31, 2009, the company had country risk

exposure in the United States of EUR 9 billion and in the

Netherlands of EUR 8 billion. Other countries exceeding

EUR 1 billion but less than EUR 3 billion are China

(including Hong Kong) and Belgium. Countries where the

risk exceeded EUR 500 million but was less than EUR 1

billion are Germany and Japan. Countries where the risk

exceeded EUR 200 million but was less than EUR 500

million are Poland, Italy, Canada and France. The degree of

risk of a country is taken into account when new

investments are considered. The company does not,

however, use financial derivative instruments to hedge

country risk.

Other insurable risks

Philips is covered for a range of different kinds of losses by

global insurance policies in the areas of property damage,

business interruption, general and product liability,

transport, directors’ and officers’ liability, employment

practice liability, fraud, and aviation product liability.

To lower exposures and to avoid potential losses, Philips

has a worldwide Risk Engineering program in place. The

main focus in this program is on property damage and

business interruption risks, which also include

interdependencies. Philips sites, and also a limited number

of sites of key suppliers, are inspected on a regular basis by

the Risk Engineering personnel of the insurer. Inspections

are carried out against predefined Risk Engineering

standards which are agreed between Philips and the

insurers. Recommendations are made in a Risk

Management report and are reviewed centrally. This is the

basis for decision-making by the local management of the

business as to which recommendations will be

implemented. For all policies, deductibles are in place,

which vary from EUR 250,000 to EUR 500,000 per

occurrence and this variance is designed to differentiate

between the existing risk categories within Philips. Above

this first layer of working deductibles, Philips operates its

own re-insurance captive, which during 2009 retained

EUR 2.5 million per occurrence for the property damage

and business interruption losses and EUR 5 million in the

aggregate per year. For general and product liability

claims, the captive retained EUR 1.5 million per claim and

EUR 6 million in the aggregate. New contracts were

signed on December 31, 2009 for the coming year,

whereby the reinsurance captive retentions remained

unchanged.

6.7.3 Details of pension risks

This section further analyzes the pension exposure and

possible risks thereof.

Pension-related exposure to changes in

financial markets

With pension obligations in more than thirty countries,

Philips has devoted considerable attention and resources

to ensuring disclosure, awareness and control of the

resulting exposures.

Depending on the investment policies and the

membership composition of the respective pension funds,

developments in financial markets and changes in life

expectancy may have significant effects on the Funded

Status and net periodic pension costs (NPPC) of Philips’

pension plans. The pension plans in Germany, the

Netherlands, the UK and the US cover approximately 95%

of the Company’s total pension liabilities. To monitor

their exposure to the respective risk factors, Philips uses a

stochastic model. Amongst other things, the model allows

both sensitivity analysis and stochastic simulations of the

pension accounting figures of Philips. The sensitivity

analysis presented and described in this chapter does not

cover funding status or cost analysis on an economic or

regulatory valuation basis.

Sensitivity analysis

An indication of Philips’ accounting risk exposures related

to pensions can be obtained by a sensitivity analysis of the

Funded Status and NPPC for the above-mentioned

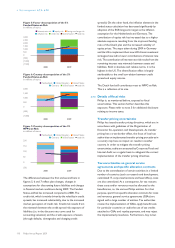

countries. The bar charts in figures 1 and 2 show the

sensitivities of the Funded Status to changes in equity price

levels, interest rates, inflation expectations and longevity.

Figures 3 and 4 show the same sensitivities for the NPPC.

The changes applied in this analysis represent

approximately one standard deviation and the absolute

numbers of the impact for each factor/assumption are

mentioned in the graphs. The risk numbers show how

much the Funded Status and NPPC change relative to

their (expected) levels at year-end 2010 if equity price

levels, interest rates, inflation expectation and longevity

trend deviate from their (expected) values at the end of

2010.

Figure 1: Sensitivity of funded status to equity

and interest rates

in millions of euros

Impact on funded status

■-Netherlands--■-United States--■-United Kingdom--■-Germany

1,000

750

500

250

0

(250)

(500)

(750)

(1,000) Equity

+20% -20%

Interest rate

+1% -1%

6 Risk management 6.7.2 - 6.7.3

116 Philips Annual Report 2009